A double diagonal is not your average options strategy. Let’s take a detailed look at this little known strategy and see if it’s worthy of adding to your option trading arsenal.

We’ll look at:

Contents

- Strategy Overview

- Trade Setup

- Double Diagonal Greeks

- Maximum Gain

- Maximum Loss

- Breakeven Prices

- How Implied Volatility Impacts Double Diagonals

- Net Credit Or Debit When Opening The Trade?

- Dan Sheridan’s Tips For Entering A Double Diagonal

- What Instruments To Trade

- Managing The Trade

- Adjusting Double Diagonals

- Double Diagonal vs Iron Condor

- Turning A Double Diagonal Into An Iron Condor

- Using Double Diagonals In A Combination Strategy

- FAQ

- Conclusion

Strategy Overview

A double diagonal spread is made up of a diagonal call spread and a diagonal put spread.

It is a fairly advanced option strategy and should only be attempted by experienced traders, and as always, you should paper trade this for 3-6 months before going live.

The double diagonal is an income trade that benefits from the passage of time.

Implied volatility is a crucial element of this strategy as you will learn below.

Trade Setup

You would enter a double diagonal spread when you anticipate minimal movement in the underlying over the course of the next month.

As this is a long vega trade, you may also be of the opinion that implied volatility will rise over the next month.

This is the conundrum for double diagonal traders, they want volatility to remain flat or rise, yet they want the underlying to stay within a specified range.

Typically, volatility spikes are associated with large movements in the underlying.

Generally when entering a double diagonal trade, the underlying would be somewhere in the center of the two sold strikes.

You can also trade this strategy with a bullish or bearish bias, although most option income traders would set it up as delta neutral or as close to it as possible.

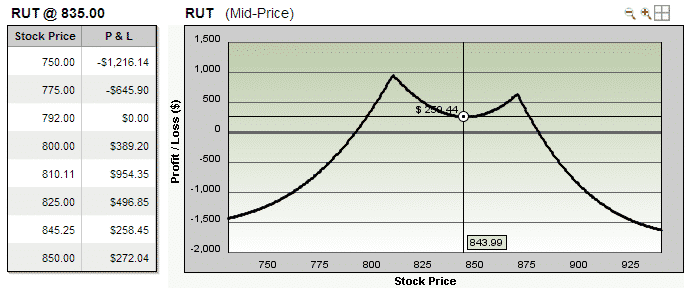

Here we see a fairly common set up for a trade using RUT:

Date: December 17th, 2012

Stock Price: 835

Underlying Implied Volatility: 19%

Trade Setup:

Sell Jan 17, 2013 810 Put @ $10.65. IV = 20.03%

Buy Feb 14, 2013 800 Put @ $15.10. IV = 21.01%

Sell Jan 17, 2013 870 Call @ $3.35. IV = 16.23%

Buy Feb 14, 2013 880 Call @ $5.55. IV = 16.32%

Net Debit: $665

The below payoff diagram shows the two profit peaks at 810 and 870 with a small dip in the middle.

The profit potential at the mid-point of the graph is around $250 assuming no change in implied volatility.

The capital at risk is about $1,665, so the profit potential in the middle of the graph is roughly 15% with a higher potential towards the peaks.

Double Diagonal Greeks

Looking at the option Greeks for this trade, Delta is basically flat, Theta is 10 and Vega is 62.

At the initiation of the trade, Vega has by far the most impact.

The two diagrams below show this trade with both a +3% and -3% change in implied volatility after 1 day.

You can see that a 3% move in volatility can have a significant effect on the trade.

Option Greeks at trade initiation

Day 1 with +3% move in Implied Volatility

day 1 with -3% move in Implied Volatility

Maximum Gain

Most standard option strategies have a clearly defined maximum profit.

However, calculating the maximum profit, maximum loss and breakevens for advanced option strategies like the double diagonal is an inexact science.

This is due to the fact that you are trading options with 2 separate expiry months.

Potential profit for this strategy is limited to the net credit received for the sale of the front month options, plus the net credit received when closing the back month options, less the original net debit paid for the back month options.

The ideal situation for this trade is that the underlying stays in between your short strikes.

Some traders may look at an expiry risk graph for a double diagonal and assume that it would be better for the stock to end near the short strikes.

It may be the case that you make a bit more when selling the back month options, however, having the underlying near your short strikes near expiry means there is an increased chance of the underlying blowing right past your short strike.

Maximum Loss

If you are able to open the position for a net credit, the maximum loss is limited to the difference between the strike prices, less the premium received.

If you open the position for a net debit, the maximum loss is the difference between the strike prices, plus the premium paid.

Breakeven Prices

There are too many variables to calculate an exact breakeven at expiry.

Most brokers, including ThinkorSwim and Interactive Brokers have profit and loss calculators that let you take into account potential changes in implied volatility levels.

The best way to look at your expiry graph would be to assume no change in volatility over the course of the trade.

Keep in mind that a decrease in implied volatility will bring your breakeven prices closer to your short strikes.

An increase in implied volatility will move them further away from your short strike.

How Implied Volatility Impacts Double Diagonals

Traders should have a solid understanding of implied volatility before attempting this strategy as it will have a significant impact on the trade.

The ideal scenario is for the underlying to stay within the two sold strikes until near expiration when you want volatility to spike up, ideally with a move towards the sold strikes.

Net Credit Or Debit When Opening The Trade?

When initiating a trade, it is preferable to try and receive a net credit, but it is not always possible, nor is it essential to having a profitable outcome.

The trade may be entered for a net debit and still make a profit if you can cover up the debit when you sell the back month options after the front month options.

When choosing whether to open a trade, it is more important to look at the expiration profit graph rather than the initial debit or credit.

Dan Sheridan’s Tips For Entering A Double Diagonal

Dan Sheridan is the guru when it comes to double diagonals, let’s take a look at the way he goes about entering a trade:

1. Sell the call option strike (minimum $0.50 for short option) in the front month, that is the first strike inside 1 standard deviation

2. Sell the put option strike (minimum $0.50 for short option) in the front month, that is the first strike inside 1 standard deviation

3. Buy a call one to two months out from the short call and up one strike (maximum 1.5 times price of the short call)

4. Buy a put one to two months out from the short call and down one strike (maximum 1.5 times price of the short call)

5. If the profit and loss graph sags in the middle, then bring the short and long options in 1 strike

6. If a negative skew of more than 2 exists (long month minus the short month), then don’t do the trade!

7. If a positive skew of 4 or more exists, then investigate

8. Know the earnings date and past gap potential

What Instruments To Trade

When trading double diagonals, it’s important to choose the right underlying stock, index or ETF. Here are a couple of guidelines to keep in mind:

- Stocks that are greater than $30

- Implied volatility (IV) is in lowest third of its two-year range

- Nontrenders, sideways movers

- Low volatilities (we want sideways movement, not wild swings)

- Skews (volatilities near and far) in line, not more than four points apart

- Nonearnings months — again, we don’t want movement due to news

- Boring, sideways, predictable industries, no biotech startups or the like.

Managing The Trade

Managing a double diagonal trade need not be as hard as you might think. Here are a few simple rules to follow that will help you achieve success with this strategy.

- Typically a double diagonal would be entered with between 30 and 60 days until expiration of the short options.

- Profit target should be around 15-20%

- Stop loss set at -25%

- If within 10 days of putting on the trade, the underlying is approaching one of your short options, you should consider adjusting or taking the entire position off.

- If after 10 days, your short strikes are hit, you should consider adjusting or taking the entire position off

- Generally you do not want to hold a double diagonal into expiry week of the short options.

- You can use back month options that are more than one month out from your short options. This will give you a greater long Vega exposure. To do this you would need to have a good understanding of how to roll option positions unless you plan on closing the entire trade when the front month nears expiration.

- You may want to use index options rather than ETF’s or stocks to avoid the risk of early assignment

- Avoid a saggy middle – no one likes a saggy middle, options traders included. To avoid a saggy middle on your profit graph, bring all your options in closer to the money

Adjusting Double Diagonals

Double diagonals can be tricky to adjust, particularly as you approach expiration. For tips on adjusting double diagonals, let’s again go to the master, Dan Sheridan.

During a webinar conducted on February 7, 2008, Sheridan gave an example of a trade entered on OIH.

Trade Date: Dec 10th, 2007.

Stock Price: $185

Underlying Volatility: 30%

Trade Setup:

Buy 1 April 200 OIH Call @ $8.70

Sell 1 Jan 195 OIH Call @ $3.30

Sell 1 Jan 175 OIH Put @ $3.60

Buy 1 Apr 170 OIH Put @ $7.90

Net Debit: $970

Capital at Risk / Max Loss: $1,470

OIH Double Diagonal – Opening Greeks

OIH Double Diagonal – Opening Risk Chart

By December 17th, OIH had dropped from $ 185 to $177 which was close to the short strike of $175.

This is how the trade looked at this point. As you can see, it was time to make an adjustment.

Risk Graph after 7 days and a drop of $8

Sheridan then goes on to present 3 different adjustment options:

Adjustment Idea 1

Buy to close the Jan 175 puts and Sell to open Jan 170 puts (changes put diagonal into a calendar).

With this adjustment, delta is reduced from 16 to 6 while Theta, Vega and Gamma all stay about the same. The adjustment cost $190.

Buy 1 Jan $175 OIH Put @ $6.30

Sell 1 Jan $170 OIH Put @ $4.40

Net debit: $190

Change in Greeks – Adjustment #1

New Risk Graph – Adjustment #1

Adjustment Idea 2

Sell to open Jan 170 puts and Buy to open Apr 175 puts (changes the put diagonal into a double calendar).

With this adjustment, delta is reduced from 16 down to 5, Theta is almost doubled from 7 to 12 and Vega is increased by 50% from 40 to 61.

The adjustment cost $800 and increased capital at risk because the position now has a double calendar in place of a single put diagonal.

Sell 1 Jan $170 OIH Put @ $4.40

Buy 1 Apr $175 OIH Put @ $12.40

Net Debit: $800

Adjustment #2 – Change in Greeks

Adjustment #2 – New Risk Graph

You can see that this adjustment has a much higher profit potential, but the trade-off is more capital at risk and a higher Vega exposure.

Adjustment Idea 3

Take off entire put diagonal and reposition down one strike for long and short puts.

With this adjustment Delta is reduced from 16 to 11, Theta and Vega stay the same and Gamma is down to -1 from -2.

Buy to close 1 Jan $175 OIH Put @ $6.30

Sell to close 1 Apr $175 OIH Put @ $10.20

Sell to open 1 Jan $170 OIH Put @ $4.40

Buy to open 1 Apr $165 OIH Put @ $8.50

Net Debit: $20

Adjustment #3 – Change in Greeks

Adjustment #3 – New Risk Graph

Double Diagonal vs Iron Condor

The double diagonal option strategy is a neutral options strategy that has a similar payoff diagram to an iron condor.

Both Iron Condors and Double Diagonals benefit from time decay, however one of the key differences is that double diagonals are long Vega.

In other words, increases in volatility will benefit double diagonals whereas they will hurt iron condors.

This is one of the major reasons attractions to this strategy, as a way to diversify some of the vega risk from trading iron condors.

The other way double diagonals differ from iron condors is that you are trading different expiry months.

Generally you would set up the double diagonal strategy by selling the near month options and buying options further out-of-the-money AND further out in time.

Turning A Double Diagonal Into An Iron Condor

One attraction of the double diagonal is that you can turn it into an iron condor after you close out the front month options.

To turn a double diagonal into and iron condor, simply close out the front month options, then sell to open options with the same strike in the same expiry month as the back month options.

Voila – you have an iron condor.

Some traders might use this strategy rather than simply selling a long term iron condor.

The idea being that you can generate twice the income by selling two lots of options.

Your rate of Theta decay will be higher using a double diagonal and turning it in to an iron condor as opposed to simply selling a long term iron condor.

This is due to the fact that your short options are always in the front month which experiences the highest rate of Theta decay.

Using Double Diagonals In A Combination Strategy

Double diagonals by themselves may not be an appropriate strategy for you when trading them in isolation.

One way to solve this problem is to use them as part of an overall combination strategy.

As double diagonal spreads are long Vega, you can use them in conjunction with your iron condors in order to decrease your Vega risk.

Below you see an example of a standard iron condor on RUT with strikes of 750-740 and 870-800 using 10 contracts.

You can see that delta is -30, Vega is -207 and Theta is 59. The payoff diagram is that of a standard iron condor.

Jan ’13 RUT iron condor Greeks

Jan ’13 RUT iron condor risk graph

Now, we add a double diagonal to the iron condor as such:

Buy 2 Feb 14th 730 Puts @ $5.64

Sell 2 Jan 17th 740 Puts @ 2.92

Buy 2 Feb 14th 890 Calls @ 3.04

Sell 2 Jan 17th 880 Calls @ 1.66

Net Debit: $820

We now have the following positions. You can see that delta is the same at -30, Vega is -91 and Theta is 65.

So Vega has been reduced from -207 to -91 which is a significant reduction. Theta has been increased from 59 to 65.

The ratio of Vega to Theta has reduced from 3.5 to less than 1.5.

This was using a ratio of 2 double diagonals for every 10 iron condors, but you can play with the numbers to work out a ratio that works for you.

Creating Rules Based On Implied Volatility

You can create rules in your trading plan depending on the current level of implied volatility.

For example, when volatility is low, you might want to add more double diagonals in order to increase your Vega.

The opposite is true when volatility is high, you might want to reduce the number of double diagonals in order to decrease your Vega.

What’s the catch you might be asking?

Well, you now have more capital at risk in the trade, with $11,000 at risk now opposed to $8,000.

However, the reduced Vega risk may help you sleep a bit better at night.

Iron condor traders are always concerned about volatility spikes, so maybe adding a double diagonal or two is the solution you have been looking for.

Looking at the profit graph below, you can see that your income potential if RUT stays exactly where it is, is reduced from $2,000 down to around $1500-$1600.

But, how often does an underlying stay in exactly the same spot over the course of a month?

How often have you had an iron condor position gradually drift up or down towards your short strikes?

FAQ

What Is A Double Diagonal Spread?

A double diagonal spread is a type of options trading strategy that involves buying and selling options at two different strike prices and two different expiration dates.

The strategy can be used to profit from a neutral market or a slightly bullish or bearish market. It is similar to the diagonal spread, but involves two different diagonal spreads.

How Does A Double Diagonal Spread Work?

A double diagonal spread involves buying and selling options at four different strike prices and expiration dates.

The trader buys a long-term call and put option at a higher strike price and sells a short-term call and put option at a lower strike price.

The trader then sells another set of short-term call and put options at a higher strike price.

The strategy is designed to generate income from the sale of the short-term options and to profit from the price movements of the long-term options.

What Are The Advantages Of Using A Double Diagonal Spread?

The advantages of using a double diagonal spread include the ability to profit from a neutral market or a slightly bullish or bearish market, the ability to generate income from the sale of short-term options, and the ability to limit potential losses through the purchase of long-term options.

Conclusion

Double diagonals are not a common option strategy, but they are one that many pro traders use.

At first glance they might look like a fantastic strategy, but you need to be careful and have a really good understanding of implied volatility and how to manage the position.

When used in isolation, the long Vega exposure might be too much for some traders.

However, using them in conjunction with other strategies, might be just the solution you were looking for.

Thanks for reading, now why don’t you go and paper trade some double diagonals and be sure to let me know what you think in the comments below!

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Gavin,

Simply an outstanding article!

I appreciate the amount of time and articulation you placed into writing about this strategy. I have not seen a more detailed explanation anywhere on the internet.

With Regards,

Marc

Thanks Marc, I felt like I needed to live up to the title. 🙂

Great, thanks very much

Dan, what are your thoughts on the risks and benefits of diagonal debit spreads ( i.e. short is further out of the money than the long) compared to diagonal credit spreads? Also, wouldn’t an earnings month be perfect (as long as the whole position is closed before the day earnings are announced) since the IV is steadily increasing?

Sorry, Gavin. Got Dan on the brain after reading your article! 🙂

No worries Boe. Yes that’s a valid strategy although I have never tried it myself. Do you have the ability to backtest? I know TOS has some good backtesting functionality.

Thanks for your quick reply, Gavin. I would love to backtest but don’t have OptionVue or a TOS account. Not sure what other programs or platforms have backtesting, but I guess a virtual account is a slow but steady way to go.

I’m also wondering how calendars and diagonals make a profit at and past the strike of the short, since the strike is at risk of being exercised.

Typically you would want to adjust before the stock breaks above your short strike. Even so, you’re unlikely to get assigned if their is time value left in the option, but you would need to be careful in the lead up to expiration, particularly if there is a dividend due.

You don’t have to worry about this on European Index style options. See here for more details:

https://optionstradingiq.com/index-options-vs-etf-options/

https://optionstradingiq.com/option-assignment-and-exercise/

Thanks again, Gavin. I did wonder if it was just that assignment lottery factor. I was recently relieved to discover you can avoid assignment due to the American short going ITM by buying it back the same trading day. I don’t have to trade just Europeans any more! 🙂

So I assume the reduction in the profit past the strike is because the short is then getting expensive to buy back.

Glad I could help.

Yes, that’s correct, the short is getting more expensive to buy back and the long option is not gaining as much because the delta is lower.

You are the man, Gavin! Thank you! 😀

Hi Gavin,

One last question. I am trying to understand the specifics of these two statements:

“If a negative skew of more than 2 exists (long month minus the short month), then don’t do the trade! If a positive skew of 4 or more exists, then investigate”

and

“Skews (volatilities near and far) in line, not more than four points apart”

Re the first statement, does this mean that, say for a Sept 55 call and Oct 60 call, where the Sept IV is 13, then the Oct IV should be no more than 15? Or does it mean Oct IV should be no less than 11?

Does the second statement mean that, say for a Sept 55 call & Oct 55 call, and Sept IV is 13, then Oct IV should be somewhere between 9 and 17?

Hi Boe,

As a general rule, you don’t want to much of a skew. As you are buying the back month option, you don’t want the buy high IV.

For your first question, the Oct implied volatility should be no less than 11 and no more than 17.

A negative skew (back month lower than front month) is fairly rare and is know as backwardation (as opposed to the more common contango). If front month volatility is much higher, it probably means there is some kind of economic event expected during the life of the front month option. A pending earnings release might result in this type of skew.

Got it! Thank you, thank you!

This seems to be awful close to Morris Puma’s BRIC trade, which I believe is some kind of Ratioed Diagonal and Condor to dial in neutral positions in vega, delta and gamma. I’m going to play around with them in a prob calc and see what happens.

I haven’t seen the BRIC trade, sounds interesting though.

Yes. Thanks for all your work articulating these concepts. I’m interested in what you think it would take to get this position. I’m not a shill for anyone, but just someone who is trying to synthesize some of the best ideas.

It’s a unique structure combining positive vega (what Dan Sheridan is pushing now http://info.sheridanmentoring.com/classes-and-courses/long-vega-strategies/) and negative vega (opposite sell side) with either adjustments or an original combination: http://youtu.be/3zJBU-DYUYs

It could also be an IC with -1 SD put debit spread (mickey mouse ear), 2 SD OTM calendar opposite the movement, and possibly adding one put to protect (mighty mouse ear): http://www.option-wizard.com/features/SFO%20200811_Dan%20Harvey%20Reprint.pdf

I’m a noob at these combos, but the claim is that the BRIC is a structure that has +/- vegas managed, presumably deltas and gammas too, so all you do is wait for theta. What do you think?

I think there’s not such thing as a free lunch. You can’t neutralize everything other than Theta, you will always have exposure to one other greek. My guess is that they are neutralizing Delta and Vega but will have Gamma exposure.

I know that I am pretty late to the game on this discussion but why would you not want to hold the front month shorts until/through the week of its expiry?

The risks are much higher in the last week. That’s why you sometimes hear the last week of an options life referred to as Gamma Week. Losses can mount pretty quickly from only a small price move if the stock is close to your short strike. Plus, if you are trading stocks there is the risk of early assignment.

Is this anything like Calendar Spread ( Time Spread)??? Thanks. RH.

Hi Robyn,

It’s similar to a calendar spread but there are subtle differences do to the long options being further away from the stock price.

Hi, thanks for the article. Wouldn’t these also be good for an earnings week? Sell the 2 shorts earnings week for high premiums, then buy the 30-40 dte longs? If stock closes that week between the 2 shorts, close whole spread for profit. using say the 16-18 deltas?

Yep I think that’s a pretty reasonable strategy.