Contents

The options collar strategy is similar to a vertical options spread.

But they are not identical.

Let’s try to understand why.

The collar strategy involves buying 100 shares of a stock, plus buying a protective put option, plus selling a call option.

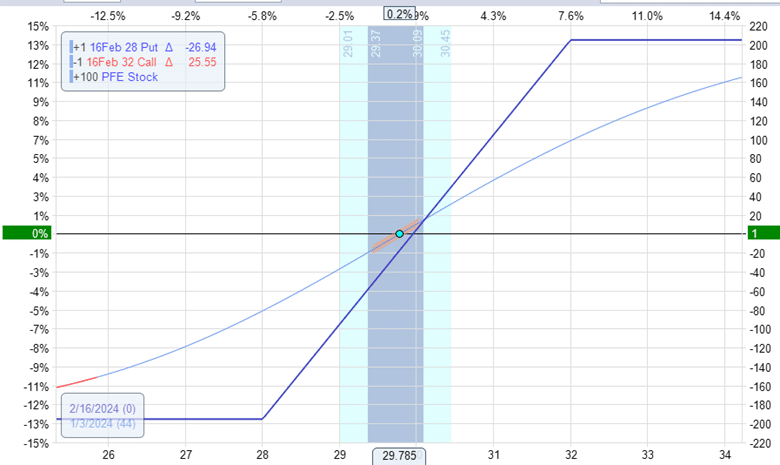

For example, the collar position on the stock Pfizer (PFE) is constructed as follows:

Date: Jan 3, 2024

Sell one Feb 16 PFE $32 call @ $0.41

Buy 100 shares @ $29.78

Buy one Feb 16 PFE $28 put @ $0.59

Net Debit: -$2995.50

The profit and loss graph looks like this:

The Greeks are:

Delta: 47.71

Theta: -0.1

Vega: 0.07

The shape of the expiration graph certainly looks similar to that of a vertical spread, doesn’t it?

As the price of the underlying stock increases along the bottom horizontal axis, the profit in the collar increases by the dollar amount shown on the right vertical axis.

Hence, the options collar is a bullish strategy.

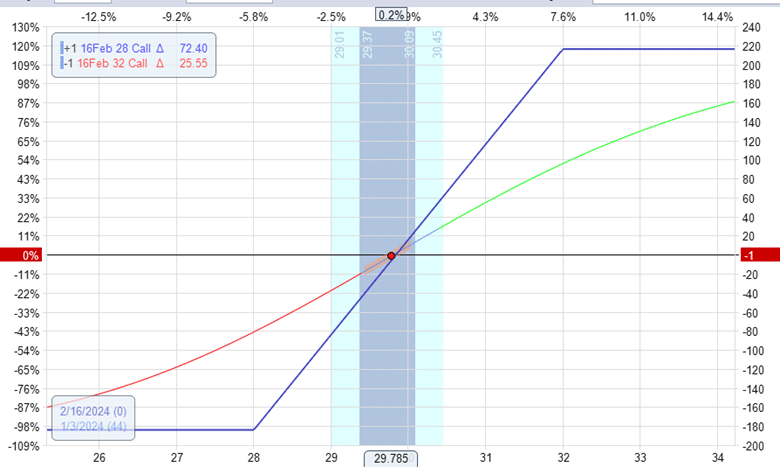

Bull Call Vertical Spread

Let’s compare that with a bull call vertical spread with the same underlying and expiration.

A bullish vertical spread is constructed by buying a call option and selling a call option at a higher strike price. We will use the same strike price as in the collar.

Remember that the vertical spread uses two call options, whereas the collar uses a call option and a put option.

Here are the specifics of the bull call spread

Date: Jan 3, 2024

Sell one Feb 16 PFE $32 call @ $0.41

Buy one Feb 16 PFE $28 call @ $2.25

Net Debit: -$184

We get the following profit and loss graph:

And the Greeks are certainly very similar to that of the collar:

Delta: 47.05

Theta: -0.03

Vega: 0.07

Compare the max potential profit in both graphs.

The highest point on the collar expiration graph is around $200.

The maximum potential profit in the vertical spread is around $220.

The max loss on the collar strategy is around $200, whereas the max loss on the vertical is $184.

They are not identical, but certainly within ballpark numbers of each other.

Capital Usage

Now, note the capital usage of the two strategies.

The vertical spread costs a debit of only $184.

This is the maximum possible loss that one can have in this vertical spread.

Because the collar strategy involves buying 100 shares of stock, it requires a capital usage of nearly $3000.

This is a big difference between the vertical spread and the collar.

Strategies that involve buying stock tend to be less capital-efficient than options-only strategies.

This capital efficiency is part of why people say options are leveraged instruments.

If one is taking a directional bullish bet on a stock, using a vertical spread rather than a collar is simpler and more capital-efficient.

However, the collar does have the advantage of receiving dividends if the underlying is a dividend-paying stock.

In our example, Pfizer pays a dividend yield of about 6% annually.

Because the vertical spread does not hold stock, it is not entitled to any dividends.

One reason that investors may end up with a collar is that they may already own the stock in the first place and decide to collar it to provide downside protection at the expense of capping upside gains.

Another reason is that investors may be trading other strategies, such as the Wheel or the 1-1-2 strategy, in which it is possible to end up being assigned stock, at which point the investor may decide to collar it.

How Did Each Do?

Since we have an example of a collar and an example of a vertical spread, how did each of them perform?

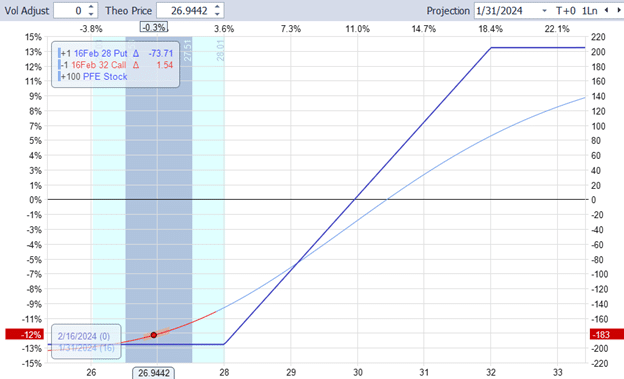

Let’s look at both P&Ls on Jan 31, when PFE dropped to $26.94.

The collar shows a loss of $183:

The vertical spread shows a similar loss of -$163.

Now let’s see what happens at expiration on Feb 16 when PFE closed at $27.62.

The short call expired worthless for the collar, and the put option is in-the-money.

The put option allowed the investor to sell the 100 shares at the strike price of $28 per share.

Therefore, the investor recouped $2800 from the original investment of $2995.50. That’s a loss of $195.50.

For the vertical spread, the short and long calls are both out-of-the-money and expired worthless.

The loss on the vertical spread is the entire investment of $184.

While the numbers are not exact due to pricing and execution fill differences, they are very similar. In theory, they should be the same.

Conclusion

The options collar and the bull call vertical spread are synthetically equivalent to each other.

Buying a stock in addition to a put option is synthetically equivalent to purchasing a long call.

Now, if you sell a call option again, you get a collar.

You get a vertical spread if you add a short call to the long call.

The two are equivalent.

The only slight difference is the potential dividend of owning the stock and differences in fill prices due to bid-ask spread differences.

We hope you enjoyed this article on the options collar compared to a vertical spread.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.