I was flabbergasted when I heard that some traders cannot trade calendars on indices.

This could be due to certain brokerages, countries, or account types.

Or it could be because certain brokerages calculate calendars differently, requiring extra margin or additional option trading privileges.

While some market-neutral butterfly strategies (such as the M3.4U and V32) do not require the use of calendars, many butterfly strategies (such as the Rhino and A14) do commonly use calendars as upside adjustments.

The Rhino is traded on the RUT and SPX indices.

The alternative to using calendars on these indices is to buy calendars on the corresponding ETFs (such as the IWM and SPY, respectively).

However, this incurs greater commissions because you have to buy ten times as much since the ETFs are 1/10th the size of the index.

In this article, we will explore using the butterflies as upside adjustments in the Rhino instead of calendars.

Contents

-

-

-

-

-

- Standard Calendar Adjustment

- Can You Use Call Broken-Wing Butterflies Instead?

- Can We Use Only One Call, Broken-Wing-Butterfly?

- What If You Are Trading A One-Contract Rhino?

- Is The Concept The Same With An SPX Rhino?

- What If I Had Not Scaled Into The Rhino?

- How Do You Handle Whipsaws?

- What Are The Benefits Of Using Upside Butterfly Adjustments?

- What To Do When The Price Of The Underlying Keeps Going Up?

- Is The Expiration Of The Upside Butterfly The Same As The Expiration Of The Base Butterfly?

- Why Do You Use Call Options For The Upside Butterfly?

- Closing Thoughts

-

-

-

-

Standard Calendar Adjustment

First, we will review the standard calendar adjustment.

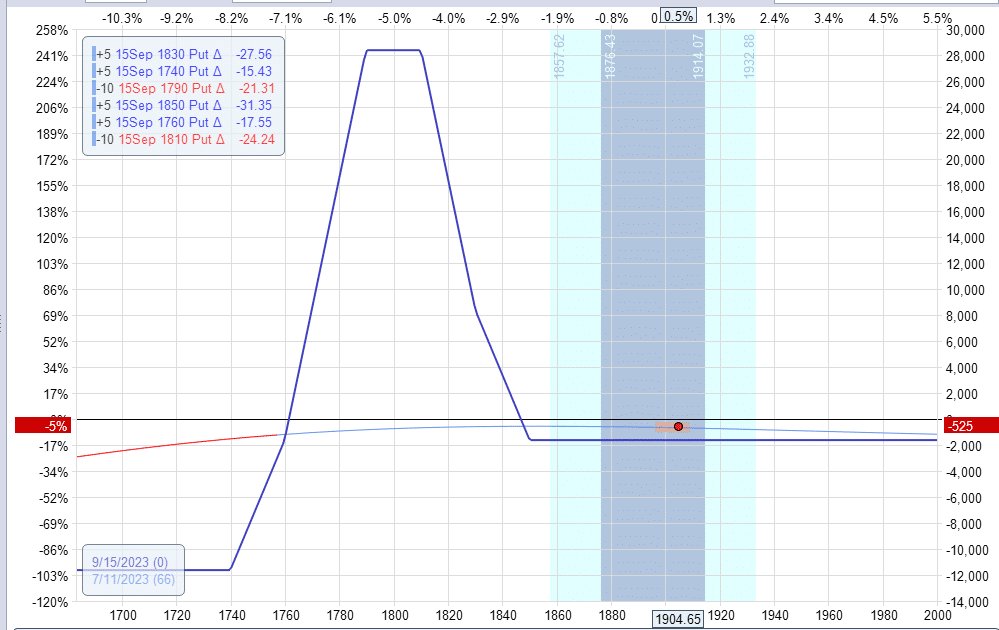

Consider this RUT Rhino that has already been scaled to ten butterflies forming this base. Graph via OptionNet Explorer.

Delta: -4.2

Theta: 18

Vega: -92

Price has continued to move up, requiring a standard upside adjustment of adding calendars above the current price.

Adding three calendars at 1940 would give us the following:

Delta: 0.39

Theta: 27

Vega: 7.83

We decreased our delta to make it flat.

The maximum risk in this trade increased to $14,000.

The calendars give us additional theta and neutralize the magnitude of the vega.

However, it can change the trade from a negative vega trade to a slightly positive one.

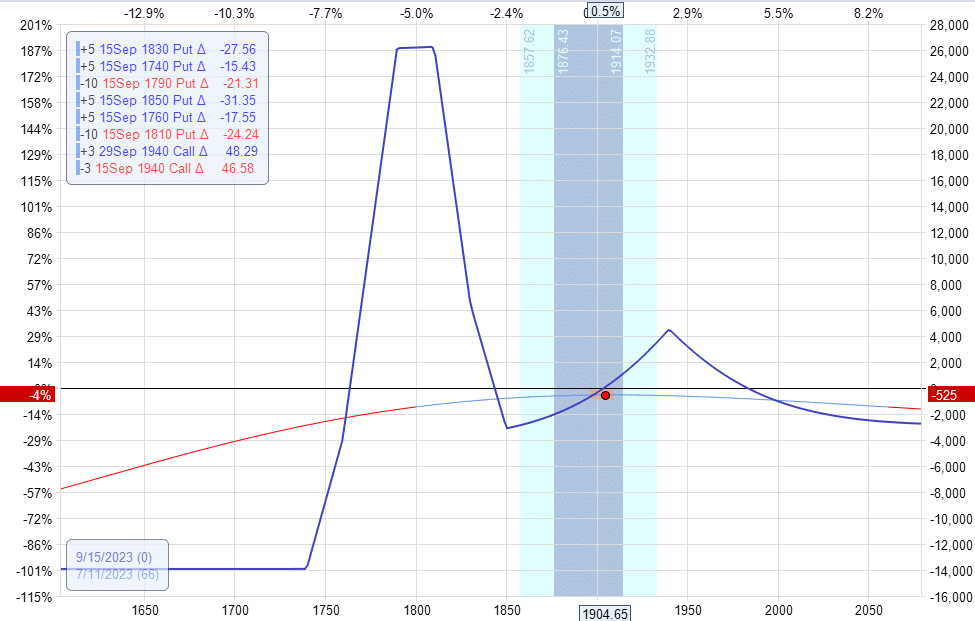

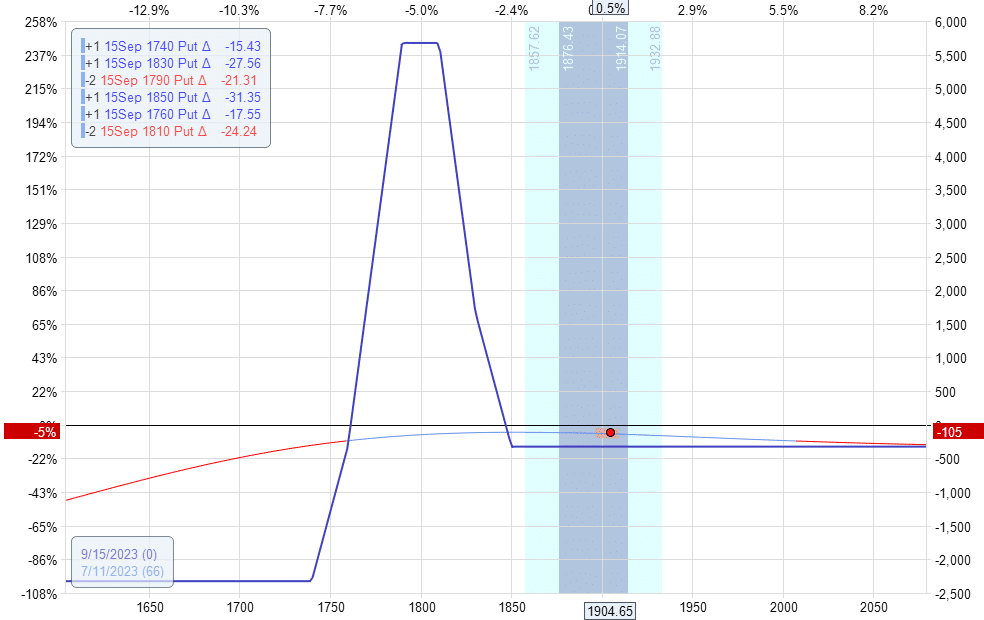

Can You Use Call Broken-Wing Butterflies Instead?

Yes, you can.

Instead of the calendars, let’s add two call broken-wing butterflies with 50 points lower wings and 40 points upper wings. We used the same lower wing width as the original butterfly.

Buy two September 15 RUT 1890 call

Sell four September 15 RUT 1940 call

Buy two September 15 RUT 1980 call

This gets the overall trade delta to nearly zero:

Delta: 0.46

Theta: 23

Vega: -150

The max risk in this trade increased to $14,000, just as in the calendars.

The theta is a little bit less.

The negative vega has significantly increased to be more negative. Increased vega means greater volatility exposure.

Negative vega means the trade prefers volatility to drop.

This may be fine in a high-volatility environment, where volatility may drop.

But in a low volatility environment with a possibility of a volatility spike, the larger amount of negative vega may become a liability.

One can hedge this by having some negative delta because a drop in the price of the underlying usually accompanies an increase in volatility.

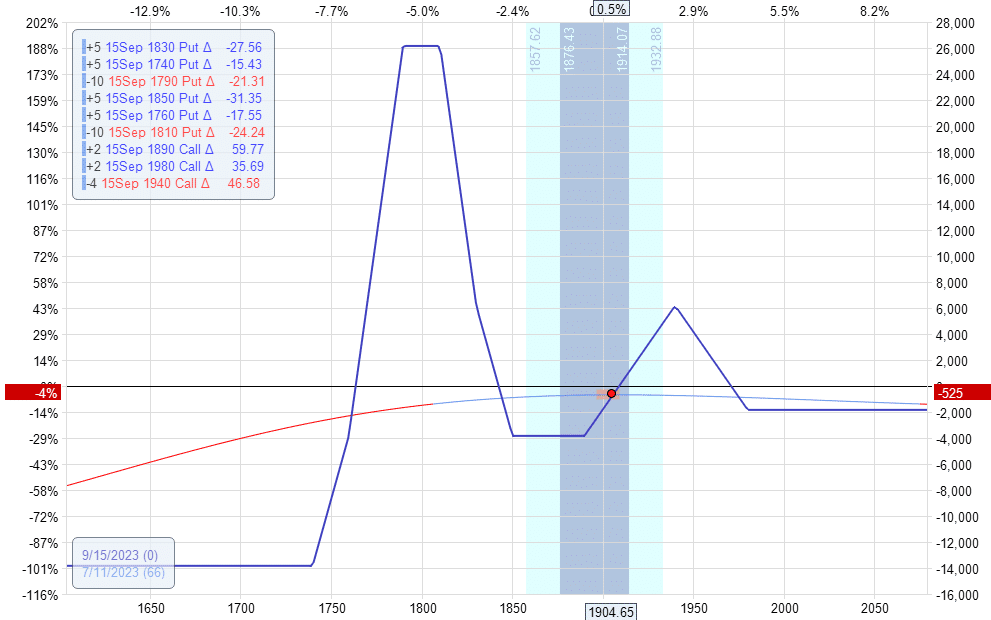

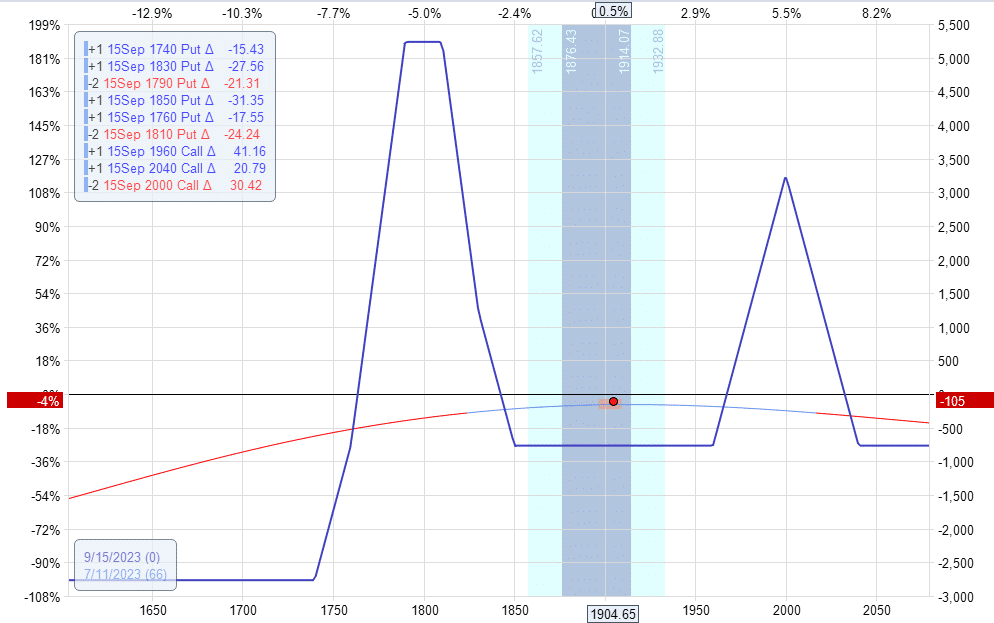

Can We Use Only One Call, Broken-Wing-Butterfly?

You can get the delta adjustment you want with only one butterfly.

We just need to make the butterfly more bullish with a 30-point upper wing and a 50-point lower wing.

Buy one September 15 RUT 1890 call

Sell two September 15 RUT 1940 call

Buy one September 15 RUT 1970 call

Delta: 0.71

Theta: 18.5

Vega: -114

The call butterfly is smaller in relation to the base.

So you get less theta and less negative vega exposure (i.e., less volatility risk).

Because we are buying fewer butterflies, there is less downside risk.

And there is less upside risk as well.

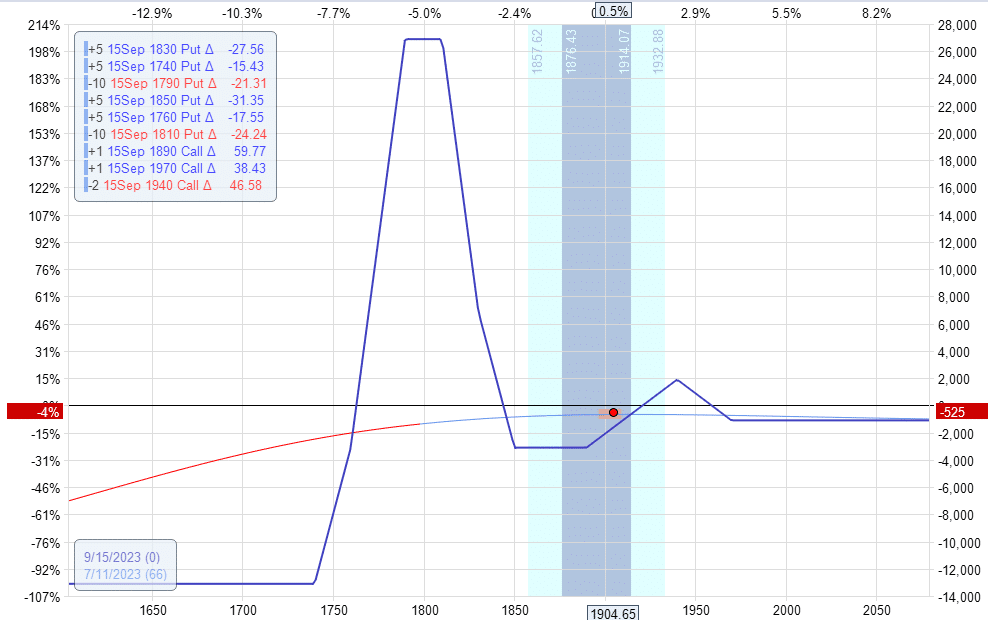

Take a look at the two expiration graphs.

The downside max risk here is -$13,100. The upside risk is -$1,100.

Unlike a calendar adjustment, this expiration graph does not change as volatilities change because this trade has no time spreads.

What If You Are Trading A One-Contract Rhino?

With a one-lot instead of a ten-lot, you will have less ability to fine-tune the adjustments.

However, it can still work if you make the upside fly smaller and further away.

If the one upside call broken-wing-butterfly is still too bullish, you might need to make it a symmetrical butterfly.

For example:

Before adjustment:

After adjustment of adding one 40-point symmetrical butterfly at 2000:

Is The Concept The Same With An SPX Rhino?

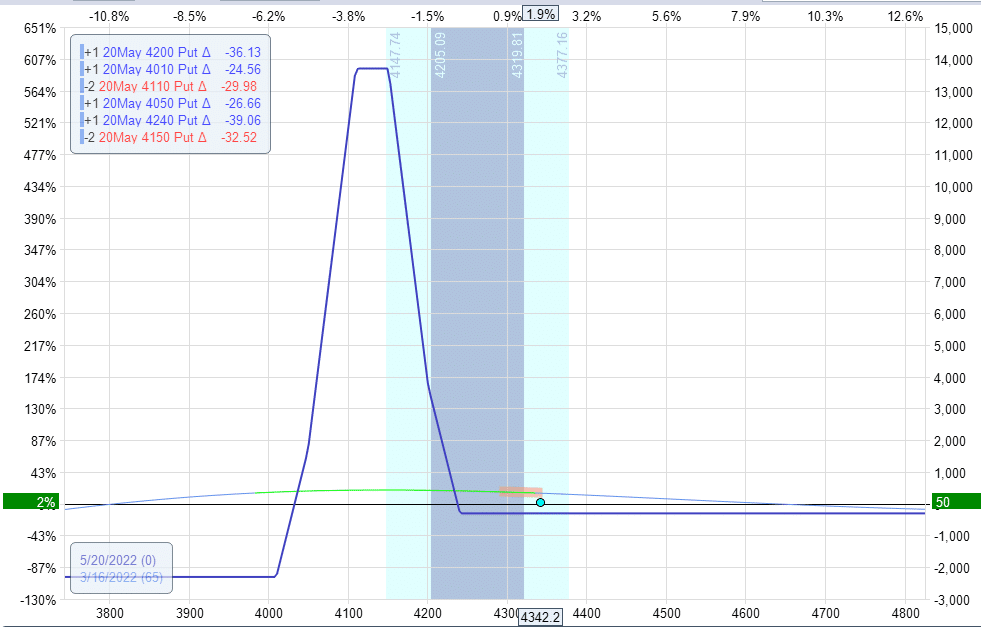

Yes, let’s consider the following SPX Rhino.

Delta: -0.95

Theta: 7.14

Vega: -32.64

If we use a calendar adjustment:

Sell one May 20 SPX 4600 call

Buy one May 31 SPX 4600 call

Debit: -$770

We would get the following:

Delta: 0.65

Theta: 12.01

Vega: 36.14

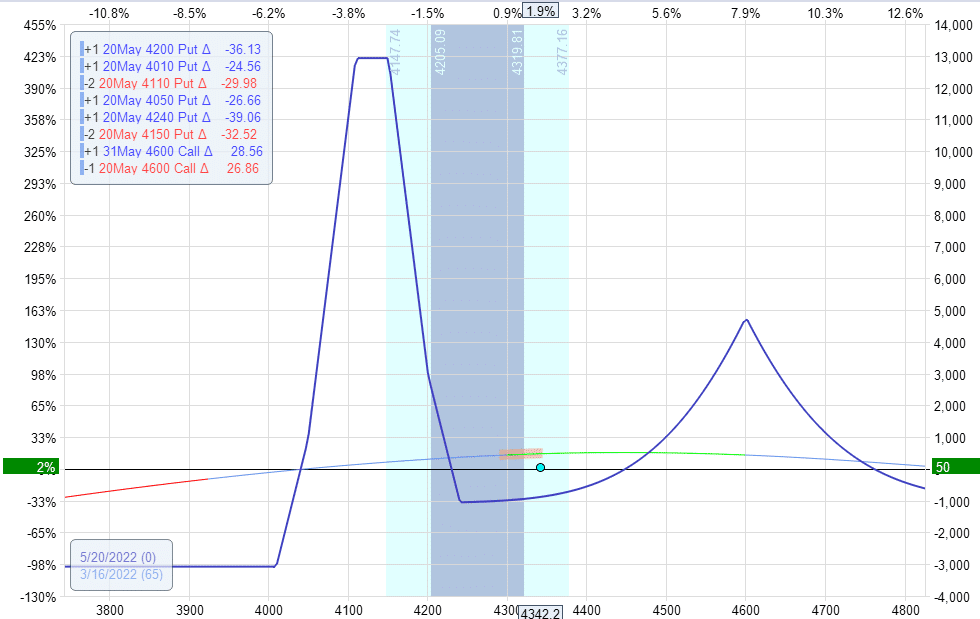

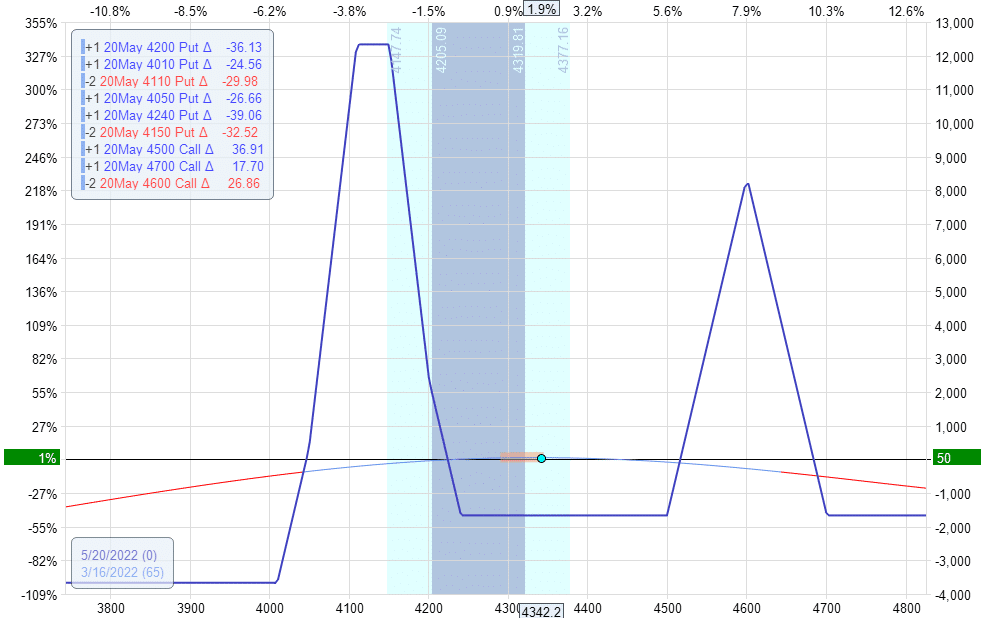

If we add a fly instead:

Buy one May 20 SPX 4500 call

Sell two May 20 SPX 4600 call

Buy one May 20 SPX 4700 call

Debit: -$1360

We get the following:

Delta: 0.04

Theta: 11.22

Vega: -74.70

The cost of the fly is a little bit more than the calendar.

And it has a little bit less theta.

For the fly adjustment, we had doubled our negative vega.

For the calendar adjustment, we flipped the sign of vega to positive vega.

Overall, the trade with the calendar adjustment has less volatility exposure.

What If I Had Not Scaled Into The Rhino?

In that case, your butterfly base is even smaller.

So, your upside butterfly would need to be smaller by having smaller wing widths.

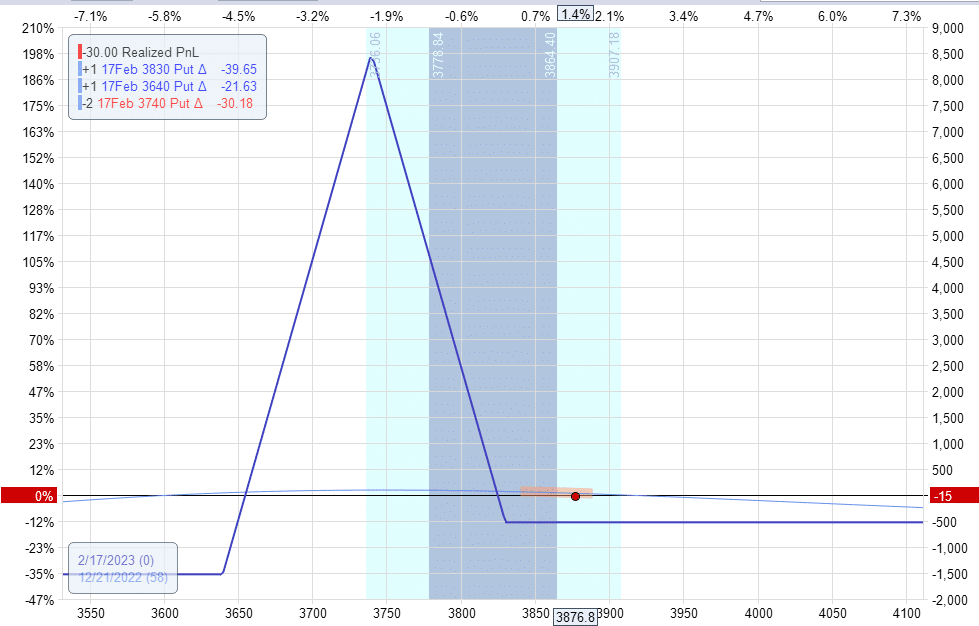

Here is an SPX Rhino where the trader decided not to scale in, or perhaps it was scaled in and subsequently taken off. In either case, we only have one contract butterfly.

Delta: -0.92

Theta: 6.76

Vega: -29.66

Adding one butterfly with a lower wing 50 points wide (half the size of the original fly) and an upper wing 40 points.

Buy one February 17 SPX 3950 call

Sell two February 17 SPX 4000 call

Buy one February 17 SPX 4040 call

We end up with a butterfly with a baby fly:

Delta: 0.42

Theta: 6.9

Vega: -37.6

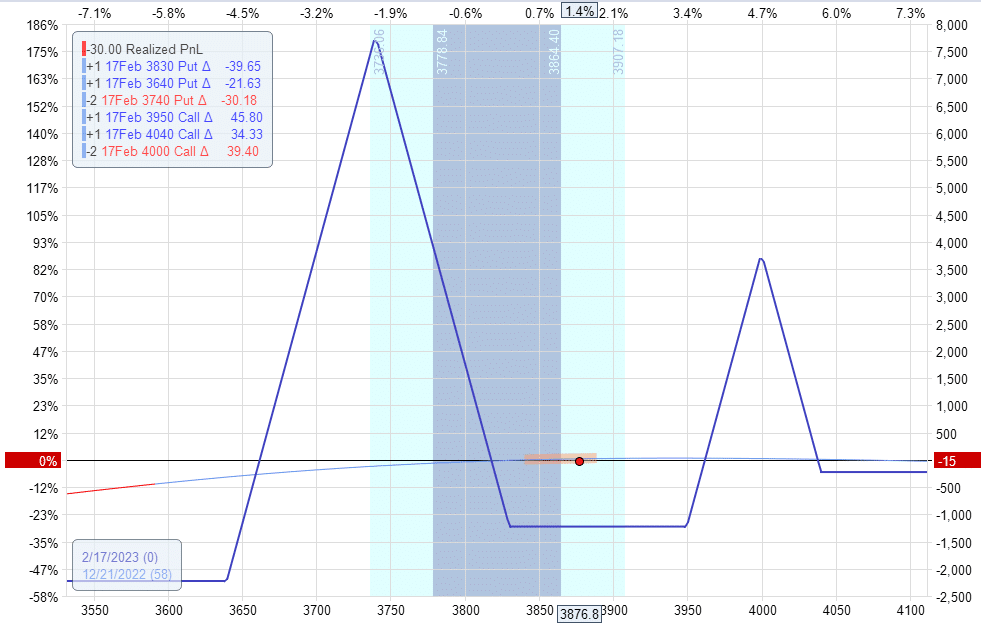

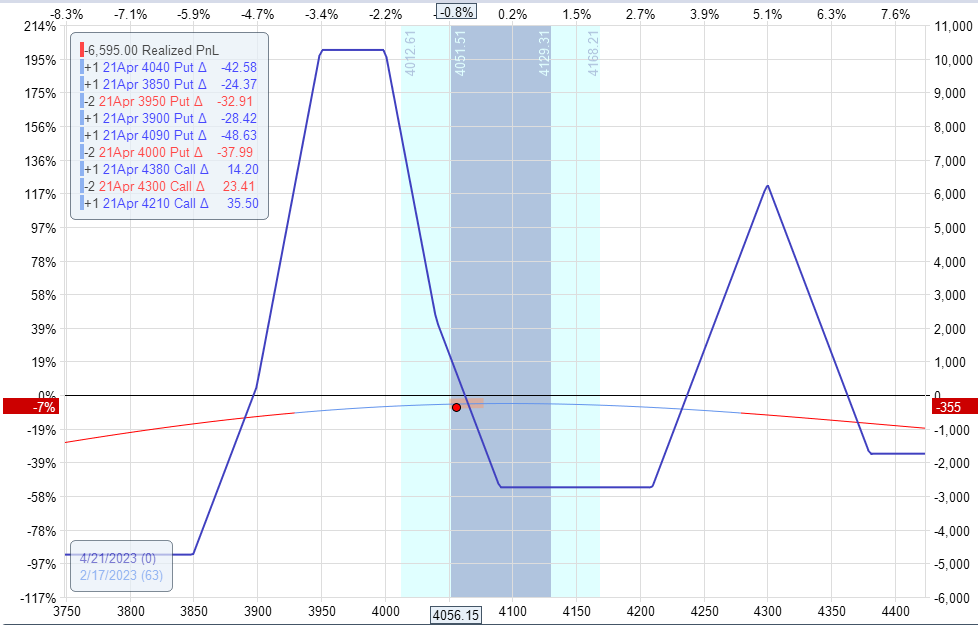

How Do You Handle Whipsaws?

Below, you see a scaled-in SPX Rhino with a call broken-wing butterfly.

The price reversed and came back down into the original butterfly base.

Delta: 2.1

Theta: 10.4

Vega: -92.7

By rolling up the lower leg of the call fly from 4200 to 4210:

Sell one April 21, 2023, SPX 4200 call

Buy one April 21, 2023, SPX 4210 call

We adjusted and reduced our delta and increased our theta:

Delta: 0.71

Theta: 12.85

Vega: -101.30

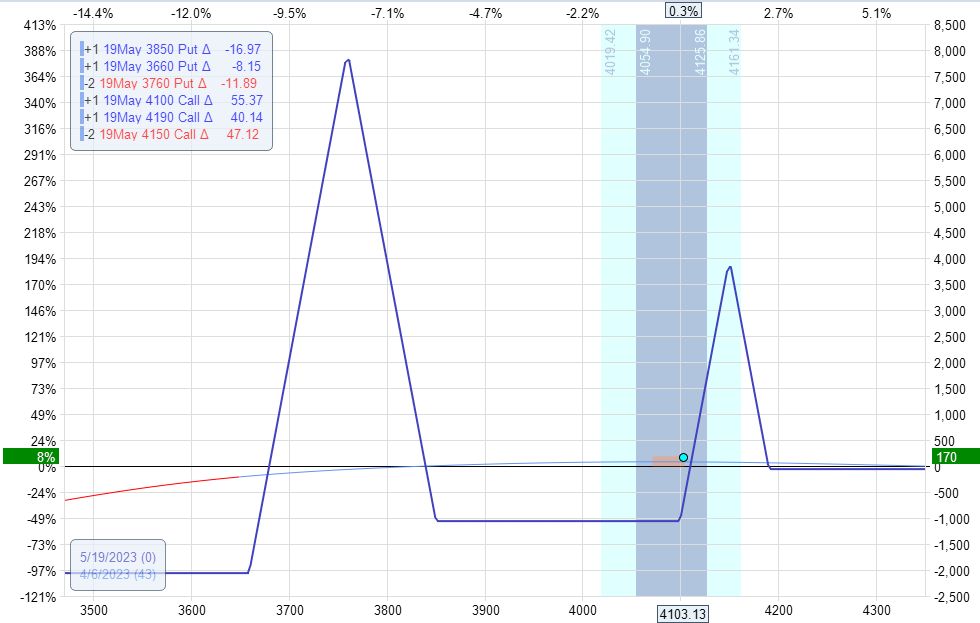

What Are The Benefits Of Using Upside Butterfly Adjustments?

First is the flexibility of adjusting deltas by rolling the legs of the upside butterfly.

Second, the upside butterfly profits from both its positive delta and its negative vega in the scenario where the price moves up toward the butterfly, as in the case here:

As the price goes up, the implied volatility tends to drop,

This volatility drop is a benefit to a negative vega butterfly.

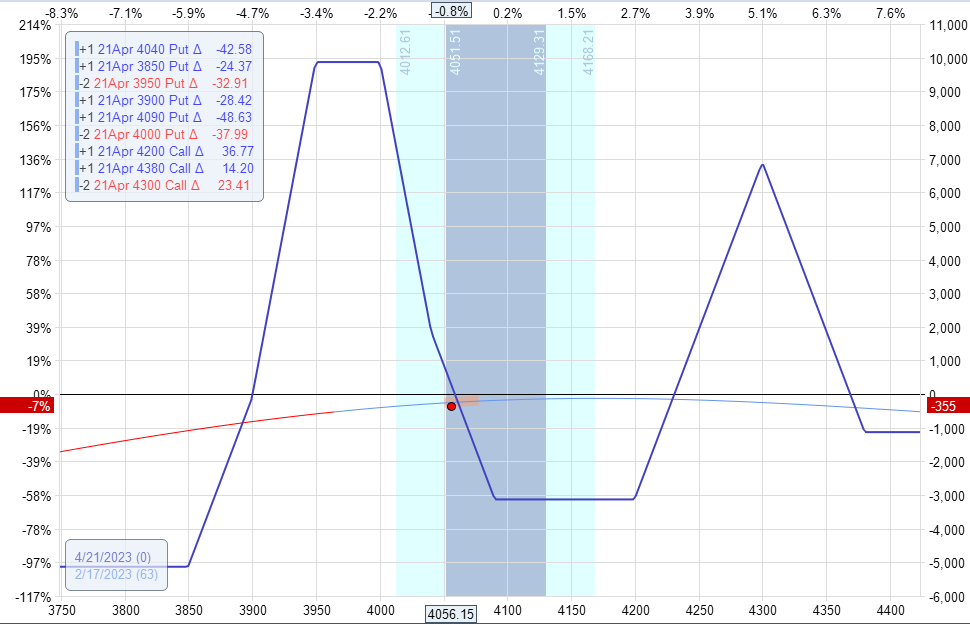

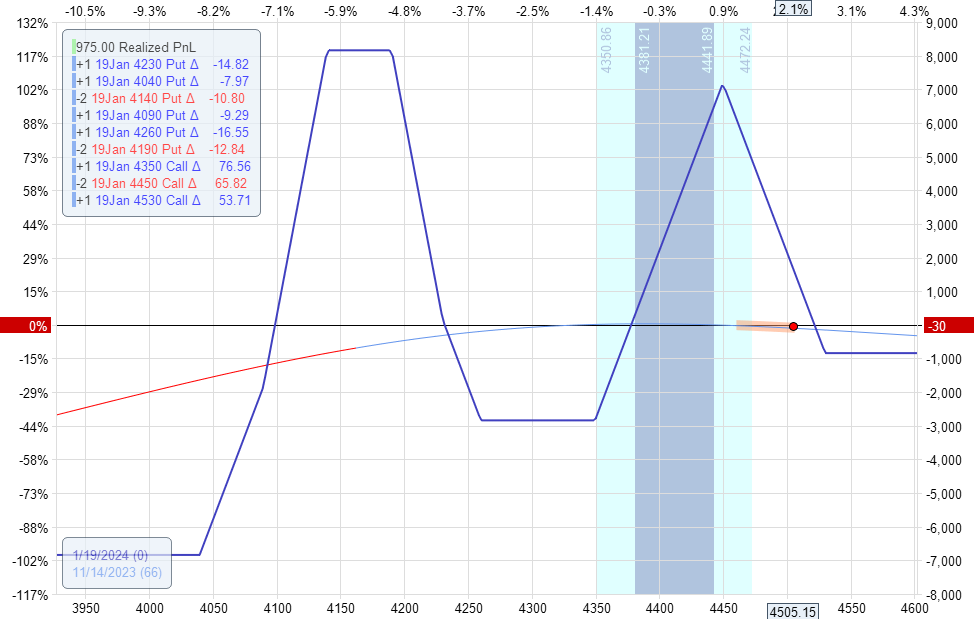

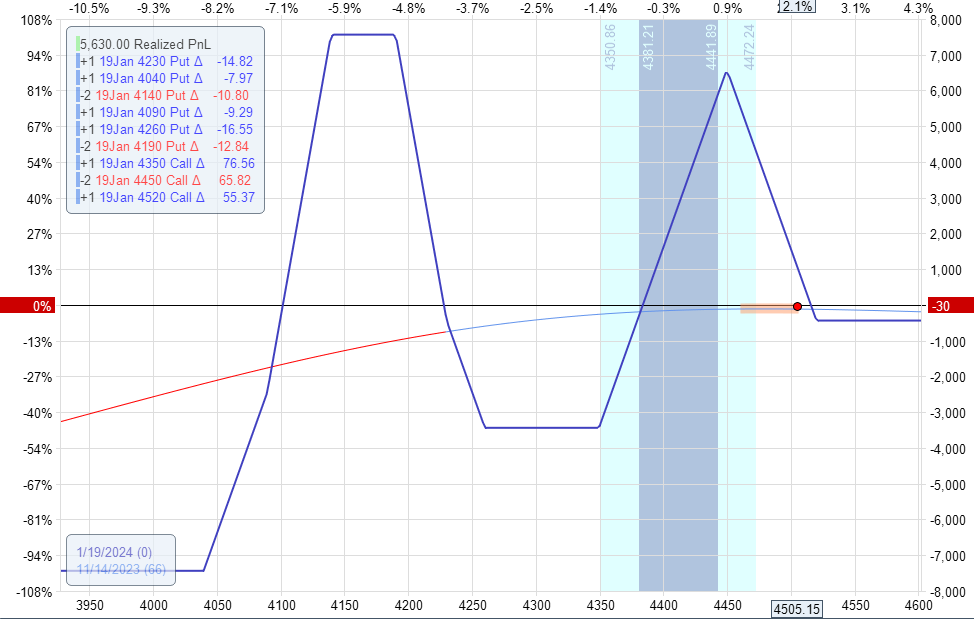

What To Do When The Price Of The Underlying Keeps Going Up?

Here, the price of SPX has gone above the short strikes of the upside butterfly.

Delta: -1.93

Theta: 8.4

Vega: -62.66

If this had been a calendar, we would have rolled the calendar up or added another calendar above the price.

With the fly having so many legs, we are reluctant to move the entire fly. And we don’t have to.

We can achieve the same effect of making the trade more bullish by rolling the upper leg of the fly down:

Buy one January 19, 2024, SPX 4520 call

Sell one January 19, 2024, SPX 4530 call

Delta: -0.32

Theta: 7.33

Vega: -66.3

Is The Expiration Of The Upside Butterfly The Same As The Expiration Of The Base Butterfly?

Yes, always.

It will be very problematic if you don’t make it as such.

Why Do You Use Call Options For The Upside Butterfly?

We use call options (as opposed to put options) because the butterfly is placed above the current price of the underlying.

As such, call options will be out-of-the-money.

If we had used put options, the options would be in-the-money.

We use call options since out-of-the-money options tend to be more liquid with tighter bid-ask spreads.

Closing Thoughts

Having the flexibility to use either calendar or fly adjustments will allow you to choose between the two, depending on the VIX.

In a high VIX (high volatility) environment, using a fly may be beneficial in terms of volatility.

Flies cost less when implied volatilities (IV) are higher.

When the market is in a sustained upmove, fly adjustments are much easier and have good risk reduction on the upside.

In a low VIX market, using a calendar may be beneficial if you feel the IV can not go any lower.

Personally, I still have a slight preference for the use of calendars as an upside adjustment.

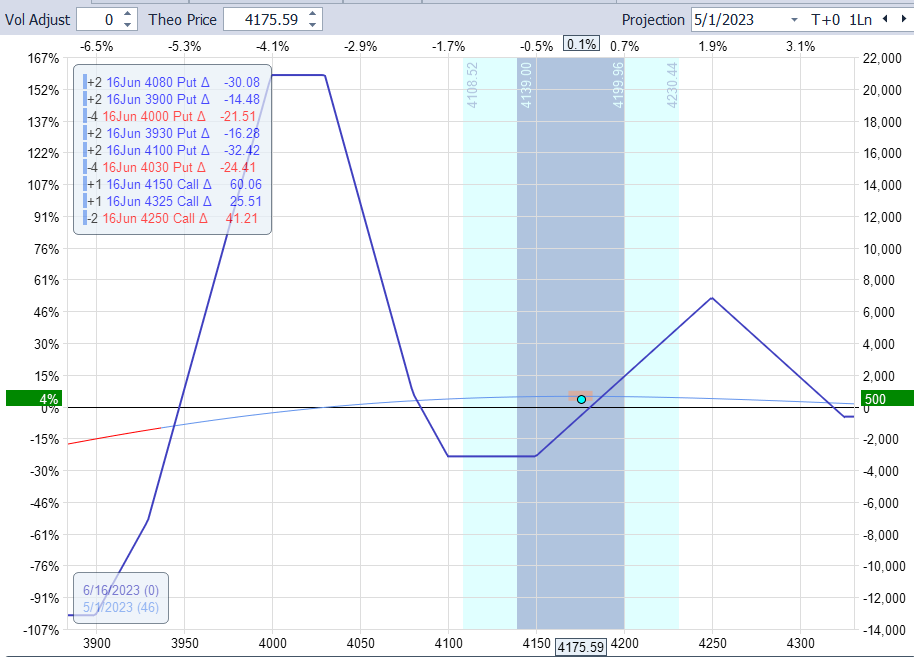

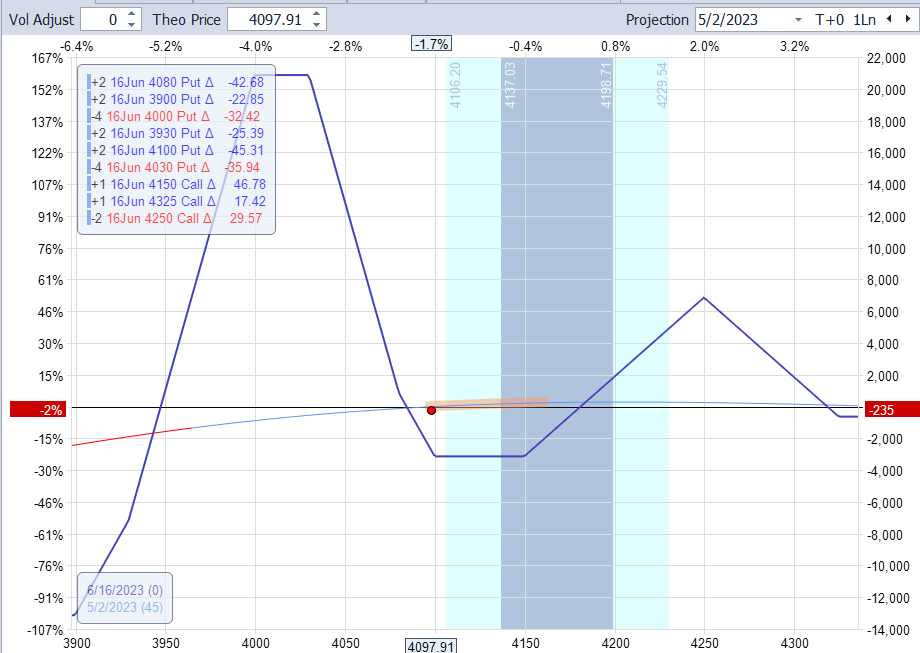

In addition to its positive vega balancing the negative vega of the Rhino, the following pictures are worth a thousand words.

May 1, 2023, SPX Rhino with an upside fly.

The next day, the trade went from being 4% in the green to -2% in the red when SPX dropped 78 points:

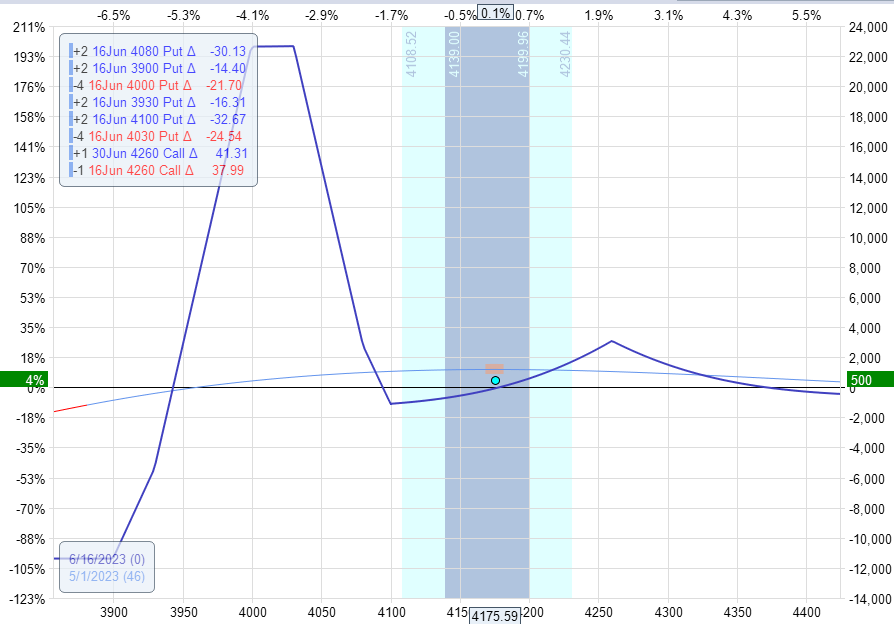

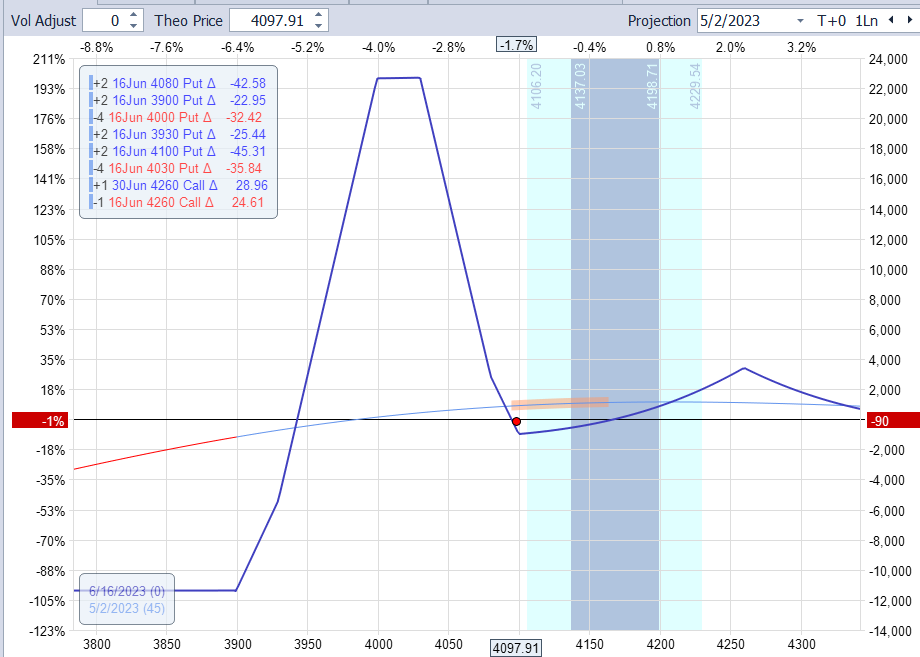

Here is the same trade with an upside calendar:

The trade performed slightly better when volatility increased as the market dropped:

An informal manual backtest of the Rhino using the upside fly versus the upside calendar shows that both are profitable during the bearish year of 2022 and the bullish year of 2023.

Which one did better in the backtest?

I wish I could tell you.

However, the numbers were so close that they were not statistically significant enough to determine which was better.

The reader is encouraged to backtest these themselves to see which one feels more comfortable.

It’s just like trying on shoes.

Buy the one that feels more comfortable.

We hope you enjoyed this article on trading the Rhino without calendars.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.