Options get a bad rap sometimes and for good reason.

If you don’t know what you are doing you can really lose your shirt.

However, when you do understand them and have enough experience, you will realize they are an incredibly flexible tool to enhance your portfolio.

Covered calls are a reasonably low risk way for investors to get started with options.

There is a natural progression for an investor who is already accustomed to share ownership to begin to explore the fabulous world of covered calls.

The key is to educate yourself, and practice, practice, practice.

Contents

-

- Why Don’t People Know About Covered Calls

- How Do Covered Calls Work?

- Why Sell An Option On Your House?

- Covered Calls On Stocks

- Understanding the Covered Call Payoff

- How to Choose the Right Strike Price

- Weekly vs Monthly Covered Calls

- What Happens When Your Covered Call Is Exercised (Assignment)

- When NOT to Sell Covered Calls

- Covered Calls for Retirement Income

- FAQ

- Related Articles

Why Don’t People Know About Covered Calls

Covered calls are not something you learn about in school.

In fact, schools don’t really teach you anything about personal finance or investing.

This is one of the great failings of our education system.

Someday I hope I can help rectify that.

Covered calls are one of the greatest wealth creation tools you can find.

How Do Covered Calls Work?

One way to teach investors about covered calls is to use property as an example.

Most people understand the property market very well so this makes it an easier introduction into the world of covered calls.

Assume Investor A just bought a house for $200,000.

Investor A then turns to Investor B and says he will sell the house to him anytime in the next 6 months for $210,000.

Investor A is selling an option on the house to Investor B.

For selling this option Investor A receives a fee of $5,000.

Investor A still owns the house and Investor B has the right to buy it for $210,000 any time in the next 6 months.

Investor A gets to keep the $5,000; that’s his no matter what happens over the next 6 months.

The property value could go to $250,000 or it could go to $150,000, but either way, Investor A pockets the $5,000.

Let’s look at how things would play out in these examples:

If the property value drops to $150,000, do you think Investor B will want to exercise his right to buy it for $210,000?

You bet your bottom dollar he won’t.

Not unless he wants to be $60,000 in the hole.

Instead, Investor B will walk away and thank his lucky stars he only lost $5,000 which is a lot better than the outcome for Investor A.

Investor A is still the owner of the house, but it’s now worth $50,000 less than he paid for it. But, that loss has been cushioned slightly by the $5,000 he received from Investor B.

Investor A is slightly better than someone else who bought an identical property.

Investor A can potentially sell another option on the house, but in order to receive a similar fee of $5,000, he might have to agree to sell the house for $155,000 rather than $210,00 which isn’t a very attractive proposition.

If he wanted to sell an option on the house at $210,000 I don’t think many investors would want to pay much more than about 5 bucks for that right!

If the property does not change in value over the next 6 months, Investor B will not want to buy it for $210,000.

Investor A maintains ownership of the property and Investor B is left with a worthless option that has expired.

Investor A has made a handy return of 2.5% on a house that has not changed in value.

AND, he can potentially sell another option for $5,000 provided there is a willing buyer.

If the property value rises to $250,000 will Investor B want to exercise his right to buy at $210,000? Of course he will.

He will be sitting on some nice equity of $35,000 from the word go.

Upon closing, Investor B’s total outlay to purchase the house will be $210,000 plus the $5,000 he paid for the option.

What happens if Investor B doesn’t want to take ownership of the house?

Maybe he can’t get a mortgage for a $210,000 property.

What happens in this case?

Would he just miss out?

What he could do rather than exercise his option, is sell it on to another investor.

In this case, if the house is valued at $250,000 and he can buy it for $210,000 then a fair price for his option would be $40,000.

Investor B’s profit is the same either way: $35,000.

Investor A has made a decent return as well, but he might be kicking himself for selling the option.

If he hadn’t sold the option, he could sell the house on the open market for $250,00.

Instead, he has an obligation to sell to Investor B for $210,000.

Investor A has still made a profit of $15,000 due to the $10,000 of capital gain and $5,000 received for the option premium.

But this return of 7.50% is less than the 25% return he would have achieved had he not sold the option.

Why Sell An Option On Your House?

Why would Investor A sell the option on his house? Well, there are a few reasons:

- Income – By selling the option, he is generating income on his asset. The ideal scenario for Investor A would be for the house price to rise to $210,000. In this case, the cost for Investor B of exercising his option would outweigh the benefits. Investor A has made a $15,000 profit and still owns the property over which he can sell another option.

- Some Capital Protection – By selling the option, Investor A has limited his downside risk, but only by a little bit. When the house price dropped to $150,000, Investor A lost $45,000. That’s still a painful loss, but it was cushioned somewhat by the $5,000. The breakeven price for Investor A is $195,000. At the end of the 6 months, he can sell the house at that price at walk away with zero loss.

Investor B’s motivation in this transaction is capital gains.

He’s looking for the house price to go up significantly in value so that he can make a tidy profit having only had to put down $5,000.

Covered Calls On Stocks

Hopefully now you’ve grasped the key concepts.

Covered calls on stocks work exactly the same was an in our property example.

With stocks you even get the added benefit of being paid dividends! Let’s look at an example.

XYZ stock is trading at $100. You own the stock and don’t think it’s going much higher.

You want to increase your income potential so you decide to sell a call option with a strike price of $100.

The buyer of the option, takes the other side of your trade and is bullish on the stock.

They think it’s going up beyond $100.

For the right to buy the stock for $100, the option buyer pays you a premium of $5.

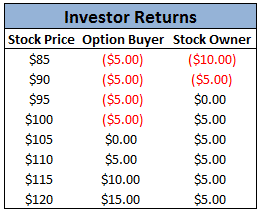

Let’s look at some scenarios:

- Stock goes to $85

The buyer of the option will walk away and lose 100% of his $5 investment.

You will still own the stock, but are sitting on a loss of $10 which is better than the $15 loss you would have if you hadn’t sold the call option.

- Stock stays at $100

The buyer of the option will walk away and lose 100% of his $5 investment.

In theory he could exercise the option if he wants to own the shares, but it is easier to just buy them directly in the market.

Note: Most brokers will automatically exercise an option if it is 1 cent in the money.

So, if the stock closes at $100.01 the option would be automatically exercised.

You are happy because you have made a $5 return on a stock that has gone sideways thanks to the option premium.

- Stock goes to $105

The option buyer will either exercise his option and buy the shares for $100 or sell the option in the open market.

If he buys the shares for $100, he can turn around and sell them in the market for a $5 gain.

But, he paid $5 for the option, so his profit is zero.

Alternatively, he can sell his option for $5 in the open market.

Either way, he has made a breakeven trade.

You are happy because you have made a 5% return, the same as if you had just held the stock.

- Stock goes to $115

If the stock goes to $115, both investors are happy, although you are a bit disappointed you didn’t just hold the shares outright.

You still make your $5 profit and 5% return, but you have left another $10 on the table.

The option buyer is happy because he can purchase a $115 stock for only $100 (don’t forget he also paid the $5 in premium, so his total cost is $105).

Or he can sell the option for $15. That’s a $10 profit on a $5 investment.

The table below shows the outcome for each investor at different stock prices.

Remember to multiply these amounts by 100 given that each option contract controls 100 shares.

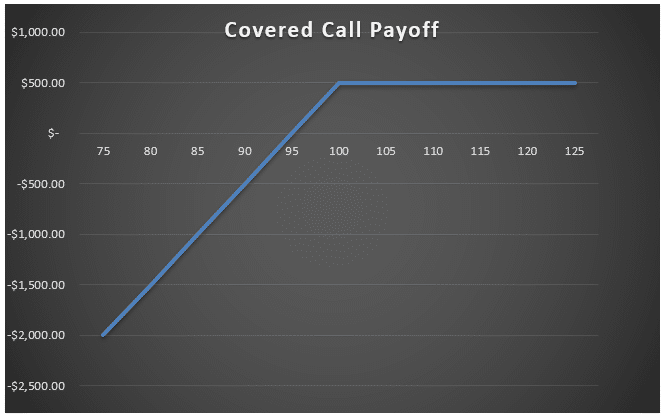

Understanding the Covered Call Payoff

The payoff profile of a covered call is one of the most important things to understand before placing your first trade. Here’s the simple formula:

Maximum profit = (Strike price − Stock purchase price) + Premium received

Breakeven = Stock purchase price − Premium received

Maximum loss = Stock purchase price − Premium received (i.e. the stock goes to zero, slightly cushioned by the premium)

Using our XYZ example: stock purchased at $100, $100 strike call sold for $5.

- Maximum profit = ($100 − $100) + $5 = $5 per share ($500 per contract)

- Breakeven = $100 − $5 = $95

- Maximum loss = $95 per share if the stock goes to zero

The key insight: the premium collected lowers your effective cost basis in the stock.

Every covered call you sell reduces your breakeven slightly further.

How to Choose the Right Strike Price

Strike selection is where covered call trading shifts from concept to craft.

There are three basic approaches, each with different trade-offs:

At-the-money (ATM) calls — Strike equals or is very close to the current stock price.

Collects the most premium of the three approaches but has the highest probability of assignment. Use when you’re comfortable selling the stock at the current price and want maximum income.

Out-of-the-money (OTM) calls — Strike is above the current stock price.

Collects less premium but allows for some capital appreciation before assignment.The most commonly used approach for income traders who want to retain upside.Typical targets are around 20–30 delta.

In-the-money (ITM) calls — Strike is below the current stock price.

Provides the most downside protection but immediately caps your upside and almost guarantees assignment. Used primarily as a defensive move when you want to exit a position or reduce risk on a stock that’s declined.

For most income traders the sweet spot is a slightly OTM strike at a roughly 20–30 delta. That collects meaningful premium while leaving room for the stock to appreciate before being called away.

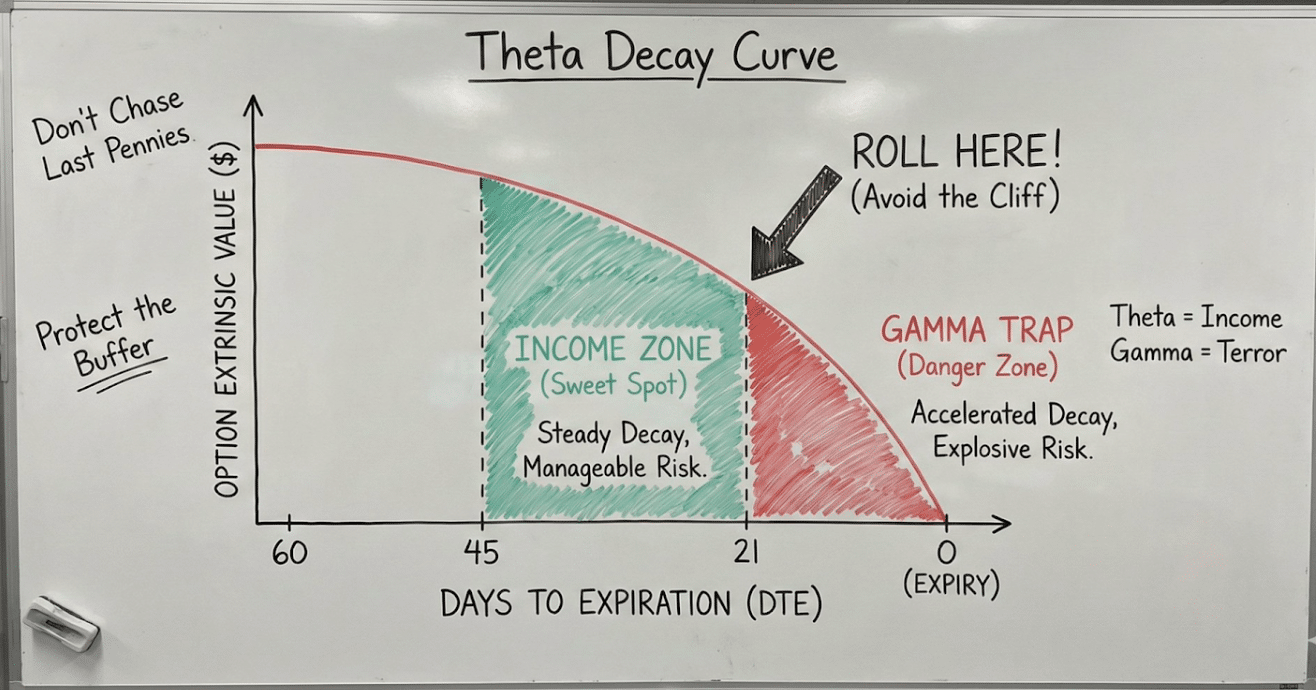

Weekly vs Monthly Covered Calls

One of the most common questions from new covered call traders is whether to sell weekly or monthly options.

The short answer: monthly (30–45 days to expiration) is usually the better starting point.

Monthly options capture the steepest part of the theta decay curve, the period where an option loses value fastest, while limiting transaction costs and management time.

Selling weekly options generates higher annualised premium in theory, but requires more active management, accumulates more commissions, and increases the risk of being whipped in and out of positions by short-term volatility.

Weekly covered calls do have a place for experienced traders who are actively managing a large portfolio of positions and want more frequent premium collection opportunities. But for most investors running a covered call strategy on a handful of stocks, monthly options are the more practical and cost-efficient choice.

See our dedicated guide on weekly vs monthly covered calls for a full comparison.

What Happens When Your Covered Call Is Exercised (Assignment)

Assignment happens when the buyer of your call option chooses to exercise their right to buy your shares at the strike price. Here’s exactly what happens:

Your 100 shares are automatically sold at the strike price.

The transaction settles in the normal settlement period (T+1 for US equities). You keep the premium you received when selling the call, that’s yours regardless.

Your position is now flat. You no longer own the shares or the short call.

Assignment can happen at any time before expiration (American-style options), but in practice it most commonly occurs at or near expiration when the option is in-the-money.

The main exception is around ex-dividend dates.

If your short call is in-the-money and the stock has an upcoming dividend, there is a risk of early assignment as the option buyer exercises to capture the dividend.

It’s worth checking ex-dividend dates before selling calls on dividend-paying stocks.

After assignment, you can start fresh.

Either buy the shares back if you still want exposure to the stock, or move on to a different position.

If you’re running a systematic strategy, assignment is simply part of the process, not a problem.

When NOT to Sell Covered Calls

Covered calls are not appropriate in every situation. Knowing when to hold off is as important as knowing how to execute the strategy.

When you’re strongly bullish.

If you believe a stock is about to make a significant move higher, selling a covered call caps your upside. Sometimes the better trade is to simply hold the stock and let it run.

On highly volatile stocks before earnings.

Implied volatility spikes around earnings, which makes premiums look attractive, but the same volatility can cause the stock to gap well beyond your strike, leaving you with a large unrealised loss on the shares while your call gets exercised.

When the premium isn’t worth the risk.

If a stock has very low implied volatility, the premium available may be so small that it doesn’t justify the trade. A 0.3% return for 30 days isn’t worth tying up capital and managing a position.

On stocks you’re not comfortable holding long-term.

The covered call strategy requires you to remain calm if the stock declines, because you’re going to keep selling calls against it while you wait for recovery. If you wouldn’t be comfortable holding a stock through a 20–30% drawdown, don’t use it for covered calls.

Covered Calls for Retirement Income

Covered calls are one of the most widely used options strategies for retirement income, and for good reason.

They generate consistent cash flow from assets you already own, without requiring you to sell your holdings.

The most common approach for retirement investors is to hold a portfolio of quality, dividend-paying stocks, or low-cost ETFs like SPY, QQQ, or sector ETFs, and sell slightly OTM calls against them each month.

The combined income from dividends and call premiums can significantly enhance the yield on a conservative portfolio.

For Australian investors using a Self Managed Super Fund, covered calls are one of the strategies most commonly approved for use within an SMSF, though trustee obligations and documentation requirements apply.

See our guide on trading options in an SMSF for the specifics.

The main risk to understand before using covered calls for retirement income is that the strategy doesn’t protect against large drawdowns.

The premium collected offers limited cushioning.

If a stock falls 30%, the $200 you collected in premium doesn’t change the fundamental loss.

Stock selection and position sizing matter more than the options mechanics when running covered calls in a retirement context.

For a complete framework on using covered calls as part of a retirement income strategy, see our guide on options income strategies for retirement portfolios.

We also have lots of video on Covered Calls on our Youtube Channel.

FAQ

What Is A Covered Call?

A covered call is an options trading strategy in which an investor sells a call option on an underlying asset that they already own.

The call option provides the buyer with the right, but not the obligation, to purchase the underlying asset from the seller at a predetermined price (strike price) before a specified expiration date.

By selling the call option, the investor receives a premium, which provides some downside protection in case the underlying asset’s price falls.

What Are The Benefits Of Covered Calls?

The benefits of covered calls include generating additional income through option premiums, reducing downside risk on an underlying asset, and potentially realizing gains on the underlying asset’s appreciation up to the strike price.

What Are The Risks Of Covered Calls?

The risks of covered calls include potentially missing out on additional gains if the underlying asset’s price rises above the strike price, being forced to sell the underlying asset at the strike price if the call option is exercised, and potentially losing money if the underlying asset’s price falls below the breakeven price.

How Do You Select The Right Strike Price For A Covered Call?

Selecting the right strike price for a covered call depends on your goals and risk tolerance.

A lower strike price will typically provide a higher premium and more downside protection, but also limit the potential upside if the underlying asset’s price rises significantly.

A higher strike price will typically provide a lower premium and less downside protection, but also allow for greater potential gains if the underlying asset’s price rises significantly.

What Are Some Tips For Implementing A Covered Call Strategy?

Some tips for implementing a covered call strategy include selecting an underlying asset that you are comfortable holding long-term, considering the impact of taxes and transaction costs on your returns, and regularly monitoring the underlying asset’s price and the option’s expiration date to decide whether to roll the option forward or let it expire.

Can you lose money selling covered calls?

Yes, the most common way to lose money with covered calls is through a decline in the underlying stock. The premium collected provides only a small amount of downside cushion. If XYZ stock falls from $100 to $60, the $5 premium you collected reduces your effective loss from $40 to $35 per share. That’s meaningful, but not protection against a large drawdown. The covered call doesn’t protect you from serious stock losses; it only generates income in flat or mildly bullish conditions.

What is a good covered call premium to collect?

A commonly cited target is 1–3% of the stock’s value per month, though this depends heavily on implied volatility. In a high-volatility environment you can collect significantly more; in a low-volatility environment like 2017 or mid-2024, 1% monthly may be difficult to achieve without selling very close to the money. Rather than targeting a specific premium amount, focus on collecting premium at a strike you’d genuinely be comfortable selling the stock at — the dollar amount follows from that.

What is the best delta for covered calls?

Most systematic covered call traders target a short call delta of 20–30. At 20 delta, the call has roughly a 20% probability of being in-the-money at expiration, meaning you’ll be assigned on about one in five trades. At 30 delta you collect more premium but face a higher assignment rate. Exactly where you land in that range depends on your income target, your willingness to have shares called away, and how bullish you are on the underlying stock.

Should I sell covered calls weekly or monthly?

Most income traders use 30–45 day expirations for covered calls. This range captures the steepest theta decay while limiting transaction costs and active management time. Weekly covered calls generate higher annualised premium in theory, but require significantly more management, accumulate more commissions, and increase whipsaw risk. Unless you’re actively managing a large portfolio and comfortable with weekly position reviews, monthly expirations are the more practical starting point.

Are covered calls suitable for an SMSF?

Covered calls are one of the options strategies most commonly permitted within an Australian SMSF, as the risk is clearly defined and the position is covered by existing share holdings. However, specific trustee documentation, strategy rules, and SMSF deed requirements must be met before trading. See our dedicated guide on trading options in an SMSF for the full requirements.

Related Articles

Selling Covered Calls – A Detailed Guide

How To Write Covered Calls: 2024 Ultimate Guide

Weekly Versus Monthly Covered Calls

How To Make Money With Covered Calls

When to Roll Covered Calls

Selling Deep In The Money Covered Calls: Why Do It?

Covered Calls For Dummies

Covered Calls With LEAPs Options Strategy

Supercharge Your Covered Calls Using LEAPS

Selling Weekly Covered Calls

Covered Calls: How to Adjust to Changing Market Conditions

Take Your Covered Call Strategy Further

Covered calls are the starting point for a systematic income approach — but the real power comes when you combine them with cash-secured puts and the wheel strategy into a complete income portfolio. Options Income Mastery covers the complete system: how to select underlyings, time entries, manage positions, and build consistent monthly income across different market conditions.

We hope you enjoyed this article on Covered Calls.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

The analogy of the property was very helpful. The property represents the underlying (XYZ stock). Since investor A owned the property, the property is the covered property (covered stock). The owner of the property wrote the contract — he is the seller of a call option, which means, he wants the price to go down. The seller(writer) wants the value of the property to decrease. The buyer of the call option wants the value of the property to increase

Yep spot on.

It doesn’t necessarily seem like I would want the stock to go down. Wouldn’t I have lost the option to bail on the stock?

If the stock goes down below your stop loss, you can still sell the shares and buy back the short call to close the entire position. Hope that helps. If you have any other questions, let me know.

Confusing, as I am trading options.

Hi Tom, what were you finding confusing? Happy to help if I can.

It has to do with confusion with the LONG CALL vs. Covered Call.

The LONG CALL is covered w/DEEP MATH. Although the math is not complicated, it requires several “inputs” from sources that change frequently.

I believe this since (I accidentally sold one recently and it looks like I will make a small profit). You have done a lot to help me and others which is very much appreciated. I’ll keep working on the LONG CALL and hope a calculator (or computer program is quickly constructed), again, THANKS!!!

in your examples above, if the stock is $ .01 above the strike price. the option will be exercised… if it is at the exact strike price, $ 100, it will not exercise, correct?

Yes, that’s right.

Attn: Gavin

To your reply in Todd’s case. How do you go about buying back the short call to close the entire option?

Hi T.j, you simply place a Buy to Close order. Basically the opposite of what you did to open the position (sell to open). Send me an email if you need more details.

What would i do in this case I’m Canadian so my stocks are Canadian my option is 1 BB September 15 strike 7.00 stock is now 7.22 my date is closing soon I think I should sell option @.50 then buy back to close how would that look with strike price and expiration

Not sure I can provide much help in this situation. Sorry.

Now that I have joined your class and benefited from your presentation on Zoom all of this is definitely becoming clearer, – phew! and Thank you!

Glad to hear it Betsy! Lots more good stuff to come over the coming weeks too!

How About rolling up as. The sold call gets in the money?

Yes you can do that, particularly if you want to hold on to the stock.

i would like to attend an option class. Where do I search?

Hi Marty, the next course will be open very soon. If you sign up to my email list, that is the best place to get notified. You can sign up here:

https://optionstradingiq.lpages.co/best-of-iq/

Hi Gavin,

I generally trade options on a daily basis and have a few stocks where I own 100 or more shares. I want to supplement my trading with covered calls. Is there an optimal stock price to focus on for covered calls as I am seeing very low premiums for stocks that are <$20.

many thanks!

Tough to get much premium on low priced stocks. In order to get any premium, you might have to look at longer-term options, maybe 6-9 months in duration.

What tool do you use to find the best premium/company for cc’s?

Barchart.com scanners are the best