Contents

The wheel options strategy is an excellent income-generating strategy that we have discussed before.

However, it is not without risk. It has undefined risk in all phases of the wheel.

The short put, long stock, and covered call are all undefined risk.

A significant amount of money can be lost in a market crash during any of these phases.

I’m writing this when the VIX closed above 30 at a nine-month high, and no one knows what the market will do on Monday.

While cash is a position, how about, we tweak the wheel strategy so that it has defined risk all the way.

Then we can more safely trade it during uncertain times. We will compare how it does compare to the regular wheel strategy.

Example Case Study

We will run the protected wheel strategy on Cola-Cola (KO) during the year 2020.

This will be a reasonable representative time period consisting of bearish first six months, which includes the pandemic selloff.

The price of KO fell 18.7% during the first half of the year.

It recovered during the last six months of the year when it when up 22.3%.

This will be our representative bullish trend.

If we want to see how the protected wheel did in an overall neutral move, look at the entire year 2020, where Coca-Cola started at $54.99 and ended the year nearly at the same price of $54.84.

Coca-Cola is a good stock to do the wheel on because it is a stable large-cap company that pays decent dividends with the following ex-dividend dates (which we shall consider if the stock gets assigned).

Mar 13, 2020: $0.41/share

Jun 12, 2020: $0.41/share

Sep 14, 2020: $0.41/share

Nov 30, 2020: $0.41/share

KO’s beta of 0.69 makes it a less volatile stock suitable for wheel trades.

However, the year 2020 turned out to be quite a volatile year.

Steps for the Protected Wheel

First, familiarize yourself with the standard wheel strategy described here.

Then we modify it so that we sell a put spread instead of a short put in the protected wheel strategy.

If we get assigned and own stock, we buy a six-month at-the-money put to protect our stock position.

The following backtest was run with OptionNet Explorer, where we sold short puts and covered calls at the market open, and we calculate the profit and loss at the dates shown at the close of market day.

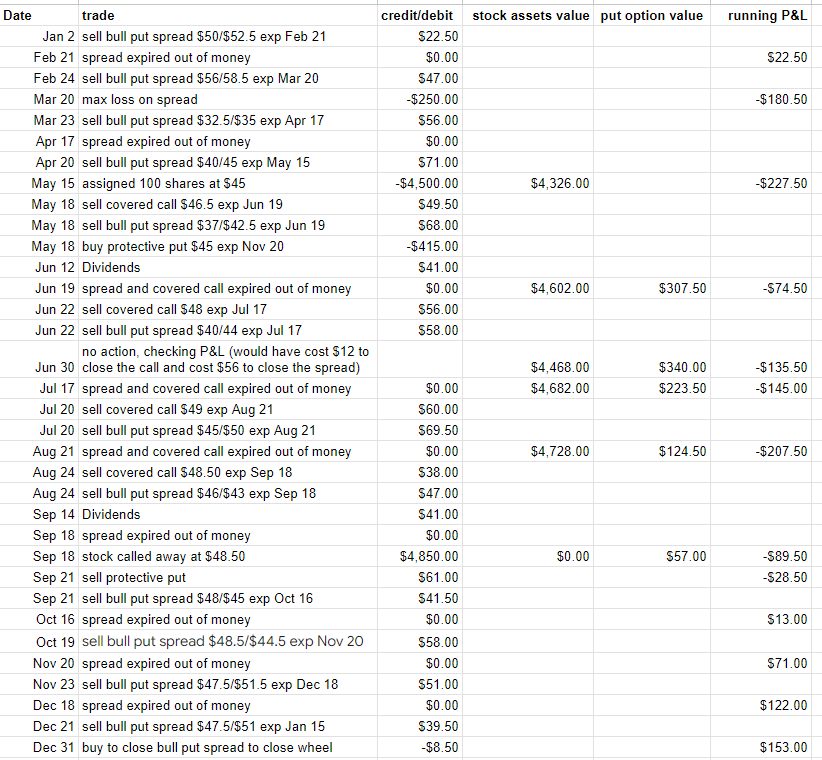

On January 2, 2020, we started by selling the $50/$52.5 bull put spread and collected a credit of $22.50.

When this spread expired out-of-the-money at the end-of-day on February 21, well sell another bull put spread the following Monday at the open.

With the price of KO at $59.64, the short put strike was chosen at $58.5 (around 30-delta) and the long put strike at $56.

This collected a credit of $47. With the spread width at $2.50, the max loss on this spread would be $203 = $250 – $47.

On expiration March 20, the price of KO was down to $38.30 (a drop of nearly 36%).

This is near the bottom of the market crash in March 2020.

Price had dropped straight down through the entire spread like a hot knife through butter.

The spread is at a max loss.

But because the bull put spread was a defined-risk position, we had only to pay out $250 at the March 20 expiration.

Adding all the credit received, the net profit and loss (P&L) is a loss of –$180.50 so far.

Continuing the strategy, we sell another spread and collected $56 on March 23.

The spread expired worthless.

We sell the $40/$45 bull put spread on April 20, collecting a credit of $71 with a max loss of $429 = $500 – $71.

The risk-to-reward ratio is 6.

At expiration on May 15, the price of KO is $43.26, which is below the short put strike of $45 yet above the long put of $40.

We are assigned 100 shares of KO at $45.

In other words, we were obligated to spend $4500 to buy these 100 shares, which are worth only $4326.

Referring to the spreadsheet above, if we tally all the incoming credits and outgoing debits to this point and add the value of the stock asset we own, the current loss is $227.50.

Just like in the traditional wheel strategy, we sell the $46.50 covered call collecting a credit of $49.50 on May 18.

Since KO is a lower-priced stock, we are willing to take up to 200 shares. So at the same time, we sell another bull put spread for a credit of $68.

If we just hold 100 shares of long stock, this is an undefined risk position (even with the covered call in place).

Therefore, in the protected wheel strategy, we also buy a put option to protect the stock.

This makes it a defined risk strategy.

Referring to the above spreadsheet, we bought the $45 at-the-money put costing $415.

This put expires in 6 months.

Since we are holding 100 shares of KO on the ex-dividend date of June 12, we collected $41 in dividends.

On expiration June 19, both the bull put spread, and the covered call expired out-of-the-money, so no money was credited or debited.

The value of our put option is down to $307.50 due to a combination of price movement, volatility changes, and time decay.

The following Monday, June 22, we sell another covered call (collected $56), and another bull put spread (collected $58).

Let’s check the P&L at the six-month mark on June 30.

Tallying all the credits and debits and adding the current value of the 100 shares (valued at $4468) and the current value of our long protective put (valued at $340), and figuring the cost to buy-to-close the short call and put spread, we see a net P&L of -$135.50.

This is quite good, considering that a buy-and-hold investor who had bought 100 shares of KO on January 2 would have lost $1064 on June 30 — a loss of 19%.

Continuing the protected wheel strategy in this way, we see that at the end of the year, the strategy nets $153 in profit even though the price of KO from the start of the year to the end of the year were essentially the same (see price chart above).

Compared to the Regular Wheel

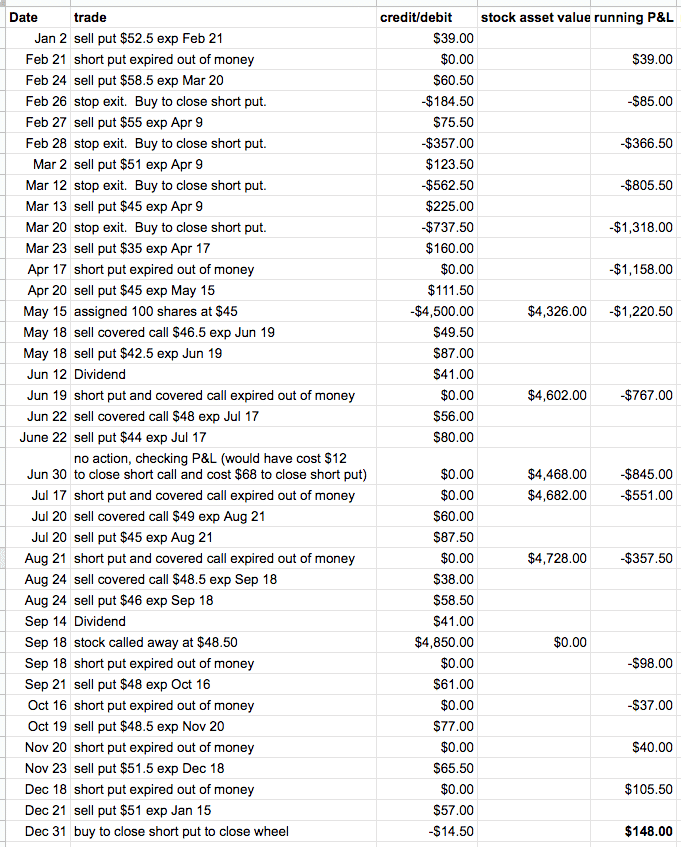

If we run the regular wheel strategy on the same timeframe, stock, and strikes, we see that the strategy took significant losses in the March crash on March 20.

Because the regular wheel is an unlimited loss strategy, many investors will have a stop loss to prevent large drawdowns.

This backtest uses the following mental stop loss rules:

Exit long stock if the stock drops 10%.

Exit short puts if its loss exceeds two times the credit received (at end-of-day closing prices)

We ran this same experiment without the use of stop losses, and the results were much worst.

We did not have to use any stop loss on the protected wheel strategy because that already has defined risk.

By the end of the first half of 2020, the wheel strategy lost $845.

However, it did a good job of recovering all of that loss from June 30 to December 31 — making a gain of $993 and resulting in an end-of-year P&L of $148.

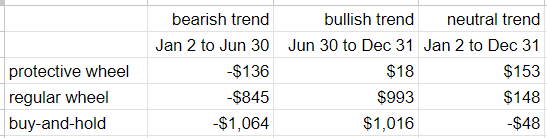

Results

Owning long stock (just buy-and-hold) would give the largest return ($1016) in a bullish market.

But in a bearish market or market crash, the buy-and-hold long stock also incurs the greatest loss (–$1064).

Trading the regular wheel strategy can incur significant losses (–$845) in a downtrend, as seen in the first half of 2020.

But it is not as bad as the buy-and-hold strategy since the losses are offset by credits received from covered calls and short puts.

We see that the protected wheel strategy helps protect a lot of the loss in bearish conditions.

Despite the severe selloff, there was no loss in the first half of 2020.

However, it does not make as much in a bull market.

It made only $18 in the bullish latter half of 2020, while the regular wheel and long stock made $993 and $1016, respectively.

Nevertheless, because it prevented a large drawdown in a market crash, it was able to come out ahead in 2020 with a profit of $153, outperforming the other two strategies.

Remember, if a strategy incurs a 25% drawdown, it requires a 33% gain from that point to get back to break even.

From the above price chart, we can see that KO dropped 18.7% during the first half of the year.

But it required a gain of 22.3% in the second half of the year to come back to breakeven.

Limiting large losses is essential. The protected wheel strategy is a defined-risk strategy that you can consider to limit large losses.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Hi,

great article. Would you say this protected wheel options strategy applied to blue chips is a trade that can be done without too much worrying?

Generally yes, but even blue-chips can drop 50% from time to time.

Hi Gavin

That is another great article! I am paper trading the wheel in TOS but this might be a little bit better. I am the kind of person that hates losing and sitting on drawdowns (holding good stock through bad times I don’t see it as a DD). I have a couple of questions if you don’t mind:

1. Do you think this works with SPY, QQQ, etc instead of stocks. The reason would be a whole index has fewer reasons (i guess?!) to suffer a big drop and will surely recover at some point even if a single stock gets bankrupted.

2. What do you think would happen if using weekly options instead of monthly? I am the kind that can’t wait to get in but also can’t wait to get out 🙂

3. How do you select the put spread legs? Is it by delta? Best credit?

4. How do you select the covered call strike? Closes to the ATM? Delta related?

Hi Mario,

1. Yes typically ETF are less risky than individual stocks because you don’t have stock specific risk, earnings risk etc. Very little change SPY goes to $0.

2. Weekly options offer a higher return on an annualized basis, but they also move a lot quicker. If the stock has a sudden drop, it is harder to adjust. Be careful with weekly options if you are a beginner. Higher returns = higher risk, always.

3. By a combination of delta, technical analysis and a minimum annualized return that I want to achieve if the stock expires worthless.

4. Technical analysis, minimum annualized return.

Are you available for individual coaching on this strategy? Would be very grateful!

Hi Jerry, I don’t do individual coaching, but have a group program starting next week if you are interested.

Hi Gavin — love your strategy here — had a question for you. If you get assigned on the 2nd lot of 100 shares of stock — do you buy a second long protective put? or just ride with the first protective put?

Depends on the situation, but if the market is turning bearish, it can be a good idea to add the second long put as protection.

am i missing something? looks like u forgot to take out the cost /loss for the protective put. in that case looks like the same outcome for both strats. then both end about $150 positive

Hi Justin, everything seems ok to me. Note that when we sell a bull put spread, we do not need to buy another put. The bull put spread already has a long put option as protection to make it a defined risk strategy. We only need to buy a long protective put when we get assigned 100 shares of stock as we did on Friday May 15, 2020. But we don’t know this for sure until Monday May 18, which is when we purchased the $45 strike protective put with expiration of November 20. This is noted in the spreadsheet as having a cost of -$415 on May 18.

We do not need to buy any additional protective puts for the next several cycles since this one protective put is far enough in expiration to protect our stock until November.

Nevertheless, due to selling covered calls, our stock got called away on September 18. No longer needing our protective put to protect non-existing stock, we sold the protective put and recovered $61 back.

I’m not saying that in all cases the protected wheel strategy will win over the traditional strategy. There are certainly situations that would far better doing without the protective put. It is just that in this example, we see that the protected wheel strategy had some benefits.

,,Hi Gavin, you write – Referring to the above spreadsheet, we bought the $45 at-the-money put costing $415.

You buy und 6 months Hedge ATM or at the assigned price? I know in your example $45 fits vor both. Would you Close the stock position and the hedge when the stock drops again and you can no longer sell CC?

Thanx for your answer.

Bruno

Hi Bruno, it depends. Every scenario is different.

Seems Buffet is somewhat of a protective put on Coke. I’d just run a regular wheel and average down as it fell. So if you were put the stock at 45 sell a strangle say 47-37 and if put at 37 sell another strangle say 40-31…Doubt Coke is going to 0.

You do need to plan the trade accordingly. I’d think of the ownership of shares max 300 as an apartment building and the premiums are my rent and eventually the apartment will grow in value. the divs add to my rental income.

Hi Dave, that is 100% my process as well. When I start a wheel I have a 10+ year time horizon on holding the stock if need be.

You must be doing pretty good with that strategy. I dont have a way to backtest my own safe wheel strategy so just jumping in. I start with a sort of poor mans covered put ie buy a 12 month ITM option like Julian sell weeklies a few strikes otm vs that owned put. If assigned do the cc’s all the while monitor the owned put. If the price goes up on the stock too much the owned put declines too fast so needs to be managed. Only a couple months into it so who knows how it’ll work out. Have 3 positions CVX, ALLY, and for fun NVDA. Insurance cost roughly 4400 for the year and getting 870 or so in option sales per month. Time will tell

Hi Gavin,

Thanks for exploring this Protective wheel strategy. In the P/L column on June 19, I am a little loss as to the calculations arriving at the $99.50 value. Could you help elaborate please? Thanks.

Thanks for checking my numbers. There was an error in the calculation of the June 19 running P&L. Instead of the $99.50, it should to -$74.50. With the P&L on May 15 at -$227.50, we add $49.50, add $68, and add $41 for the sale of covered call, sale of bull put spread, and collection of dividends. Then we add $102 for the appreciation of stock and subtract $107.5 for the loss in value of the protective put. To finally arrive at running P&L of -$74.50. I’ve made the correction now. Thanks again.

Thanks. That make sense now.

I have used a similar technique for the last few months, working ok. Now I am refining it and spending lots of $ for protection (by buying a put) but it guarantees me a profit. I kind of use a weekly wheel strategy BUT buy a 6 month expiration PUT 20% in the money, (very expensive). Then I will sell puts and covered calls to pay for the hedge.. I am guaranteed to be able to sell my shares for 20% above the current prize in 6 months. I will let you know how it works in June 2024.

Julian you are not guaranteed as the cost of the expensive put maybe more than the sum of premiums sold. I am sure you knew this going in. So how did you do ? I’m sort of doing the same thing although some puts that I but are atm or itm or slightly otm so a variety.

I looked for your June 2024 results but could not find them. Please advise and let us know how you did

hi Gavin, when you sell the bull put spread, why don’t you also sell the far OTM bear call spread to get more premium just like iron condor? I think it is definitely somewhat more profitable. What is your idea?

Yes I do that sometimes if I want to reduce the delta exposure. It’s great because you generate more premium and reduce your directional risk.