Contents

- What is Gamma Hedging?

- Why Should You Gamma Hedge?

- Who Gamma Hedges?

- Should I Be Worried About Hedging My Gamma?

- Bonus*** Using Delta to Hedge Gamma Risk

- Concluding Remarks

Today we’ll talk about gamma hedging, a trading strategy that you could implement to reduce risk in your portfolio.

Perhaps you’re familiar with delta hedging.

This is the process of buying or selling shares, or options, to maintain a consistent delta exposure on an options trade.

For those who trade volatility, delta hedging allows them to take a directionless view on an underlying as the trade progresses, isolating their point of view while controlling position risk.

The reason traders delta hedge in the first place is because of gamma, or the rate of change in delta for every dollar move at the spot price.

If gamma did not exist, one would not need to delta hedge at all.

So if delta hedging involves gamma, what is gamma hedging?

What is Gamma Hedging?

In delta hedging, a trader buys or sells shares to remain delta neutral.

In gamma hedging, a trader will buy or sell options to neutralize or hedge their gamma exposure.

Why Should You Gamma Hedge?

Gamma hedging reduces the risk of an options position.

To understand why one would want to gamma hedge, we first need to know how delta hedging falls short.

In a perfect world, we could hedge our deltas instantaneously.

This would negate the effect and risk of gamma.

However, we do not live in a perfect world.

Stock exchanges close daily, as well as on weekends and holidays.

Individual stocks are subject to further jump risk through events such as earnings, acquisitions and other news.

These frequent events cannot be simply delta hedged away.

Even indexes can be halted from trading in the most extreme of cases.

Due to this jump risk, it is impossible to remove the entire potential delta risk from options simply through delta hedging.

What gamma hedging does is help offset this risk by purchasing or selling gamma.

This is done by buying or selling options of other strikes and expiries.

If a large jump happens, a trader will lose money on their short gamma options but make money on their long gamma options.

Who Gamma Hedges?

First and foremost, gamma hedging is essential for market makers.

By providing liquidity, options market makers will tend to build up an inventory of certain strikes and combinations across an option chain.

These positions can be large.

Generally speaking, the market maker has no opinion on the direction of the stock.

Their goal is to make a fraction of the bid-ask spread simply.

Hence the market maker will attempt to be gamma neutral as well as delta neutral.

If you are curious who is buying a 10 cent call way out of the money, unless it is a meme stock, odds are it a market maker managing their greek exposure.

Both institutions and hedge funds will use gamma hedge.

For example, a fund may have a strategy of collecting variance risk premia on the S&P 500 by selling delta-neutral monthly straddles.

Despite this, delta hedging alone will not help them from going bankrupt if the index opens down 10% tomorrow.

So they may buy some far out-of-the-money weekly puts to hedge some of their gamma risk.

Individual retail traders often gamma hedge as well, though they may not know it.

Imagine I sell an out-of-the-money delta 10 call on AMC.

I am feeling lucky and wanting to collect the premium. Bad news, and the stock rallies 30% the next day.

Let’s say I still think the position will go down, but I understand it could continue to go up, and the gamma has made the delta now worrisome.

So I now buy a few further out-of-the-money calls.

Congratulations, you are not only a delta hedger but a gamma hedger as well!

Should I Be Worried About Hedging My Gamma?

At this point, it is important to know if you should be hedging your gamma.

The first question to ask yourself is how much gamma do you have.

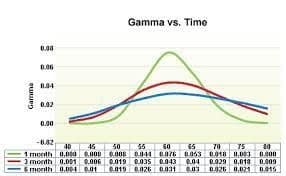

The below chart can be a help.

Source: Options Education Org

We can see that Gamma is highest for close expirations that are at the money.

Hence for conservative investors selling options a few months in advance, delta hedging alone is probably sufficient.

Additionally, their gamma exposure may be negligible or positive for investors who buy and sell options.

Gamma hedging is generally not needed for a position with positive gamma, which illustrates a potential asymmetrical positive payoff for the individual.

Yet if you are selling short-dated options with large amounts of capital, gamma hedging is not only smart but essential to staying in business.

Attempting to being gamma neutral sounds like a good goal but remember this.

To get paid in a trade, we need to take risks.

We are long theta if we are short some gamma.

We run the risk of not expressing a trade if we neutralize our gamma.

While a market maker can do this, they are not in the same business as us.

For the average retail trader, attempting to run a high-frequency book will result in more commissions and a strategy with no alpha.

If you are worried about gamma risk, a few solutions do not involve gamma hedging.

- Go out further in time, do not trade weekly options frequently.

- Have smaller positions

- Have positions both long and short options

Tip* Checking the gamma of your position is usually easy using your brokerage account. If you cannot find it, most option price calculators will also show the gamma of an option contract.

Bonus*** Using Delta to Hedge Gamma Risk

Sometimes the best way to hedge gamma risk can be through delta.

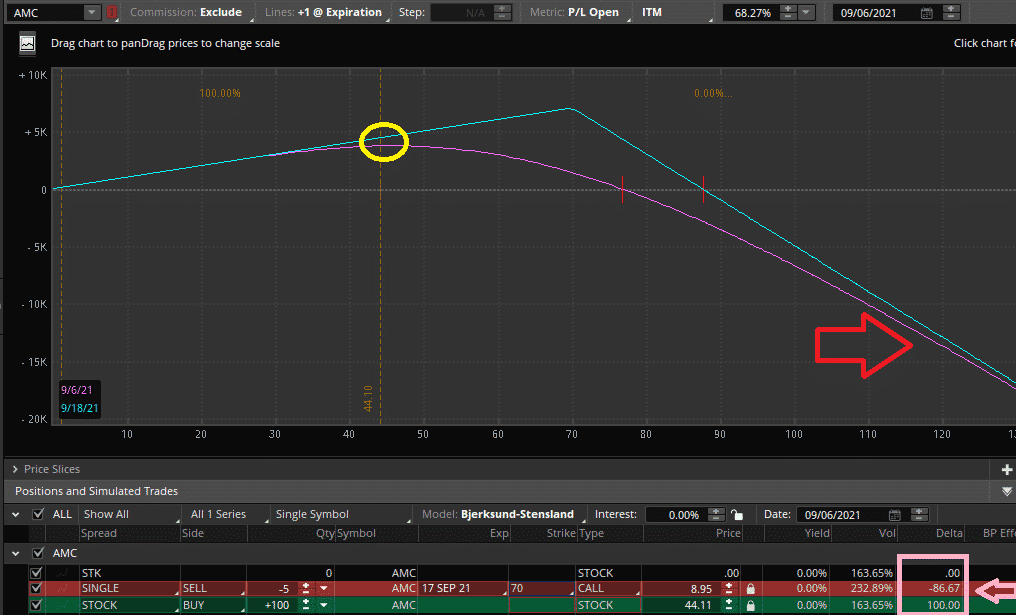

Let’s take a look at selling some weekly out-of-the-money calls on AMC.

Here I have sold five 70 Calls and am long 100 shares.

We can see at the bottom of our graphic we are basically delta neutral.

Though are we risk-neutral?

We can see if the stock goes down, we cannot lose any money.

Yet if the stock jumps to 100, we are in serious problems.

We might use call options to gamma hedge our position.

Nevertheless, if our view was that the 70 calls are overpriced, odds are the 80 calls are as well.

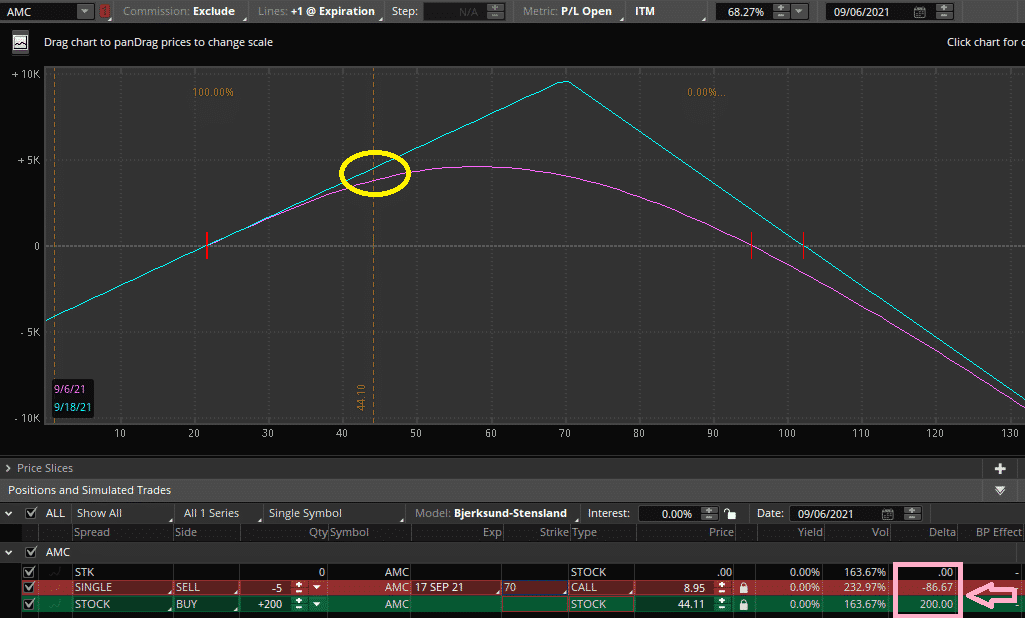

What if we over hedged our shares?

Let’s have a look below.

We now have a delta of over 100, but ironically, the position has far less tail risk.

While we can now lose money to the downside, the price can still only go to zero.

On the upside, even at $100 on expiration, we still make money.

The reason for this is intuitive. We are selling 17 delta calls.

They can only go to a delta of zero while they can go all the way to a maximum delta of one hundred.

Additionally, our short gamma will become the highest risk if we approach the 70 strike.

Overhedging is an example of one strategy we can use to protect against gamma risk preemptively.

Concluding Remarks

Gamma hedging is the process by which traders neutralize gamma by the buying and selling of options.

Gamma hedging is important due to jump risks where conventional delta hedging is unable to fully mitigate risk.

Depending on your trading style, gamma hedging will vary in importance.

For investors solely trading longer-dated options, delta hedging will usually suffice.

Conversely, gamma hedging can become very important for traders who like to trade large positions on shorter-dated options.

Even though most investors do not require gamma hedging, being aware of the gamma in your portfolio can help you develop stronger positions and avoid taking on excessive risks.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Hi Gavin,

Good post on an important matter.

The first graph (“option gamma hedging”) is not working (at least in my browser).

Regards.

Now is working perfect. Evidently an issue on my side. Ignore in my comment the “bug report” part.

Good article on an important subject.

Regards

Thanks. I appreciate your comments.

Great post! Thanks for this. I’ve been trying to get a decent explainer on this topic.

Glad you liked it Garry.

Hey Gavin, great post! Can you please write a blog on how to optimally keep delta and gamma risk same in shorter dated options’ portfolio? Thanks!

P.S. : The website UI is amazing,

Thanks for the suggestion, I will add that to my list. Glad you like the website.