Last time, we showed the adjustment technique, using a calendar to defend an iron condor.

This time, we use a calendar to defend a non-directional butterfly.

In the condor case, we placed the calendar at the short leg of the threatened spread.

We will place the calendar for the butterfly at the long leg of the threatened lower wing.

You will see what I mean by the following example of an SPX trade that is already in progress.

Date: April 2, 2024

Price: SPX @ $5203

One long May 10 SPX 5275 put

Two short May 10 SPX 5225 put

One long May 10 SPX 5160 put

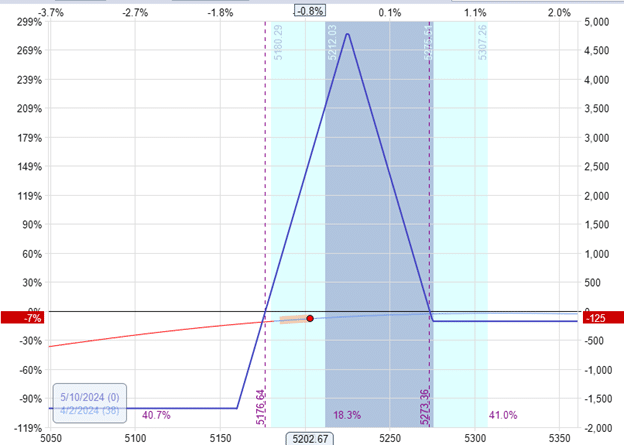

BEFORE:

Source: OptionNet Explorer

The price of SPX is near the left edge of the expiration graph with the following Greeks.

Delta: 1.83

Theta: 3.88

Vega: -50.76

Theta/Delta ratio: 2.1

The trader decides to calendarize the lower leg.

Sell to close the May 10 SPX 5160 put

Buy to open the May 17 SPX 5160 put

Debit: -$675

The adjustment is a calendar because we are selling a put option at the near-term expiration and buying one at the same strike at a further date.

Because the calendar’s short put option coincides with the butterfly’s long put option, it effectively closes out the long put of the butterfly and adds another long put option further out in time at the same strike.

One can think of it as rolling the long 5160 put option further out in time.

If “calendarizing the lower leg” sounds too much like a medical procedure, a less graphical description would be “rolling the lower long option out in time.”

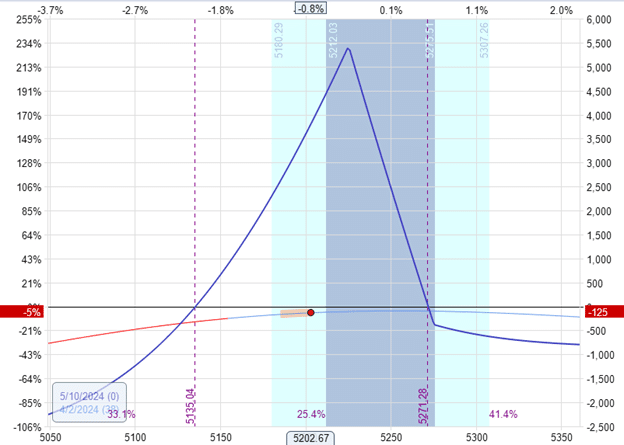

Afterwards, we are left with a butterfly with one leg at a different expiration:

One long May 10 SPX 5275 put

Two short May 10 SPX 5225 put

One long May 17 SPX 5160 put

AFTER:

You will immediately notice that its expiration graph has widened, and the price is more centrally located underneath the “tent.”

We have increased the distance to the lower expiration breakeven points, which was at 5176 to now 5135 (see purple vertical line).

The changes in the Greeks have also improved.

Delta: 1.65

Theta: 11.88

Vega: 6.21

Theta/Delta ratio: 7.2

While it has only decreased the delta slightly, the calendar has greatly increased theta, thereby boosting the theta/delta ratio.

Non-directional premium sellers utilizing this butterfly rely on theta for the trade’s income generation.

The delta represents the price risk.

A higher theta/delta ratio indicates an improvement in the trade’s reward-to-risk characteristics.

Conclusion

This adjustment works well when the price is moving down.

When the market is moving down, its volatility typically increases.

The negative vega is a liability.

The adjustment completely removed the butterfly’s negative vega and decreased the trade’s sensitivity to volatility changes.

However, the timing of the adjustment is critical.

If the underlying price had already dropped below the strike of the lower leg, then the adjustment would not be as effective because now the calendar is above the price instead of below it.

Another variable is how far out in time you want to roll the lower option.

In our example, the expiration of the short and the long options are seven days apart.

This seems to be a reasonable time spread for when the butterfly is about a month away from expiration.

For butterflies closer to expiration, experiment with time differences that are 4 or 3 days apart.

As with all new adjustments that a trader might learn, it is important to model them in all configurations and different market environments.

We hope you enjoyed this article on calendarizing a butterfly spread.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Related Articles

Double Calendar Spreads

Does it Matter if We Use Puts or Calls for Calendar Spreads

Controlling the Vega of Calendar Spreads

Calendar Spreads 101

Calendarizing an Iron Condor

When do Calendar Spreads Have Negative Vega?

What are Reverse Calendar Spreads?

Calendar and Double Calendar Examples

The Double Calendar Pre-Earnings Strategy

Calendar Spreads with Weekly Options

The Bullish Calendar Spread

Bearish Put Calendar Spread

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

It’s amazing, thank you!