QYLD is one of the most popular income ETFs in the world, with over $8 billion in assets and a yield that typically sits around 11-12% annually.

For retirees hunting for monthly income, that number looks very attractive.

But there’s a version of this story that doesn’t get told in the fund’s marketing material: QYLD’s share price has declined at roughly 2% per year over its lifetime.

That income you’re collecting is partly your own capital coming back to you.

This article breaks down the real comparison, what QYLD actually does, how it compares to selling your own covered calls, and why the difference in outcomes over 10 years is larger than most investors realise.

Contents

- What QYLD Actually Does (And the Part That Matters)

- The NAV Erosion Problem

- The Total Return Comparison: Real Numbers

- What You Give Up With QYLD’s ATM Strategy

- Selling Your Own Covered Calls: The Three Advantages

- Who QYLD Actually Makes Sense For

- FAQ

- Summary

What QYLD Actually Does (And the Part That Matters)

QYLD, the Global X NASDAQ-100 Covered Call ETF, holds the stocks in the QQQ (the Nasdaq-100 index) and sells at-the-money covered calls against the entire position every month.

The premium collected from selling those calls is distributed to shareholders as monthly income.

On the surface, this is exactly the covered call strategy covered in our covered call guide. Sell calls against your stock holdings, collect premium, and generate income.

The critical detail is where QYLD sells its calls: at the money.

An at-the-money call has its strike set exactly at the current price of the underlying index.

This means that if the Nasdaq-100 goes up at all by expiration, even one point, the entire gain is captured by the call buyer rather than QYLD shareholders.

QYLD collects the maximum premium available for that month, then resets. Any upside in the underlying is systematically surrendered.

This is a structural choice, not an accident. At-the-money calls generate the most premium. They also cap every month’s participation in any positive market movement.

When you sell your own covered calls, you choose where to place the strike. Most income traders sell out-of-the-money calls at 5-10% above the current price, which collect less premium but retain meaningful upside participation if the stock rises.

The NAV Erosion Problem

This is the number that isn’t prominently featured in QYLD’s fund page.

Over the past 10 years, QYLD’s share price CAGR was approximately -2.1%.

The stock it holds, the Nasdaq-100, appreciated significantly over the same period. QYLD’s shares declined because surrendering all upside every month, in a market that spent most of the decade rising, means the fund consistently sells its growth potential for premium income.

The practical consequence: a retiree who bought QYLD 10 years ago at $25/share and collected monthly distributions of around $0.20-$0.23 has received significant income, but the shares now trade at roughly $17-$18 per share.

They’ve been collecting their own capital back in the form of distributions.

This is not inherently wrong as an investment approach, if you need income and you genuinely don’t care about the share price, receiving capital in the form of regular distributions is one way to generate cash flow.

But it’s not the same as generating income from a strategy that also preserves or grows your capital.

When you sell covered calls on your own stock portfolio at out-of-the-money strikes, the underlying stock retains the potential for some capital appreciation.

You’re generating premium income on top of capital that can still compound.

The Total Return Comparison: Real Numbers

Let’s put concrete numbers on the comparison.

Over the past 10 years, QYLD has underperformed QQQ with an annualised return of approximately 9%, while QQQ yielded roughly 19-21% annualised.

That’s a dramatic gap. A $100,000 investment in QQQ 10 years ago would be worth significantly more than the same amount in QYLD, even after accounting for QYLD’s much higher distribution yield.

But the relevant comparison for someone selling their own covered calls isn’t QYLD versus QQQ. It’s QYLD versus what you’d achieve running a conservative covered call strategy yourself.

A self-managed covered call strategy on quality stocks or a broad ETF, selling out-of-the-money calls at 20-30 delta:

– Collects approximately 8-15% annually in premium depending on the underlying and IV environment

– Retains stock appreciation up to the strike price

– Pays no management fees (QYLD charges 0.60% annually)

– Allows you to choose your strike based on current conditions rather than always selling at the money

– Lets you roll, adjust, or skip months based on market conditions

Over 10 years, the compounding difference between a strategy that preserves capital growth and one that systematically surrenders it is substantial.

Whether that gap persists in future will depend on market direction, volatility, and the specific strikes chosen by a self-managed investor.

Historically, over the past decade (a period dominated by a strong bull market in US equities) a self-managed covered call approach using out-of-the-money strikes would have produced higher total returns than QYLD, while generating broadly comparable annual income.

Past performance is not a reliable indicator of future performance, and in flat or declining markets the relative outcome can be very different.

What You Give Up With QYLD’s ATM Strategy

Beyond NAV erosion, there are several specific advantages you surrender when delegating to QYLD.

Strike selection. QYLD always sells at the money. You never have the option to let a strong earnings month run or to sell a more conservative strike when conditions are uncertain. The strategy is mechanical and inflexible by design.

Underlying selection. QYLD is locked into the Nasdaq-100. If you’re running your own strategy, you can write calls on dividend stocks you want to hold long-term, on sector ETFs with more favourable volatility profiles, or shift to SPY-based positions when QQQ vol is unattractive.

Tax management. In a taxable account, QYLD distributions are mostly treated as ordinary income. When you manage your own covered calls, you have control over timing, which months to collect premium, when to take short-term vs long-term gains on stock that gets called away, and how to layer positions across tax years. Our options for retirement accounts guide covers the tax treatment of options income in detail.

Responsiveness to IV. QYLD sells every month regardless of the volatility environment. When IV is very low, the at-the-money premium is thin, QYLD collects less income, and still surrenders all upside. When you manage your own positions, you can respond to IV conditions by selling more aggressively in high-IV months, reducing size, or extending duration in low-IV environments. Our high-IV vs. low-IV strategy guide covers how to calibrate for each environment.

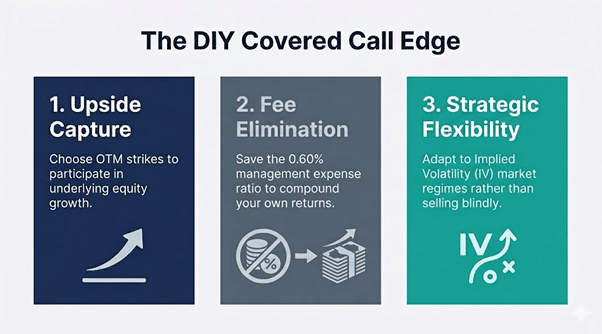

Selling Your Own Covered Calls: The Three Advantages

When you sell your own covered calls instead of delegating to QYLD, you gain three specific advantages that compound over time.

1. You keep capital appreciation. By selling calls 5-10% above the current price rather than at the money, you participate in moderate market gains. In a year where QQQ rises 25%, QYLD’s shareholders get only the monthly premium. If your covered call strike is 8% above entry and the market rises 25%, you capture the first 8% of that gain plus the premium, a meaningfully better outcome.

2. You eliminate the management fee. QYLD’s 0.60% annual expense ratio doesn’t sound large, but on a $300,000 position, it’s $1,800 per year, income you’ve paid to have someone execute a mechanical strategy you could run yourself. Over 10 years compounded, that’s a significant drag.

3. You control the exit. If a stock in your covered call portfolio makes an exceptional move, you can let it go and redeploy into a better opportunity. QYLD can’t do this; it holds the Nasdaq-100 and mechanically overwrites it every month. Your flexibility to rotate, concentrate, or exit positions is worth something.

Who QYLD Actually Makes Sense For

This isn’t an entirely one-sided case.

There are legitimate reasons to own QYLD.

Simplicity over optimisation. A retiree who has no interest in learning options mechanics, monitoring positions, or making strike selection decisions can own QYLD, collect distributions automatically, and never think about it. The cost of that convenience, the management fee, and the structural drag of the ATM strategy may be worth it for genuinely passive investors.

Very small portfolios. Running covered calls requires owning at least 100 shares of a stock or ETF. If a portfolio is too small to run multiple covered call positions with proper diversification, a covered call ETF provides access to the strategy without the concentration risk of owning only one or two positions.

Specific income needs. For investors who need to maximise monthly cash distributions regardless of total return, some retirees drawing down a specific dollar amount monthly, QYLD’s high distribution yield may serve that need more reliably than a self-managed strategy that produces variable income month to month.

For investors with sufficient capital to run multiple covered call positions and the willingness to manage them actively, a self-managed approach has historically produced stronger total returns than QYLD over the past decade.

Whether it suits a given investor will depend on their circumstances, time commitment, and tolerance for the additional decision-making involved.

FAQ

Q: Is QYLD’s 11-12% yield sustainable?

The yield is mathematically sustainable as long as QYLD keeps selling calls; the premium will always exist.

But if the underlying (the Nasdaq-100) is rising faster than the premium collected, the strategy will experience NAV erosion because it’s systematically selling off future gains.

In strong bull markets, QYLD tends to see its NAV decline. In flat or modestly positive markets, it holds value better.

Q: What about JEPI or JEPQ, are they better than QYLD?

JEPI (JPMorgan Equity Premium Income ETF) uses a different approach; it sells out-of-the-money index options rather than at-the-money calls and combines this with defensive stock selection.

This results in a lower yield (around 7-9%) but better NAV preservation in bull markets.

JEPQ applies a similar approach to the Nasdaq-100.

Both have historically preserved NAV more effectively than QYLD because they don’t sell all of their upside each month.

Whether they suit a particular investor depends on individual circumstances, including return objectives, income needs, and risk tolerance.

Q: How much capital do I need to run covered calls myself instead of owning QYLD?

A practical minimum is $30,000-$50,000, allowing you to own 100 shares each of 3-5 quality stocks or ETFs and run covered calls on all of them.

Below that level, the diversification is insufficient, and the per-trade costs become relatively significant.

Our options trading for retirement income guide covers capital requirements across different portfolio sizes.

Q: Can I own QYLD and also sell my own covered calls?

Yes, and some investors do, using QYLD for a portion of the portfolio (passive income) while running self-managed covered calls on individual stock positions they want to hold directly.

This hybrid approach captures some of the convenience of the ETF while retaining control over the core portfolio.

Summary

QYLD offers simplicity and consistent monthly distributions.

What it doesn’t offer, and what its marketing doesn’t emphasise, is capital preservation.

Selling at-the-money calls every month in a rising market means systematically surrendering growth, which is why the share price has declined over QYLD’s lifetime even as it distributed substantial income.

For investors willing to manage their own covered call positions, the advantages are concrete: you keep capital appreciation up to your chosen strike, you pay no management fee, you can respond to IV conditions rather than always selling mechanically, and you retain control over underlying selection and timing.

Looking back over the past 10 years, the data has favoured a self-managed covered call approach over QYLD on a total return basis, primarily because QYLD’s at-the-money strategy is structured to maximise short-term income at the cost of long-term capital growth.

Future results may differ depending on market conditions.

If you’re serious about building an income-generating options portfolio:

Options Income Mastery: Learn the complete wheel strategy including covered calls, cash-secured puts, position sizing, and adjustment techniques for consistent monthly cash flow ($397)

The Accelerator Program: Advanced training covering portfolio-level management, multiple income strategies, systematic approaches, and professional risk management techniques for serious traders ($997)

Related Articles:

- Selling Covered Calls: A Detailed Guide

- How to Generate Monthly Income with Options: A Retiree’s Guide

- 8 Covered Call ETFs for Income-Focused Investors

- Options for Retirement Accounts: The Ultimate Guide

- Wheel Strategy vs Covered Call: Which Generates More Income?

We hope you enjoyed this article on QYLD vs covered calls.

If you have any questions, send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.