Today, we’re going to take a look at the risk reversal option strategy.

Contents

- Introduction

- What Is A Risk Reversal?

- How Do You Trade A Risk Reversal Strategy?

- When To Deploy A Risk Reversal Strategy?

- Maximum Loss

- Maximum Gain

- Breakeven Price

- Payoff Diagram

- Risk of Early Assignment

- Greeks

- Risk Reversal vs Long Stock

- Advantages and Disadvantages of a Risk Reversal Strategy

- Risk Reversal Example

- Conclusion

Introduction

Successful option trading requires sound risk management principles.

Most traders who fail, do so because they make large bets without adequate risk management.

When those bets go against them, they end up losing all the money in their account.

While there are many aspects to adequate risk management, this article will focus on one such approach which is called a risk reversal strategy.

This is a specific type of risk management called hedging.

Note that a risk reversal can also be used to double down on a directional bet, which we will touch on later in the article.

Before we delve into the strategy, it’s worth refreshing just what hedging is.

At its core, hedging is a process which aims to eliminate, or at the very least minimize, the downside risk of a position and/or an entire portfolio.

The way a hedge works, is that it attempts to eliminate the directional risk of a position, generally by using a related trade with an opposite direction.

So for example, if you are long a particular underlying asset, you would go short in a comparable asset.

This way, if your long bet turns out to be wrong, you make some profits on the related short position (your hedge) and you minimize or eliminate the amount of loss on the long position.

In essence, this is how a risk reversal strategy works when used for hedging, which we will now cover in more detail.

What Is A Risk Reversal?

A risk reversal strategy is generally used as a hedging strategy. It is designed to protect a trader’s long or short position, by using out-of-the-money call and put options.

Risk reversal strategies are typically favored by experienced traders such as institutional investors, as retail traders are generally unaware of its capabilities.

When used as a hedging strategy, total profit potential will be limited but the upside is that a trader’s positions are protected against unfavorable price movements.

All this can be achieved at very little cost which is why this is an attractive strategy for many traders.

A risk reversal can also be used to double down on a directional call such as when a trader feels particularly bearish or bullish about a position and may be seeking greater leverage.

How Do You Trade A Risk Reversal Strategy?

The basic way to deploy a risk reversal strategy involves the simultaneous selling (or writing) of an out-of-the-money call or put option, whilst simultaneously buying the opposite option.

In both cases the put and call will use the same expiration date.

So for example, you may sell an out-of-the-money put option and simultaneously buy an out-of-the-money call option.

By writing the put, you will receive a premium which you can then use towards buying the call.

In this example, the trader will have a net debit if the the cost of buying the call will be higher than the premium received for selling the put.

If the trader was to do a reverse of this trade (selling a call and buying a put) then they would generate a net credit.

Note that commissions also need to be considered and these will potentially change the balance of the trade.

By executing a risk reversal strategy, a trader is in effect reversing their volatility skew risk.

Consider that out-of-the-money puts are typically more expensive (they have higher implied volatilities) than out-of-the-money calls.

This is due to a much greater demand for puts as these are typically used as a hedge for long positions.

Since a trader generally sells options with higher implied volatility and buys options with lower implied volatility when executing a risk reversal strategy, they are in effect reversing volatility skew risk.

When To Deploy A Risk Reversal Strategy?

There are a number of scenarios where a risk reversal strategy can yield benefits.

The first is when you are very bullish on a stock and wish to leverage up your position. In this scenario you would write an out-of-the-money put and then use the associated premium to buy an out-of-the-money call, in effect doubling down on your bullish view.

The second scenario is in the lead up to important events like a stock split or spinoff, where there is some downside support while the end result should be appreciable price gains.

A third scenario is when a blue-chip stock has a sharp fall during a strong bull market that is unlikely to remain at those levels over the long term (for example panic over a temporary disruption to production).

In this case a risk reversal strategy would work very well should the stock rebound in the medium-term.

Finally, whenever you have an existing short or long position and desire some protection, you can use a risk reversal strategy as a way to hedge the position.

Maximum Loss

The maximum loss on a risk reversal is unlimited up to the point of the stock reaching $0. It will depend on the price of the put being sold.

For example, if a $30 put is sold, the maximum loss would be $3,000 less any net premium received on the trade.

If premium was paid to enter the trade (i.e. the bought call was higher in price than the sold put), the maximum loss would be $3,000 PLUS the premium paid.

If a $150 put was sold, the maximum loss would be $9,000 plus or minus the net premium received / paid on the trade.

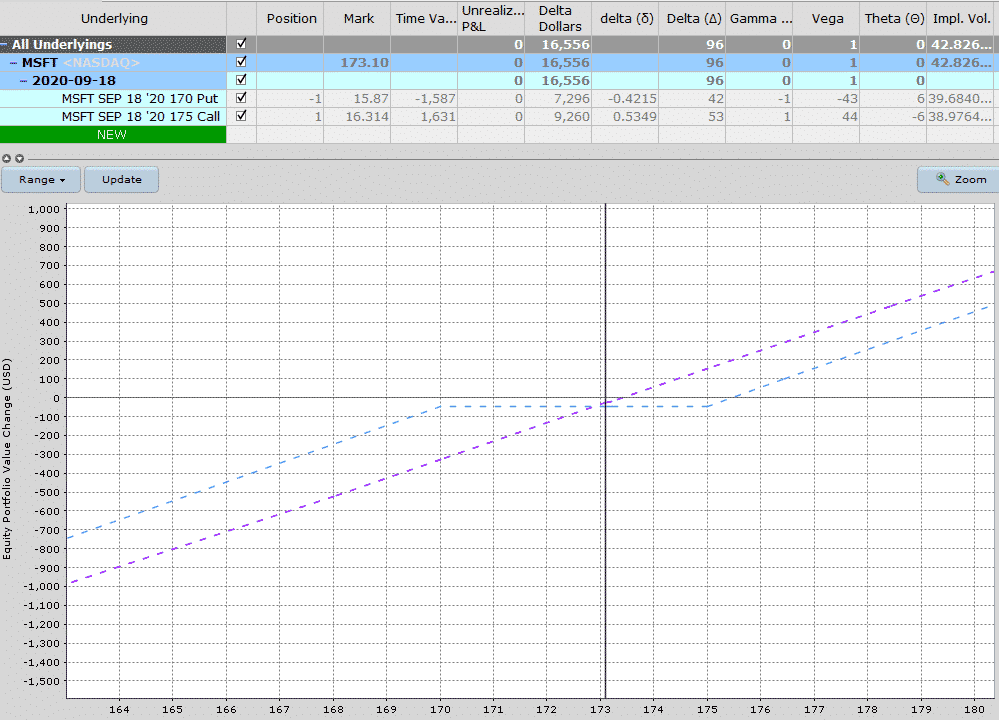

Using this example for MSFT, the call was bought for $16.30 and the put was sold for $15.87. That results in a net cost to enter the trade of $43.

The maximum loss in this case would be $17,043.

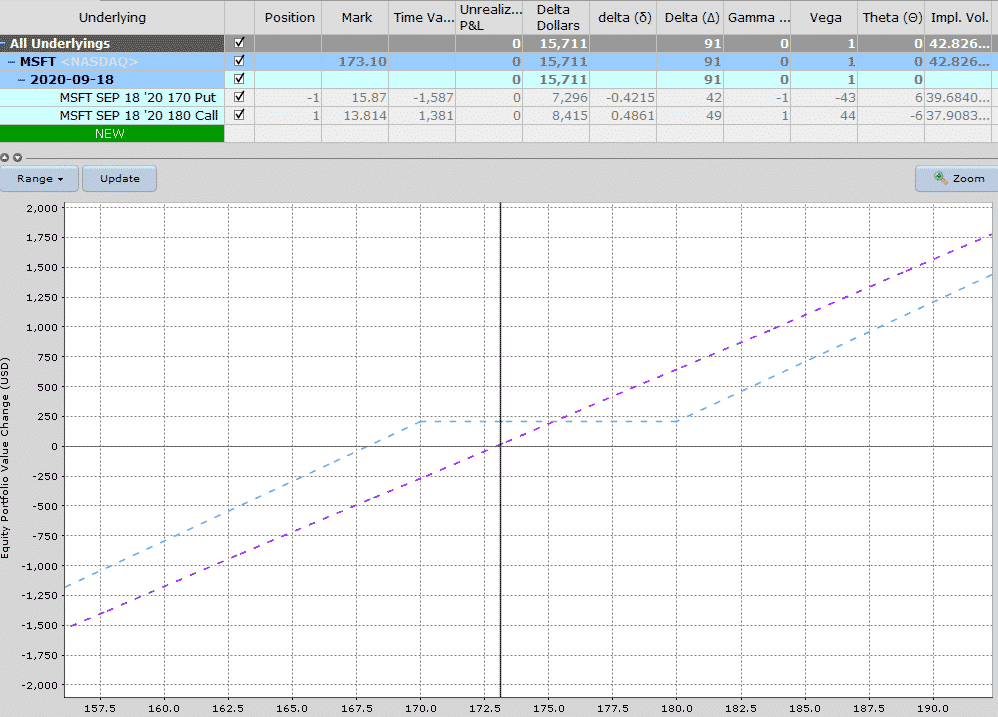

If we adjust the strikes slightly and buy a $180 call for $13.80 instead of a $175 call for $16.30, it results in receiving a premium of $207 instead of paying $43.

In this case the maximum loss would be $16,793.

Maximum Gain

The risk reversal strategy allows the opportunity for unlimited gains on the upside.

Using the second MSFT example above, once the stock passes $180, gains occur on a 1:1 basis. Every $1 rise in the stock results in a $100 gain for the risk reversal (at expiry).

There is also an income portion to the second trade because of the $207 in premium received.

The trade will make $207 profit if MSFT stays above $170 at expiry.

Breakeven Price

The breakeven price for a risk reversal depends on the strike placement.

In the first MSFT example above, a premium was paid to enter the trade.

The breakeven price is equal to the call option strike price plus the premium paid. $175 plus $43 equals $175.43

In our second example, a net premium was received for entering the trade. In this case, the breakeven price is the sold put strike price less the premium received. $170 less $2.07 equals $167.93.

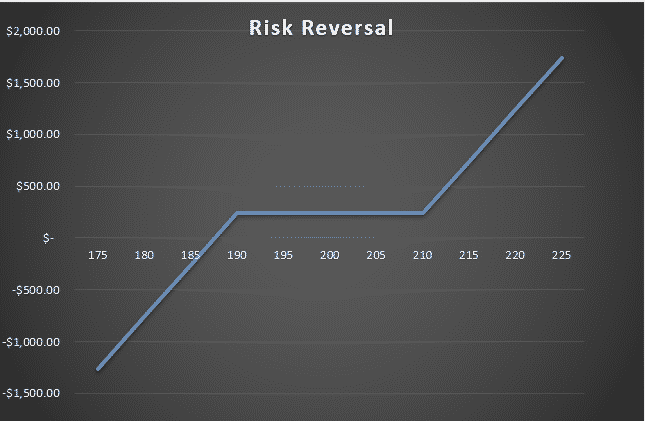

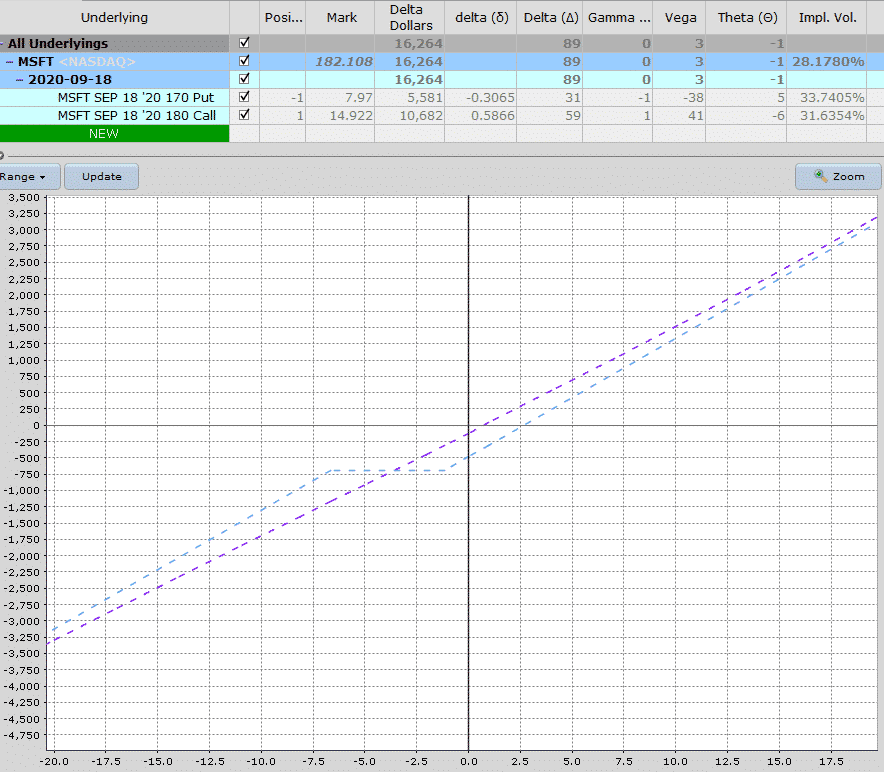

Payoff Diagram

The payoff diagram for a risk reversal is very similar to a long stock position other than the “flat bit” in the middle.

If MSFT stays between the short put and long call the profit or loss will be equal to the premium received / paid.

The benefit of this strategy is that the payoff is very similar to owning 100 shares of the underlying stock, but can be initiated for little to no cost or even for a credit. Just be aware of margin requirements.

Therefore, the position is similar to that of taking a leverage position in a stock.

It should be noted that even though you can enter this strategy and only need to cover the margin, losses can be substantial on the downside and are similar to owning 100 shares of the stock.

Traders should be aware of this and use appropriate position sizing.

Risk of Early Assignment

There is always a risk of early assignment when having a short option position in an individual stock or ETF. You can mitigate this risk by trading Index options, but they are more expensive.

Usually early assignment only occurs on call options when there is an upcoming dividend payment.

Traders will exercise the call in order to take ownership of the share before the ex-date and receive the dividend.

As this strategy contains long calls and not short calls, there is no risk of assignment on the call options.

Short puts can also be assigned early. The important thing to be aware of is that early assignment generally happens when a short option is in-the-money.

If the underlying stock used in the risk reversal strategy drops below the short put, traders need to be aware that they might be assigned on the put which would require them to purchase 100 shares of the underlying stock.

Risk Reversal Greeks

DELTA

Risk reversals are generally set up as bullish trades, although they can be placed as bearish trades as well.

A standard bullish risk reversal will have positive delta and a bearish risk reversal will have negative delta.

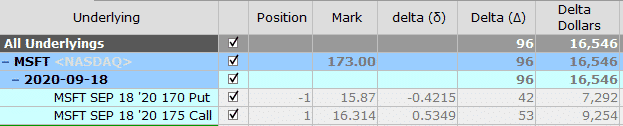

Looking at the first MSFT example, the position has a notional delta or delta dollars of 16,542.

That compares to a delta of 17,295 for a position of 100 shares. The delta of a risk reversal is very similar to owning 100 shares.

Both the short put and long call have positive delta in a bullish risk reversal.

The overall position delta is 96 which is very similar to the delta of 100 which would be the case when owning 100 shares.

A bearish risk reversal would have a negative delta similar to being short 100 shares.

GAMMA

Gamma is very low for a risk reversal, in fact it is almost non-existent.

In our MSFT example, the net Gamma is 0.03, very low indeed!

VEGA

Vega exposure is also quite low in a risk reversal. Sold puts have negative vega and long calls have positive vega.

In a risk reversal these two basically cancel each other out. In the MST example there is a very slight positive vega.

THETA

Theta is also very low in risk reversals. In both the MST examples, theta was shown as zero, but it would be something like -0.12.

If a net premium was received for the trade, the position would have slightly positive theta and benefit from time decay.

If the position resulting in a net premium being paid, theta would be negative and the position would lost a small amount of value each day.

Risk Reversal vs Long Stock

We’ve seen already when looking at the payoff diagram and the greeks, that a risk reversal is very similar to a long stock position.

The main difference between a risk reversal compared to a long stock position is the flat section in the middle of the payoff diagram.

A risk reversal is basically a synthetic long stock position where the trader can gain a similar exposure without having to lock up as much capital.

Advantages and Disadvantages of a Risk Reversal Strategy

The main advantages of a risk reversal strategy are that they can be implemented at little cost (sometimes no cost), they provide a trader with a favourable risk to reward ratio and they can be used to either hedge a position or double down on a bullish bet.

Another big advantage of a risk reversal is that it takes advantage of the natural volatility skew that occurs in the market.

Generally speaking, out-of-the-money puts trade with a higher implied volatility than the out-of-the-money calls.

As this trade involves selling the puts and buying the calls, that is advantageous to the trade because they are selling high volatility and buying cheap volatility.

This is why the trade usually results in a net credit being received because the calls are cheaper than the puts.

The main disadvantages of a risk reversal strategy are that the short leg may have high margin requirements and using a risk reversal to double down on a position could result in larger losses.

Risk Reversal Example

Using the MSFT example from earlier, the trade started out with MSFT trading at 173.10 and a month later the stock was trading at 182.

The risk reversal at this point was showing a profit of $900.

That’s basically the same return as holding 100 shares (182.10 – 173.10 x 100).

Conclusion

A risk reversal strategy provides traders with an effective way to manage some of the risks of a directional position or to double down on a directional position in a low-cost way.

It is executed by selling an out-of-the-money call or put option while simultaneously buying the opposite out-of-the-money option (i.e. one is a call, the other is a put).

A bullish risk reversal maintains a similar exposure to owning 100 shares of the underlying stock while a bearish risk reversal has a similar exposure to being short 100 shares.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Hi,

Thanks for the article. Let’s say I have 1000 shares of AMD, which is trading @ 90. I would like to do some hedge for the stock positions. So what expiration should I pick? and what strike of Sell Call ? what strike of Buy Put? Please help me with this, thanks!

Hi Penn, I can’t really give specific advice for regulatory reasons. But as a general example, I would want to go out about 3-4 months and strike placement would depend on how tight I want the hedge.

How would you roll a put to modify a risk reversal to avoid assignment? Also if you are long 1000 stock, and want to set up a risk reversal, does this entail selling the stock and then entering a risk reversal? To use this strategy if you are long the stock, I assume you’d to sell stock and create the position with availability of funds? If stock is owned partially on margin, can you typically use buying power to do a risk reversal? I ask because I made mistake of buying the calls before selling puts and was expensive lesson in execution! To this day I can’t figure out if it failed due to quick sale of stock and funds not clearing or due to cost of the calls taking more out of my buying power than anticipated. Thanks for your help!

Hi Josh,

I would keep an eye on the time value of the option, and if it gets too long as assignment is becoming a possibility, I would roll the put down in price, out in time or a combination of the two.

Depends on your goals, but yes if you want to convert your 1000 shares into a risk reversal, you would sell the shares and then trade 10 contracts of the risk reversal.

See below for info on buying power:

https://optionstradingiq.com/option-buying-power-explained/

For maximum loss , it’s a “good” thing if they are actions, not like oil that went in negative during corona times

Yes, that was pretty crazy wasn’t it?!