During every earnings season, everyone talks about earnings trade strategies.

Whether their weapon of choice is the iron condor, the short strangle, the dual butterfly, the double calendar, or the diagonal, they are all trying to take advantage of the volatility drop that everyone knows will happen after the earnings event.

Some say that because the volatility drop is something that everyone already knows, there is no statistical advantage to playing a known predictable effect.

While others continue to do earnings trades every season with the belief that there is some edge.

Today, we are not getting into that debate.

We are not going to talk about earnings trade in the strict sense of the word, which means holding a trade across the earnings event.

Instead, today we are going to talk about a pre-earnings trade strategy.

By definition, a pre-earning trade is a trade placed and taken off before the earnings event.

This strategy utilizes a double calendar, which is a bit advanced since it consists of four legs.

But unlike an iron condor, its four legs are not in the same expiration.

This is not the only pre-earnings strategy out there.

And this is not a strategy invented here. In fact, this strategy can be seen in publicly available videos.

Contents

The Double Calendar Example

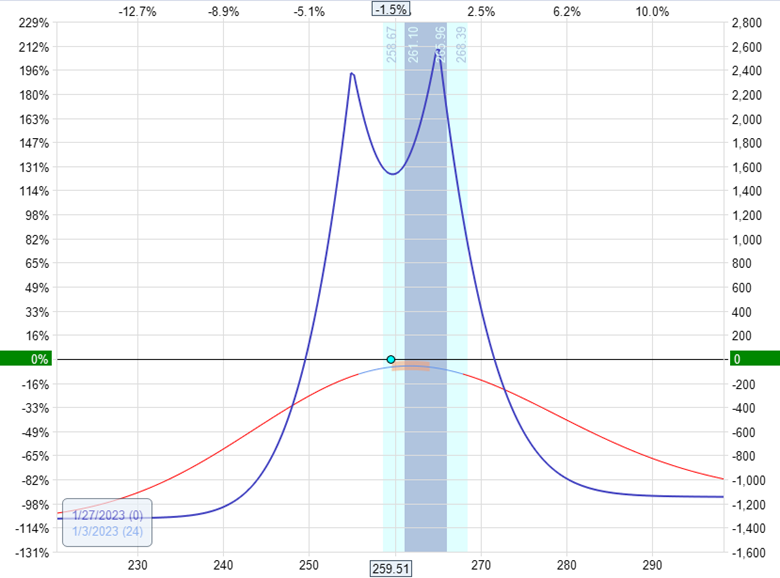

McDonald’s (MCD) announced earnings on January 31, 2023, before the market opened.

The following double calendar was initiated on January 3 (about one month prior to the announcement).

Date: January 3, 2023

Price: MCD @ $259.51

Buy ten February 3 MCD $255 put @ $4.65

Sell ten January 27 MCD $255 put @ $4.13

Sell ten January 27 MCD $265 call @ $4.05

Buy ten February 3 MCD $265 call @ $4.75

This is a 10-lot trade with a total debit of $1225.

For double calendars, the max risk equals the total debit paid for the trade, assuming you hadn’t made any adjustments.

If you make adjustments, that can increase or decrease the max risk in the trade.

You can see the max risk on the expiration graph.

Source: OptionNet Explorer

It is normal for one side to have a slightly higher risk than the other side.

The Construction

A few things to note about this construction.

- You always sell the front-month expiration.

- You always buy the back-month expiration.

- The strikes of the calls are the same. This is the definition of a calendar.

- The strikes of the puts are the same.

- The upper calendar is a call-calendar

- The lower calendar is a put-calendar

Even though we say “front-month” and “back-month,” we just mean the earlier expiration and the later expiration, respectively, even though both expirations can be in the same month.

It doesn’t matter if you use a put calendar or a call calendar for either the upper or lower calendar. Put calendars and call calendars are interchangeable.

And you can have both calendars as put-calendars as well as both calendars as call calendars.

The graph, the Greeks, and the trade will be nearly identical.

However, the call calendar is traditionally used for the upper calendar.

This is because calls at that upper strike will be out-of-the-money.

Puts at that strike will be in-the-money.

Traders often prefer working with out-of-the-money options because the bid-ask spread is believed to be slightly tighter for out-of-the-money options.

While there is some truth to that, the amount of difference is small and is apparent only when further out of the money away from the current price.

With the strikes of the double-calendar being fairly close to at-the-money, the difference in bid/ask is negligible, if at all.

Nevertheless, traders are used to using calls for the upper and puts for the lower calendar.

The Greeks

The initial values of the Greeks at the start of the trade are:

Delta: 8.45

Vega: 73.29

Theta: 36.51

Gamma: -3.71

The delta is slightly positive.

This is not by design, but rather with the strike availability as they are, this is what it turned out to be.

Note that strike selection on equities is more limited than the strike selection that is available on weekly index options.

Even though a small positive delta at the beginning of the trade may work out in our favor because the double calendar is long vega – or at least that’s what the Greeks say.

It is debatable whether calendars behave as per their Greeks in terms of vega all the time.

A long vega trade benefits if volatility increases.

It loses money if volatility decreases, as it typically would if MCD makes an up move.

Since it loses money due to volatility on an up move, some positive delta would gain some money on an up move.

So positive delta is a hedge against volatility dropping.

The trade has positive theta, which means that it generates money over time (with all other things being equal).

The theta component is not large.

But there is another aspect to the trade that helps it generate money.

The theta occurs because all options lose value over time.

For this trade, we expect short options to lose value more than long options.

This is going to benefit the trade.

The short options are not exposed to the earnings announcement because it expires prior to earnings. Hence, we expect these short options to decay in value normally.

Since we are selling them, we want them to drop in value.

We expect the long options to hold their value more or to decay in value less – at least until the earnings announcement is made, at which time we would have been out of the trade already.

We want the long options to hold their value because we own the long options.

How Were The Strikes Of The Calendars Selected?

The strikes were selected based on trial and error by looking at how the expiration graph looks – especially the location of the curve that is between the two calendar peaks.

When we say “expiration graph,” which expiration do we mean?

We mean the graph of the P&L at the time of the front-month expiration – not the graph of the back-month expiration.

Putting the strikes closer together will make the curve between the two peaks higher.

Putting the strikes closer together will give less range for the price to move.

Putting the strikes further apart will give a wider graph and more range for the price to move before needing to adjust.

However, the curve between the peaks will be lower.

A lower curve will mean less theta, meaning the trade makes money slower.

A higher curve means more theta.

That’s why we have to try different strikes to find the right balance so that strikes are not too far and not too close.

The curve between the peaks is not too high and not too low.

If it dips to almost touching the horizontal zero-profit line, then it is too low.

When To Adjust

The double calendar is a “range-bound” trade.

We want the price to stay in between the two peaks of the calendars and let theta decay work in generating income.

Generally, we want to adjust or take off the trade if the price moves beyond the strikes of either calendar.

Adjusting calendars is tricky because if you move the strike of either the short or long leg, you no longer have a calendar. You would have a diagonal, and you would give up one of the important characteristics of a calendar.

The max risk of the calendar is limited to the cost of that calendar.

This assertion is not true of diagonals.

Many traders will add or remove calendars to maintain calendars as calendars.

For example, if the price gets to the short strikes of the lower calendar, they remove the upper calendar.

Left with only one calendar, if the price moves to the edge of the calendar tent, they add back another calendar – letting the market dictate which side to add that calendar on.

FAQs

When to exit that double calendar pre-earnings strategy?

Some traders will hold the trade until the expiration of the short strikes.

But many will exit before then.

They may have a timed exit where they will say that they exit one week before the expiration of the short strike.

They may exit if they reach the profit target or loss limit on the trade.

They may exit due to market conditions and if they feel the trade is not going well or it is experiencing excessive adjustments.

Why trade pre-earning strategies versus trading earnings?

Earnings strategies that hold the trade across the earnings event take the risk of price making a large move due to earnings announcement.

This can easily result in a max loss in the trade.

These trades are also very short-term in nature, with expirations less than a week out.

These trades can get very exciting.

Pre-earnings strategies, where the trade is exited before the announcement, are not subject to these extremely large price moves.

They have longer duration expirations.

They are less exciting.

Some traders like to trade earnings because it is fun and exciting.

Other traders like to trade pre-earnings because they don’t like the unpredictability of the price move, and they want a slower-moving trade.

Some traders like to trade both in order to take full advantage of earnings opportunities.

How is the double calendar pre-earnings strategy different from the double calendar earnings strategy?

The two strategies can be easily confused.

The construction and the method of income generation are different between the two strategies.

The double calendar pre-earnings strategy (one we discussed today) relies on the volatility increasing on the long options more than the short ones.

As such, the expiration of the short option must be before the earnings date so that they are not exposed to the earnings event.

The double calendar earnings strategy (which is intended to be held through expiration) relies on the volatility crush of the earnings event.

As such, the short options (and therefore the long options as well) must have expirations after the earnings event so that the short options can experience the large implied volatility drop once earnings are announced.

Do the strike of the call calendar and the put calendar of the double calendar have to be equal distance from the current price?

No, it does not have to be.

Although often it is about similar in distance from the current price.

This is done, so that the price is in the middle between the two calendar peaks at the start of the trade.

The trader may decide to move one of the calendars further or closer to the current price to adjust the initial delta, either to get it closer to zero or to express his or her directional bias.

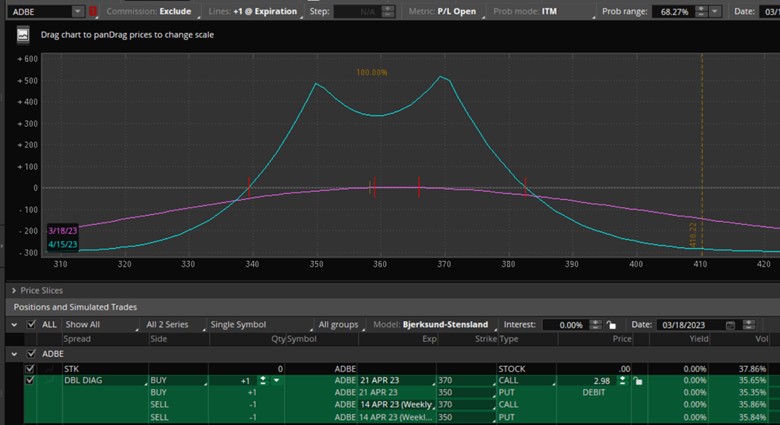

How does the double calendar risk graph look in ThinkOrSwim?

For those who are more used to the graphing interface of ThinkOrSwim rather than OptionNet Explorer, here is how a double-calendar on Adobe (ADBE) would look as a one-lot trade:

Even though this is a double calendar (look at the strikes), ThinkOrSwim will name them “double diagonals.”

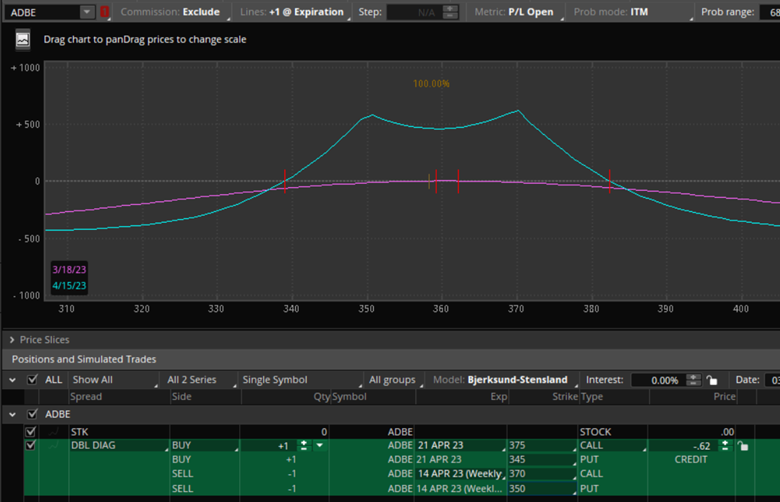

Can double-diagonals be used for pre-earnings trade?

Yes, they can.

Here is the risk graph of a double-diagonal pre-earnings trade in ADBE…

Double diagonals are the most flexible four-legged options structure there is.

Double calendars are just a sub-type of double-diagonals where the short and long strikes are the same.

While double-diagonals can also be used for earnings and pre-earnings trades, they generally cost more.

Their max risk will have to be determined by reading the risk graph.

The max risk of the double calendar can be more easily determined since one can not lose more than the initial cost of the double calendar

Conclusion

Regardless of using double-diagonal or double-calendars, these flexible structures can be adjusted in a variety of ways, including placement of the upper and lower strikes, the time to expiration of the short options, and the long options.

By tweaking these parameters, the trader achieves a risk graph that they believe will take advantage of the implied volatility increase as the stock approaches earnings announcement.

We hope you enjoyed this article about the double calendar pre-earnings strategy.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Related Articles

Double Calendar Spreads

Does it Matter if We Use Puts or Calls for Calendar Spreads

Controlling the Vega of Calendar Spreads

Calendarizing a Butterfly Spread

Calendarizing an Iron Condor

When do Calendar Spreads Have Negative Vega?

What are Reverse Calendar Spreads?

Calendar and Double Calendar Examples

Calendar Spreads 101

Calendar Spreads with Weekly Options

The Bullish Calendar Spread

Bearish Put Calendar Spread

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Hi Gavin,

I love your content on the Double Calendar spread for pre-earnings. I have been executing this exact strategy (both live and paper) for 2 quarters now with some success. I would like to be more consistent on my setup and exit. To date I have not made any adjustments to the spread unless it breaches one of my strikes, then I close the whole position. Can you elaborate on the following comment:

“For example, if the price gets to the short strikes of the lower calendar, they remove the upper calendar.”

“Left with only one calendar, if the price moves to the edge of the calendar tent, they add back another calendar – letting the market dictate which side to add that calendar on.”

What is meant by the edge of the tent on the risk graph?

Thank you and please advise

The expiration breakeven point.

To many stock with high expected move after the earnings, their double calender curve is always below the horizontal zero-profit line. I guess this strategy only works to the stocks with very low expected move after earnings, but theirs IV will not increase much for the earnings. Hi Gavin, Do you use it a lot?

It’s not one of my main strategies.