August 5, 2024, was a bad day for selling option premium.

I don’t care how they were selling premiums or what strategies they were using.

They likely took a loss if they had trades on that day that sold premium.

When I say “purely selling premium,” I mean that the trade’s main purpose is to sell options premium without directional bias.

I’m not talking about directional trades with some premium selling component.

Some took a substantial loss.

And others took smaller losses.

There might be an exception where a very small minority did okay because they had some hedges or some peculiar thing with their strategy.

Contents

Premium Selling

Let’s first explain who these option premium sellers are.

Their primary goal is to sell options (either call options or put options or both) and then buy them back at a lower price to close the trade.

The difference between the sale price and the buy-back price is the profit that they keep.

The idea is that options are priced in a time factor so that their sale price is higher than the intrinsic value of that option.

This extra value is known as the extrinsic value of the option.

The more time the option has till expiration, the greater the extrinsic value is.

The extrinsic value usually decreases as time passes (unless volatility changes affect it).

Hence, in theory, the option’s value should decrease with time (if all other things go as normal).

This is what the option premium seller is betting on – that he/she can sell an option at a high price, wait a while, and buy it back at a lower price when the option value decreases.

Because the price of the option is also known as the premium of the option, we sometimes refer to these option sellers as premium sellers.

These premium sellers are not really in the game of trying to predict the directional move of an asset.

They are just interested in the option decaying in value with time.

The Strangle

The strangle is an example of such a non-directional premium selling strategy.

It involves selling a call option and a put option that opposes each other to avoid directional bias.

For example:

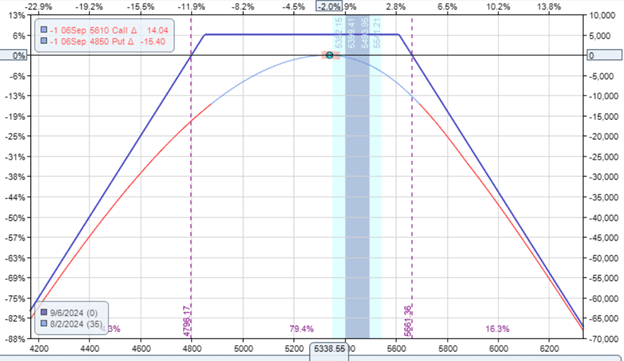

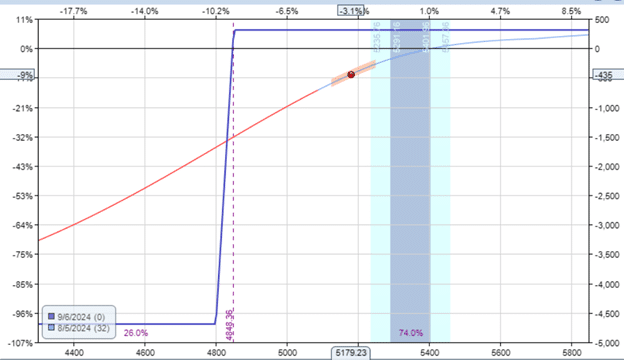

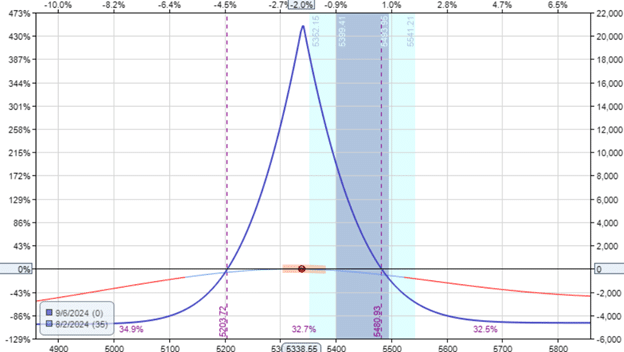

Date: August 2, 2024

Price: SPX @ 5338

Sell one September 6 SPX 4850 put @ $27.45

Sell one September 6 SPX 5610 put @ $23.05

Credit: $5,050

The trade initially collects a credit of $5050.

If all goes well, the trader hopes to buy back to close the trade at a price of less than $5050.

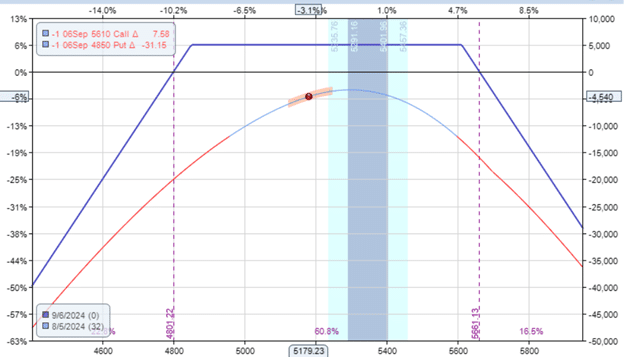

The next day, SPX dropped to 5186.

From market close Friday to market close Monday, there was a huge 160-point drop.

Source: tradingview.com

Not only this, but the volatility increased, with VIX going from 23.38 to 38.56 (close to close).

During Intraday on August 5, the VIX even spiked to over 60.

This is partly due to the Bank of Japan deciding to tighten its monetary policy to stabilize a weak Yen, which caused the Japanese market to fall 12 percent.

As a result, the strangle lost $4540, a 5.7% loss on margin:

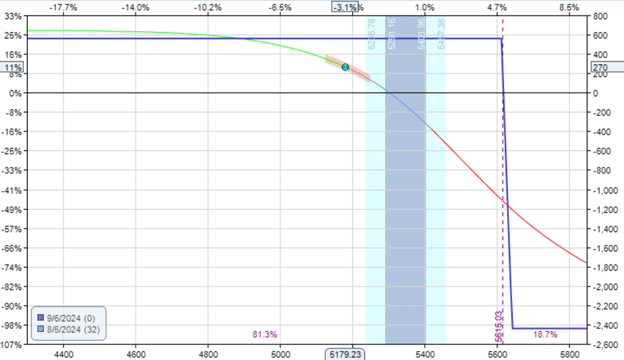

Based on the modeling of the first risk graph, we see that if there was not a volatility change, a drop of 160 points would have resulted in a loss of about -$1440.

So, a large part of the loss ($3100) is due to the rise in volatility.

You can also see in the second risk graph that the T+0 line had dropped – showing that the trade lost money.

This is when volatility rises in a trade with negative vega.

The strangle is a negative vega trade.

It is also known as a short volatility trade because it wants volatility to decrease.

This example illustrates how non-directional premium sellers can lose money.

They lose money when price makes a big move and when there is a rise in implied volatility.

In terms of both factors, they experienced a big loss on August 5, 2024.

Iron Condor

A trader who is not comfortable taking a $4500 loss in one day should not be trading non-defined risk strangle trades on the SPX index – not even one contract.

A tamer trade would be the defined risk iron condor.

In this example, we sell the same 15-delta out-of-the-money short call and short put as before. But this time, we buy protective long-term put and protective long-term calls to limit the risk.

For example,

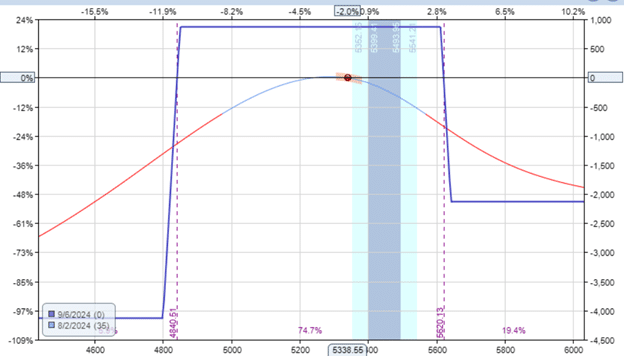

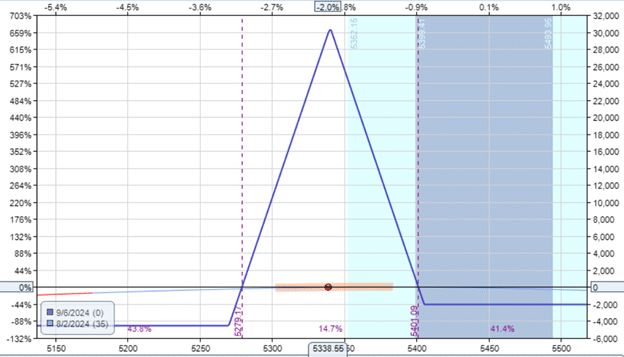

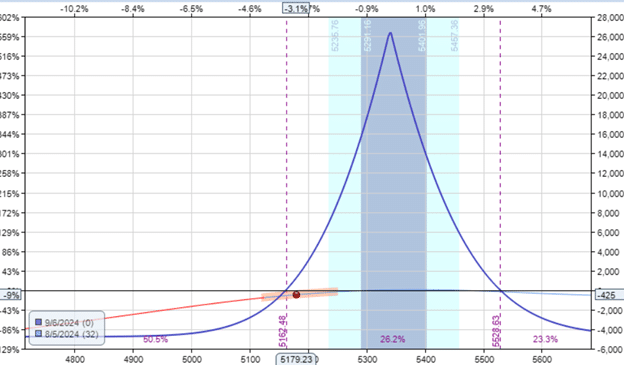

Date: August 2, 2024

Price: SPX @ 5338

Buy one September 6 SPX 4800 put @ $24.35

Sell one September 6 SPX 4850 put @ $27.45

Sell one September 6 SPX 5610 call @ $23.05

Buy one September 6 SPX 5640 call @ $17.45

Credit: $870

This time, we get a smaller credit.

Receiving a smaller credit indicates that this trade has less risk than the previous one.

Looking at the risk graph, we see that it has a max risk of $4130:

It is an asymmetric iron condor with a smaller call spread than the put spread.

This is so that we can get the overall delta closer to zero.

The delta on this trade is -0.78.

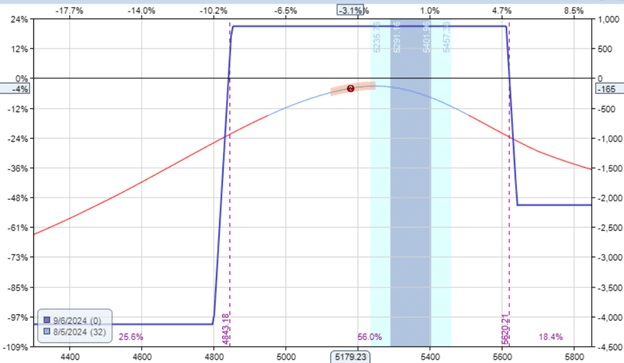

One day later, the trade is down $165, or down 4% on the capital at risk:

Bull Put Spread

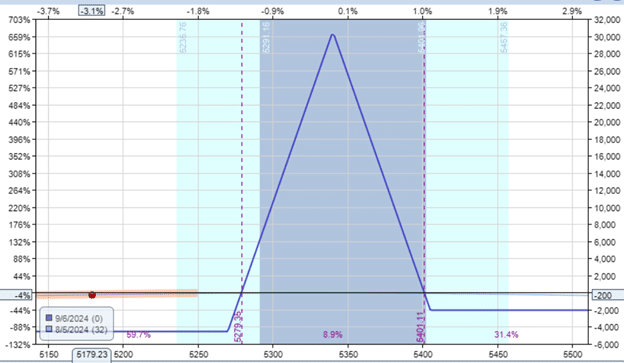

The iron condor consists of a bull put spread and a bear call spread.

Looking at the bull put spread, we see from the modeling that it lost -$435, or -9%, on its capital at risk:

Any bull put spreads took a beating on that day, August 5, 2024, because the direction and volatility had gone significantly against the trade.

If bull put spreads take such losses, cash-secured short put trades will take equal or greater losses.

Cash-secured short puts are used in the Wheel trade and the 1-1-2 trades.

Bear Call Spread

The loss in the bull put spread of the iron condor is partially offset by the gains in the bear call spread.

The bear call spread did make money because the price went in the same direction that the trade wanted it to go:

It profited $270 to help compensate for the loss of the bull put spread.

Butterfly

How about a non-directional butterfly with the same expiration as the previous examples – 35 days till expiration?

Date: August 2, 2024

Price: SPX @ 5338

Buy five September 6 SPX 5270 put @ $93.45

Sell ten September 6 SPX 5340 put @ $116.85

Buy five September 6 SPX 5405 put @ $144.35

Debit: -$2050

We did five contracts to make the max risk of $4550 somewhat close to that of the iron condor example:

It, too, took a similar loss of -$200, or -4.4%:

The Calendar

Unlike the previous example, the calendar has positive vega.

Let’s see how it does.

Date: August 2, 2024

Price: SPX @ 5338

Sell five September 6 SPX 5340 put @ $116.85

Buy five September 13 SPX 5340 put @ $126.15

Debit: -$4650

BEFORE:

AFTER:

Ouch. It lost 9%, or -$425, despite VIX going up.

This highlights the fact that calendars sometimes do not behave as their overall vega leads us to believe.

This is because the volatility of the short and long options can change at different rates due to their different expiration dates.

This effect is less prominent in trade structures where every option has the same expiration date.

Conclusion

The story’s moral is that if you sell options premium – and there is nothing wrong with that – you need to keep your position size small.

“Small” means different things to different people depending on their account size, disposable cash, and risk tolerance.

But you can not know what is small for you unless you know how big of a loss your strategy can encounter in one day.

You may have a good plan. Your strategy may work well month after month until the market decides to hit back one day.

As the boxer Mike Tyson says, “Everyone has a plan until they get punched in the mouth.”

Yes, you need a plan and follow it.

You may need to adapt your plan over time.

You also need to know how hard the market can hit so that you can size your positions small enough.

Some YouTubers pride themselves on full transparency and post their options trading results.

They might post some amazing gains month after month and then post this loss.

I don’t want to point out any in particular because some “took a really nice big giant drawdown” – quoting from YouTube videos.

Another had said, “manic Monday unbelievable slaughterhouse that it was in the markets … it was ugly.”

More than one of them had mentioned that they should have shrunk their position size.

We hope you enjoyed this article on selling option premium.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

In your examples some puts have to be changed for calls

Thanks. Fixed.