Master the delta theta ratio to optimize your options portfolio for maximum theta decay while minimizing directional risk.

Learn the ideal 0.5 ratio target, how it varies by strategy (iron condors, butterflies, credit spreads), and when to adjust based on volatility conditions.

Contents

-

- What Is The Delta Theta Ratio?

- Why Delta Theta Ratio Matters for Income Traders

- The Ideal Delta Theta Ratio: Tom Sosnoff’s 0.5 Rule

- How Volatility Affects Delta Theta Ratio

- Delta Theta Ratio by Strategy

- Strike Selection and Delta Theta Ratio

- Time to Expiration Impact on Delta Theta Ratio

- How to Calculate Delta Theta Ratio

- When to Adjust Based on Delta Theta Ratio

- Index Options vs Individual Stocks

- Delta Theta Ratio Management Rules

- Common Delta Theta Ratio Mistakes

- FAQs About Delta Theta Ratio

- Conclusion: Mastering Risk-Reward Balance

What Is The Delta Theta Ratio?

The delta theta ratio is a critical metric that measures the balance between directional risk (delta) and time decay profit (theta) in an options position.

Simple Definition:

Delta Theta Ratio = Delta ÷ Theta

For example:

- Position delta: -12

- Position theta: +30

- Delta theta ratio: 12 ÷ 30 = 0.4 (or 40%)

What Each Component Means:

Delta:

- Measures directional exposure

- Represents approximate dollar change per $1 move in underlying

- Higher delta = more directional risk

- Lower delta = more neutral position

Theta:

- Measures time decay profit

- Represents dollar gain per day from passage of time

- Higher theta = more daily income

- Lower theta = less time decay benefit

The Ratio:

- Lower ratio = more income relative to directional risk (ideal for non-directional traders)

- Higher ratio = more directional risk relative to income (less ideal)

- Target: 0.5 or lower for premium selling strategies

Why Delta Theta Ratio Matters For Income Traders

The non-directional trader wants to hedge delta to make it delta-neutral and have theta as large as possible.

In theory, they want the delta theta ratio to be zero.

Why This Matters:

- Risk-Reward Optimization A proper delta theta ratio ensures you’re getting adequately compensated (theta) for the directional risk (delta) you’re taking.

- Portfolio Stability Lower ratios mean your portfolio won’t get whipsawed by every market move. Your P&L is driven more by time decay than price movement.

- Predictable Income When delta is low relative to theta, your daily returns become more predictable and less dependent on market direction.

- Strategic Positioning The ratio helps you decide:

• Which strikes to select

• When to adjust positions

• Whether to add or reduce exposure

• How to balance multiple positions

The Challenge:

In practice, a zero delta theta ratio is not achievable because:

- Delta changes continuously as the underlying price moves

- You don’t want to be constantly over-adjusting positions

- Transaction costs make frequent adjustments expensive

- Some directional exposure is inevitable in real trading

This is why experienced traders target a 0.5 ratio rather than zero—it’s achievable and sustainable while still maintaining excellent risk-reward characteristics.

The Ideal Delta Theta Ratio: Tom Sosnoff’s 0.5 Rule

So what is the ideal delta theta ratio in practice?

Tom Sosnoff of TastyTrade was asked a similar question at a symposium when he answered:

“A lot of this depends on where the markets are based on current levels of implied volatility.”

Sosnoff’s Framework:

In Low Volatility Environments:

At the time Sosnoff gave his answer, market volatility was low, which means lower theta and higher delta-theta ratios. He explained:

“Our deltas are much higher than our thetas right now.

Because I don’t feel the risk in short premium is worth the reward because volatility is so low.

So our deltas are 2 or 3X our theta right now.

That’s not a perfect world. That’s exactly what you don’t want.”

Translation: When volatility is crushed, you might accept a 2.0-3.0 delta theta ratio because:

- Premium is too small to justify the risk

- You need larger positions (higher delta) to generate meaningful income

- Time decay (theta) is naturally lower in low IV environments

In Normal to High Volatility:

Sosnoff continues with his ideal scenario:

“In a perfect world, you would much prefer your deltas about half of your theta.”

Translation: Target a 0.5 delta theta ratio (delta is 50% or less of theta) when market conditions allow it.

The 0.5 Rule Explained:

What It Means:

- For every $50 of theta, keep delta at $25 or less

- For every $100 of daily time decay, maintain delta below $50

- Your income potential should be 2X your directional risk

When It’s Achievable:

- Index options (SPX, RUT, NDX) more than individual stocks

- Normal to elevated volatility environments

- Positions with 20-45 days to expiration

- Properly structured iron condors and butterflies

When It’s Not:

- Extremely low volatility (VIX < 12)

- Very short-term trades (< 7 days)

- High-conviction directional trades

- Individual stock options with wide bid-ask spreads

Master The Greeks

Understanding delta theta ratio is just one piece of systematic options trading:

View Our Free Options Trading Resources – Learn how to analyze and manage the Greeks for more consistent returns.

How Volatility Affects Delta Theta Ratio

Implied volatility has a massive impact on your delta theta ratio, and understanding this relationship is crucial for proper position sizing.

High Volatility Environment:

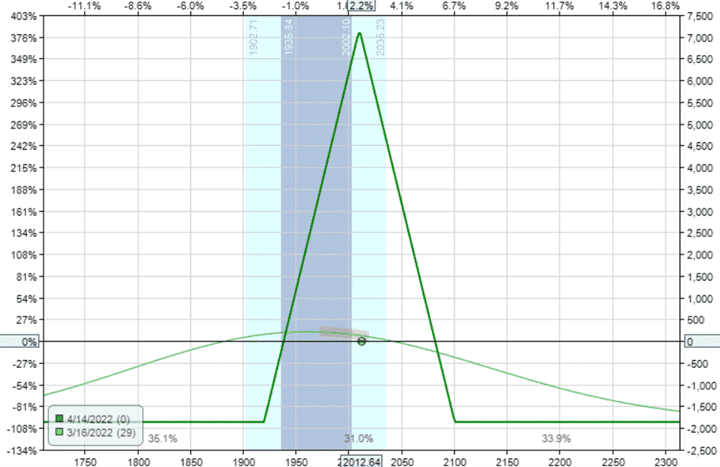

Example: March 16, 2022 (RVX at 33, VIX at 29)

Bull put spread on RUT with 29 days to expiration:

- Buy two April 14 RUT 1835 puts

- Sell two April 14 RUT 1840 puts (18-delta short strike)

Greeks:

- Delta: 1.12

- Theta: 2.59

- Vega: -5.86

- Gamma: -0.01

Delta/Theta Ratio: 1.12 ÷ 2.59 = 0.43 (43%)

This is excellent and well below the 0.5 target.

The elevated volatility produces higher theta relative to delta.

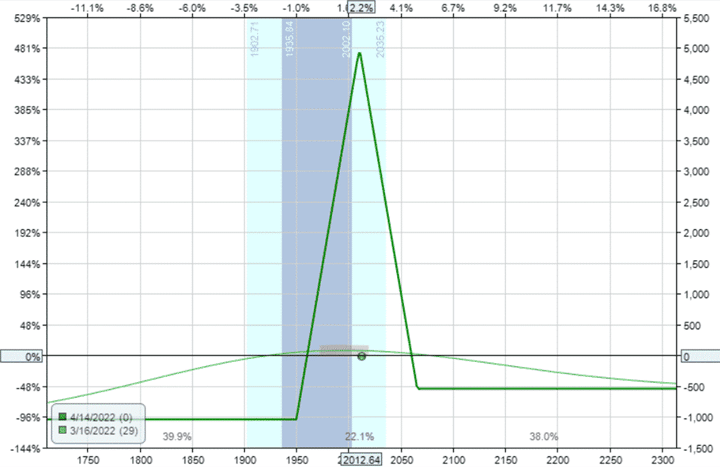

Low Volatility Environment:

Example: January 4, 2022 (Lower Volatility)

Similar bull put spread on RUT with similar parameters:

- Buy two February 4 RUT 2110 puts

- Sell two February 4 RUT 2115 puts

Greeks:

- Delta: 1.25

- Theta: 2.11

- Vega: -7.78

- Gamma: -0.01

Delta/Theta Ratio: 1.25 ÷ 2.11 = 0.59 (59%)

The ratio jumped to 59%, above our ideal 0.5 target. In low volatility, you get less theta for the same directional risk.

Key Insights:

High IV = Better Ratios

- More premium available

- Higher theta for similar delta

- Easier to achieve 0.5 ratio or lower

- Better risk-reward for premium sellers

Low IV = Worse Ratios

- Less premium available

- Lower theta relative to delta

- Harder to achieve ideal ratios

- Consider waiting or taking smaller positions

Practical Application: This is why experienced traders become more aggressive in high volatility and more selective in low volatility.

The math literally tells you when conditions favor premium selling.

Delta Theta Ratio by Strategy

Different options strategies produce vastly different delta theta ratios.

Understanding these differences helps you select the right strategy for your market outlook and risk tolerance.

Bull Put Spreads

Bull put spreads are inherently directional but can still maintain reasonable delta theta ratios.

Example: March 16, 2022

- RUT @ $2013

- Buy two April 14 RUT 1835 puts

- Sell two April 14 RUT 1840 puts (18-delta short strike)

- 29 days to expiration

Greeks:

- Delta: 1.12

- Theta: 2.59

- Delta/Theta Ratio: 0.43

This is an excellent ratio for a directional spread.

You’re getting $2.59 of daily theta for only $1.12 of directional exposure.

If Positioned Closer To The Money:

Moving the short strike to 30-delta (closer to the money):

Greeks:

- Delta: 1.74

- Theta: 1.68

- Delta/Theta Ratio: 1.04

The trade becomes much more directional.

As you move closer to the money:

- Delta increases significantly

- Theta increases, but not proportionally

- Vega becomes more dominant

- Risk-reward deteriorates for non-directional traders

Key Takeaway: For bull put spreads, keep short strikes at 15-20 delta to maintain favorable delta theta ratios around 0.4-0.5.

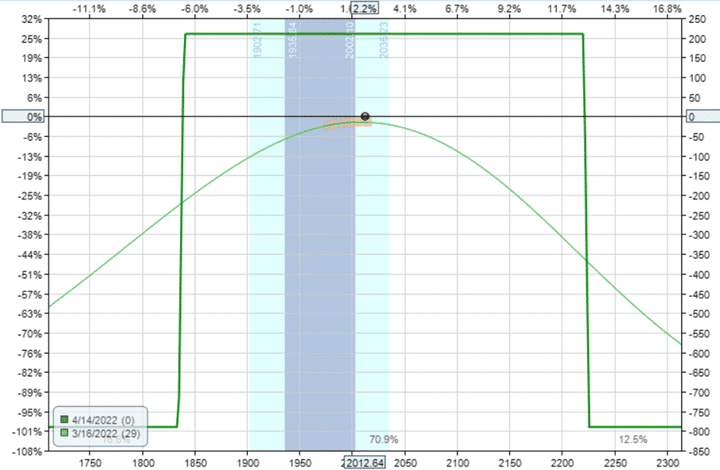

Iron Condors

Iron condors are the gold standard for achieving ideal delta theta ratios.

Example: March 16, 2022

- RUT @ $2013

- Buy two April 14 RUT 1835 puts

- Sell two April 14 RUT 1840 puts (18-delta)

- Sell two April 14 RUT 2220 calls (8-delta)

- Buy two April 14 RUT 2225 calls

Greeks:

- Delta: -0.04

- Theta: 6.87

- Vega: -15.42

- Gamma: 0.00

Delta/Theta Ratio: 0.04 ÷ 6.87 = 0.006 (0.6%)

This is nearly perfect!

We’ve essentially eliminated delta while maximizing theta.

Why It Works:

- Bear call spread offsets bull put spread delta

- Total delta near zero

- Theta from both credit spreads combine

- Ideal ratio for non-directional income

Positioning Consideration:

In this example, the bear call spread is positioned further from the money (8-delta, 207 points away) compared to the bull put spread (18-delta, 173 points away).

If we positioned both sides equidistant with the call spread at 2185:

- Delta: Would increase slightly to around -0.47

- Theta: Would increase to 7.6

- Delta/Theta Ratio: 0.06 (6%)

Still excellent, but demonstrates the tradeoff between balanced positioning and optimal delta theta ratio.

Iron Butterflies

Iron butterflies produce the highest theta but require careful delta management.

Example: March 16, 2022

- RUT @ $2013

- Buy one April 14 RUT 1920 put

- Sell one April 14 RUT 2010 put (ATM)

- Sell one April 14 RUT 2010 call (ATM)

- Buy one April 14 RUT 2100 call

Greeks:

- Delta: -3.52

- Theta: 28.29

- Vega: -59.65

- Gamma: -0.04

Delta/Theta Ratio: 3.52 ÷ 28.29 = 0.12 (12%)

Even with one contract, this butterfly has massive theta ($28.29 per day).

The 0.12 ratio is still very good, but note:

Important Considerations:

- Much larger position size (max risk $1,860 vs condor’s $790)

- Negative delta (-3.52) creates bearish tilt

- Higher gamma means delta will change quickly

- Requires more active management

The Negative Delta:

Even though this butterfly is symmetrically centered, it starts with negative delta due to put-call skew, which is a phenomenon where puts trade at higher implied volatility than equidistant calls.

Some traders prefer this negative delta as a hedge against market downturns.

Others want more neutral positioning, leading to…

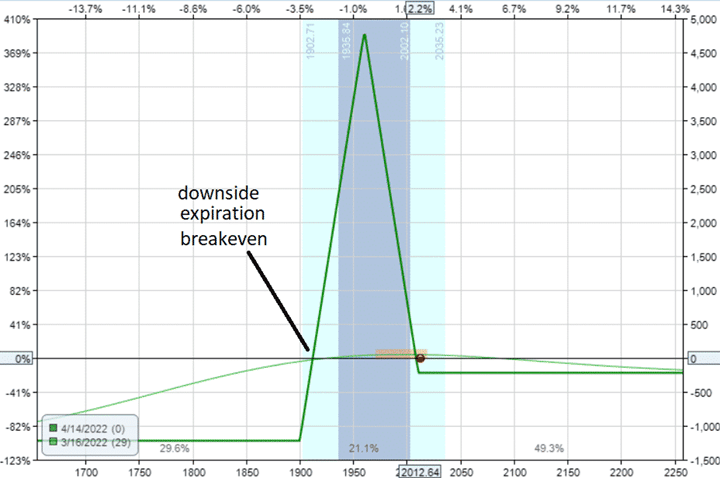

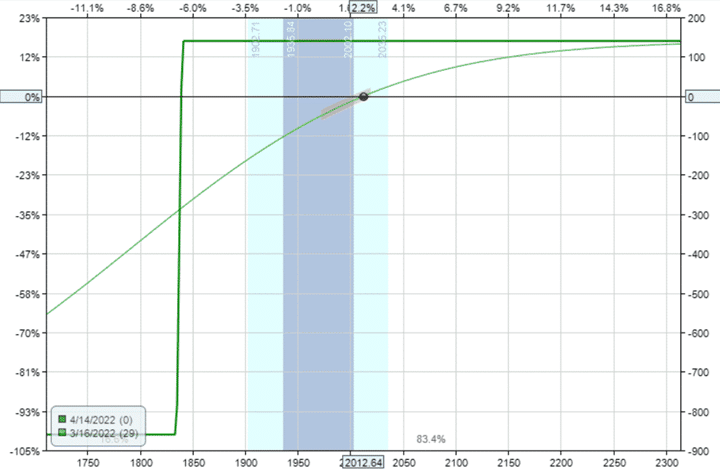

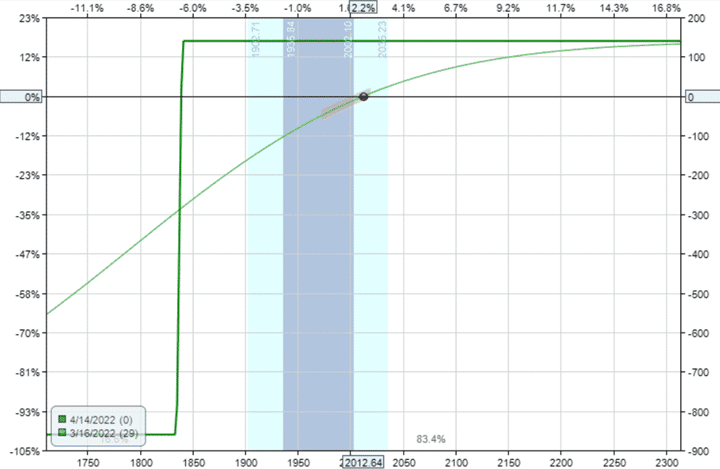

Broken Wing Butterflies

Broken wing butterflies adjust the wing widths to neutralize delta while maintaining high theta.

Example 1: Adjusted for Delta Neutrality

- RUT @ $2013

- Buy one April 14 RUT 1950 put

- Sell one April 14 RUT 2010 put (ATM)

- Sell one April 14 RUT 2010 call (ATM)

- Buy one April 14 RUT 2065 call

Greeks:

- Delta: -0.44

- Theta: 11.16

- Vega: -25.34

- Gamma: 0.01

Delta/Theta Ratio: 0.44 ÷ 11.16 = 0.04 (4%)

By narrowing the put wing and widening the call wing, we’ve:

- Reduced delta to nearly zero

- Maintained excellent theta

- Achieved an outstanding 0.04 ratio

- Created a more neutral position

Example 2: Rhino-Style Configuration

Some traders prefer having the downside breakeven further away.

This is used in strategies like the Rhino.

- Buy one April 14 RUT 1900 put

- Sell two April 14 RUT 1960 puts

- Buy one April 14 RUT 2010 put (at current price)

Greeks:

- Delta: -0.30

- Theta: 9.4

- Vega: -17.69

- Gamma: -0.06

Delta/Theta Ratio: 0.30 ÷ 9.4 = 0.03 (3%)

This all-puts broken wing produces:

- Near-zero delta

- Strong theta

- Exceptional 0.03 ratio

- Downside breakeven well below current price

Strike Selection and Delta Theta Ratio

Your strike selection has a massive impact on your delta theta ratio.

Here’s how different choices affect your Greeks:

The Delta Spectrum:

Far Out-of-the-Money (5-10 Delta):

- Very low delta

- Very low theta

- Ratio: Often 0.3-0.5 (good)

- Problem: Not enough premium to justify the trade

Sweet Spot (15-20 Delta):

- Moderate delta

- Good theta

- Ratio: Typically 0.4-0.5 (excellent)

- Balance: Good premium, reasonable risk

Closer to the Money (30+ Delta):

- High delta

- Higher theta, but not proportionally

- Ratio: Often 0.8-1.2 (poor for non-directional)

- Use: Only for directional plays

Practical Guidelines:

For Credit Spreads:

- Target short strikes at 15-20 delta

- Keeps delta theta ratio below 0.5

- Balances premium collection with risk

For Iron Condors:

- Put side: 15-20 delta short strike

- Call side: Can go farther (8-15 delta) to balance overall delta

- Total delta near zero, excellent ratio

For Butterflies:

- Sell at-the-money for maximum theta

- Adjust wings to achieve desired delta

- Monitor ratio, target 0.05-0.15

Time to Expiration Impact on Delta Theta Ratio

As expiration approaches, the delta theta ratio becomes more volatile due to accelerating theta and increasing gamma.

Comparison: 29 Days vs 14 Days

Example: Broken Wing Butterfly at 29 DTE

- Buy one April 14 RUT 1900 put

- Sell two April 14 RUT 1960 puts

- Buy one April 14 RUT 2010 put

Greeks:

- Delta: -0.30

- Theta: 9.4

- Gamma: -0.06

- Delta/Theta Ratio: 0.03

Same Structure at 14 DTE

- Buy one March 30 RUT 1910 put

- Sell two March 30 RUT 1965 puts

- Buy one March 30 RUT 2010 put

Greeks:

- Delta: -0.80

- Theta: 21.18

- Gamma: -0.08

- Delta/Theta Ratio: 0.04

Key Observations:

Theta Doubles:

- From 9.4 to 21.18

- Theta acceleration in final weeks

- This is why traders love shorter-term positions

Theta Exceeds Vega:

- At 14 DTE: Theta (21.18) > Vega (17.50)

- At 29 DTE: Theta (9.4) < Vega (17.69)

- Shorter trades have a beta Theta to Vega Ratio

Gamma Increases:

- Higher gamma means delta changes faster

- Delta theta ratio becomes more volatile

- Requires more frequent monitoring and adjustments

Management Implication:

As you get closer to expiration, even though your delta theta ratio might look good (0.04 in this example), the higher gamma means that ratio will fluctuate more rapidly with every market move.

This is why many traders:

- Close positions at 21 DTE and roll to 45 DTE

- Monitor more frequently in the final 2 weeks

- Have tighter adjustment triggers

How to Calculate Delta Theta Ratio

Calculating the delta theta ratio is straightforward, but interpreting it requires understanding your trading platform and position sizing.

Basic Calculation:

Delta Theta Ratio = Delta ÷ Theta

Always use the absolute value of delta (ignore negative sign) because you’re measuring magnitude of directional risk, not direction.

Examples:

Example 1: Single Iron Condor

- Delta: -12.5

- Theta: 45.3

- Ratio: 12.5 ÷ 45.3 = 0.28 (28%)

Example 2: Bull Put Spread

- Delta: 8.2

- Theta: 15.6

- Ratio: 8.2 ÷ 15.6 = 0.53 (53%)

Example 3: Butterfly

- Delta: -0.44

- Theta: 11.16

- Ratio: 0.44 ÷ 11.16 = 0.04 (4%)

Scaling by Position Size:

Important: If you trade multiple contracts, both delta and theta scale proportionally, so the ratio stays the same.

One Contract:

- Delta: 5

- Theta: 10

- Ratio: 0.5

Two Contracts:

- Delta: 10

- Theta: 20

- Ratio: 0.5 (unchanged)

Ten Contracts:

- Delta: 50

- Theta: 100

- Ratio: 0.5 (still unchanged)

This is why you can analyze delta theta ratio on a per-contract basis and scale up once you’ve verified the trade structure is sound.

Portfolio-Level Calculation:

For your entire portfolio:

- Sum total portfolio delta

- Sum total portfolio theta

- Calculate ratio

Example Portfolio:

- 5 iron condors: Delta -15, Theta +120

- 3 bull put spreads: Delta +24, Theta +45

- 2 butterflies: Delta -2, Theta +18

- Total: Delta +7, Theta +183

- Portfolio Ratio: 7 ÷ 183 = 0.04

This gives you a holistic view of your risk-reward profile.

When to Adjust Based on Delta Theta Ratio

The delta theta ratio provides clear signals for when your position needs attention.

Adjustment Triggers:

Initial Position (Setup):

- Target: 0.5 or lower

- Action: Enter trade only if ratio is favorable

- Don’t force trades in unfavorable volatility

Early in Trade (0-50% profit):

- Acceptable: Up to 0.3 (30%)

- Action: Monitor but no adjustment needed

- Let theta do its work

Warning Zone (Getting defensive):

- Warning: 0.3-0.5 (30-50%)

- Action: Prepare for potential adjustment

- Have adjustment plan ready

Adjustment Required:

- Critical: 0.5+ (50%+)

- Action: Adjust position to reduce delta

- Methods: Add opposing spread, roll tested side, reduce size

From My Bootcamp Day 1:

“For a typical iron condor that began with a delta theta ratio near 0%, you want to adjust when the delta theta ratio gets to around 30%.”

Why 30%?

At 30%, your directional risk has grown significantly relative to your remaining theta. If you don’t adjust:

- Further adverse moves accelerate losses

- Theta can’t keep pace with delta losses

- Position becomes increasingly directional

- Risk-reward deteriorates rapidly

Adjustment Methods:

Method 1: Add Opposing Spread If bullish delta has grown too large, add a bear call spread to offset.

Method 2: Roll Tested Side If price has moved against you, roll the threatened side further out.

Method 3: Add New Iron Condor Layer in a new position at 45 DTE while managing the older position.

Method 4: Close and Reset Sometimes the cleanest solution is to close at a small loss and redeploy capital in a better setup.

Monitoring Frequency:

0-0.2 Ratio: Check daily

0.2-0.3 Ratio: Check 2-3x daily

0.3-0.5 Ratio: Check multiple times per day

0.5+ Ratio: Requires immediate attention

As expiration approaches and gamma increases, you need to monitor the trade more frequently because the delta theta ratio gets out of line at an increasing rate.

Learn Systematic Adjustment Rules

Knowing when and how to adjust is the difference between consistent profits and frustrating losses:

Options Income Mastery – Learn proven adjustment triggers and techniques for credit spreads, iron condors, and other income strategies ($397)

The Accelerator Program – Advanced position management including delta hedging, gamma scalping, and portfolio-level Greek management ($997)

Index Options vs Individual Stocks

The delta theta ratio is much easier to manage in index options compared to individual stocks.

Why Indices Are Superior:

1. More Achievable Ratios

Index options like RUT (Russell 2000) and SPX (S&P 500) make it easier to achieve and maintain ideal delta theta ratios around 0.5 because:

- Lower volatility of diversified index vs single stocks

- More predictable price movement

- Less gap risk

- Smoother theta decay

2. Avoid Catalyst Events

Individual stocks can experience:

- Earnings surprises (20-40% moves)

- FDA announcements (biotech)

- Product launches

- Management changes

- Analyst upgrades/downgrades

These catalyst events can create massive overnight gaps that destroy carefully managed delta theta ratios.

3. Better Liquidity

Major indices offer:

- Tighter bid-ask spreads

- More strikes available

- Better fills on adjustments

- Lower transaction costs

4. Tax Benefits

SPX and RUT enjoy Section 1256 treatment:

- 60% long-term, 40% short-term capital gains

- Regardless of holding period

- Significant tax savings for active traders

When Individual Stocks Make Sense:

Despite the challenges, individual stock options work when:

- You have strong fundamental conviction

- Stock is very liquid (AAPL, MSFT, AMZN)

- Using the wheel strategy where you want to own the stock

- Accepting higher delta in exchange for higher premium

For pure non-directional income focused on ideal delta theta ratios, stick with indices.

Delta Theta Ratio Management Rules

Here are practical rules for using delta theta ratio effectively:

Rule 1: Start Right

Never enter a trade with a delta theta ratio above 0.5 unless you have a directional conviction.

If the initial setup doesn’t offer favorable risk-reward, wait for better conditions.

Rule 2: Position Size Based on Ratio

Lower ratios allow for larger position sizing:

- 0.0-0.2 ratio: Can use larger size

- 0.2-0.4 ratio: Moderate sizing

- 0.4-0.6 ratio: Smaller positions

- 0.6+ ratio: Avoid unless directional play

Rule 3: Adjust at 30%

When delta theta ratio reaches 0.3 (30%), have an adjustment plan ready and be prepared to execute.

Rule 4: Consider Portfolio Level

Don’t just look at individual positions.

Your total portfolio delta theta ratio is what matters for overall risk management.

Rule 5: Volatility Adjustments

High IV (VIX > 20):

- Target ratios of 0.3-0.4

- More aggressive position sizing

- Excellent risk-reward available

Normal IV (VIX 15-20):

- Target ratios of 0.4-0.5

- Standard position sizing

- Good conditions for premium selling

Low IV (VIX < 15):

- Accept ratios of 0.5-0.7

- Reduce position sizing

- Consider waiting for better setups

Rule 6: Time Decay Awareness

As you approach expiration:

- Gamma increases, making ratio more volatile

- Monitor more frequently

- Tighten adjustment triggers

- Consider closing early (21 DTE rule)

Rule 7: Don’t Over-Optimize

Perfect ratios (0.0-0.1) often mean:

- Positions too far from the money

- Not enough premium to justify trade

- High transaction costs relative to profit potential

Target 0.3-0.5 for practical, profitable trading.

Common Delta Theta Ratio Mistakes

Avoid these frequent errors when managing delta theta ratios:

Mistake 1: Ignoring Gamma

Focusing only on delta theta ratio while ignoring gamma is dangerous.

High gamma means your delta will change rapidly, making your ratio unstable.

Solution: Consider delta, theta, AND gamma together.

High gamma positions require more frequent monitoring.

Mistake 2: Chasing Perfect Ratios

Trying to achieve 0.0-0.1 ratios often means:

- Positioning strikes too far OTM

- Collecting minimal premium

- Transaction costs eating profits

Solution: Accept 0.3-0.5 as excellent and profitable.

Mistake 3: Not Adjusting to Volatility

Using the same ratio targets regardless of market volatility.

Solution: Adjust targets based on VIX and underlying-specific IV.

Be more lenient in low IV environments.

Mistake 4: Over-Adjusting

Constantly tweaking positions to maintain perfect ratios leads to:

- Death by a thousand commissions

- Increased slippage

- Reduced returns

Solution: Accept some fluctuation.

Only adjust when ratio exceeds 0.3 significantly.

Mistake 5: Forgetting About Vega

Focusing solely on delta and theta while ignoring vega exposure can lead to nasty surprises during volatility spikes.

Solution: Monitor your theta-vega ratio too (see related content on this topic).

Mistake 6: Same Approach for All Strategies

Different strategies require different ratio targets:

- Iron condors: Target 0.0-0.1

- Butterflies: Target 0.1-0.2

- Credit spreads: Target 0.4-0.5

Solution: Adjust expectations based on strategy type.

Mistake 7: Individual Trade Focus

Obsessing over individual trade ratios while ignoring portfolio-level exposure.

Solution: Manage both.

Individual trades should have good ratios, but portfolio balance matters more.

FAQs About Delta Theta Ratio

What is the delta theta ratio?

The delta theta ratio is a metric that compares the rate of change of an options position’s delta (directional risk) to its theta (time decay profit).

It’s calculated by dividing the absolute value of delta by theta.

For example, a position with delta of -10 and theta of +20 has a delta theta ratio of 0.5 (or 50%).

This ratio helps traders assess whether they’re getting adequate income (theta) relative to the directional risk (delta) they’re taking.

What is the ideal delta theta ratio?

The ideal delta theta ratio for non-directional income traders is 0.5 or lower (50% or less).

This means your theta should be at least 2X your delta.

Tom Sosnoff of TastyTrade states:

“In a perfect world, you would much prefer your deltas about half of your theta.”

In practice, ratios between 0.3-0.5 are excellent for premium selling strategies like iron condors and credit spreads.

Lower ratios (0.0-0.2) are achievable with perfectly balanced iron condors and butterflies.

How is the delta theta ratio calculated?

The delta theta ratio is calculated using this formula: Delta Theta Ratio = |Delta| ÷ Theta.

Always use the absolute value (positive number) of delta since you’re measuring magnitude, not direction.

For example: if your position has delta of -15 and theta of +30, the ratio is 15 ÷ 30 = 0.5.

If trading multiple contracts, both delta and theta scale proportionally, so the ratio remains constant regardless of position size.

When should I adjust my position based on delta theta ratio?

You should adjust your position when the delta theta ratio exceeds 0.3 (30%).

At this level, your directional risk has grown too large relative to your remaining theta profit potential.

Common adjustment triggers include: initial setup above 0.5 (don’t enter), ratio climbing to 0.3 during the trade (prepare to adjust), and ratio exceeding 0.5 (adjust immediately).

The closer you get to expiration, the more frequently you need to monitor because gamma increases and makes the ratio more volatile.

How does volatility affect delta theta ratio?

Higher volatility produces lower (better) delta theta ratios because option premiums increase, boosting theta relative to delta.

In the examples above, a bull put spread in high volatility (RVX 33) had a ratio of 0.43, while the same structure in low volatility had a ratio of 0.59.

In low IV environments, you should accept higher ratios (0.5-0.7) or wait for better conditions.

In high IV environments (VIX > 20), target excellent ratios of 0.3-0.4 and consider larger position sizing.

Why are index options better for delta theta ratios?

Index options like SPX and RUT make it easier to achieve and maintain ideal delta theta ratios because they avoid catalyst event risk that plagues individual stocks.

Indices offer more predictable price movement, lower gap risk, better liquidity, and tighter spreads.

Individual stocks can experience 20-40% overnight moves from earnings, FDA announcements, or other catalysts that destroy carefully managed ratios.

For pure non-directional trading focused on optimal delta theta ratios, major indices are superior to individual stocks.

What’s the difference between delta theta ratio for different strategies?

Different strategies produce vastly different delta theta ratios: Credit spreads typically achieve 0.4-0.5 when short strikes are at 15-20 delta.

Iron condors can achieve near-perfect ratios of 0.0-0.1 when properly balanced.

Iron butterflies produce higher theta but start around 0.12 due to at-the-money short strikes.

Broken wing butterflies can achieve excellent ratios of 0.03-0.05 by adjusting wing widths to neutralize delta.

The strategy you choose should match your ratio targets and risk tolerance.

How does time to expiration impact delta theta ratio?

As expiration approaches, theta accelerates while gamma increases, making delta theta ratios more volatile.

A broken wing butterfly at 29 DTE might have theta of 9.4 and gamma of -0.06, while the same structure at 14 DTE has theta of 21.18 but gamma of -0.08.

While theta more than doubles (beneficial), the higher gamma means delta changes faster with every market move, requiring more frequent monitoring and tighter adjustment triggers.

Many traders close positions at 21 DTE to avoid this increased volatility.

Conclusion: Mastering Risk-Reward Balance

The delta theta ratio is one of the most powerful tools available to options income traders for optimizing risk-reward balance.

Key Takeaways:

- Target 0.5 or Lower For non-directional premium selling, keep your delta theta ratio at 0.5 (50%) or below. This ensures you’re getting at least $2 of theta for every $1 of delta risk.

- Adjust to Market Conditions In high volatility, achieve excellent ratios of 0.3-0.4. In low volatility, accept 0.5-0.7 or wait for better setups.

- Strategy Matters

• Iron condors: 0.0-0.1 (nearly perfect)

• Butterflies: 0.1-0.2 (excellent)

• Credit spreads: 0.4-0.5 (good) - Adjust at 30% When your delta theta ratio climbs to 0.3 during a trade, prepare for adjustments. Above 0.5 requires immediate action.

- Prefer Indices RUT, SPX, and NDX offer superior delta theta ratio management compared to individual stocks due to lower catalyst risk and more predictable behavior.

- Watch Gamma Too High gamma makes delta theta ratios more volatile, requiring more frequent monitoring and tighter management, especially approaching expiration.

- Portfolio View While individual position ratios matter, your total portfolio delta theta ratio determines your overall risk exposure.

The Bottom Line:

Understanding and actively managing your delta theta ratio transforms you from a passive premium seller hoping for the best into a systematic trader optimizing risk-reward on every position.

The 0.5 rule—keeping delta at 50% or less of theta—provides a simple, actionable framework that works across strategies and market conditions.

Combined with proper strike selection, position sizing based on volatility, and disciplined adjustment triggers at the 30% level, the delta theta ratio becomes your compass for navigating the options landscape.

If you’ve enjoyed this deep dive into delta theta ratios, visit the topic of theta-vega ratios for another crucial dimension of Greeks management.

Related Articles

- Bull Put Spreads Guide

- Best Iron Condor Strategy

- Selling Put Options Strategy

- The Wheel Strategy

- Weekly Option Strategies

We hope you enjoyed this comprehensive guide to delta theta ratio.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

hi Gav, this delta theta ratio is valid for US mkts.. cud u give a ratio for Indian mkts(Nifty).. if we trade Broken Wing Butterfly.

I’m not hugely familiar with the Indian market, but the same principles should hold true.

I am quite confused by the Delta/Theta ratio.

Take one example, as of today 7/9/2022,

IWM’s price: 175.59

Put strike 160 , Exp 12/08/2022, Premium 1.66, Delta -0.17, Gamma 0.01, Theta -0.07, Vega .14

RTU Price: 1769.3645,

Put strike 1610 , Exp 12/08/2022, Premium 16.65, Delta -0.17, Gamma 0.00, Theta -0.65, Vega 1.35

The two underlying are the same thing, However, their deltas and vegas are ten times different.

I understand that Delta is a slope (or ratio, margin) with no unit of measure, while Theta’s unit of measure is dollar/day. They can’t be compared. Better to compare Delta dollars with Theta dollars to check risk/theta.

By the way, I want to thank you for all the information!

Yes, makes sense. Thanks.