When a stock begins to decline, a trader may initiate a bear call credit spread to profit from the bearish move.

As the stock falls, the spread typically gains value and accumulates unrealized profit.

However, markets do not always continue moving lower.

Sometimes a stock experiences a sharp V-bottom reversal, quickly recovering and rallying back upward.

When that happens, much or even all of the profit earned on the bear call spread can disappear.

In this article, we demonstrate a technique that allows a trader to lock in profits on a bear call credit spread after it has become profitable.

By making a simple adjustment, it is possible to eliminate the remaining risk in the position so that even if the stock stages a powerful V-bottom recovery, the trade cannot turn into a loss.

Contents

- Example On RUT

- Eliminating The risk

- Margin Reduction

- What Happened Next: The V-Bottom

- What To Do When The Condor Is Breached

- When This Technique Works — And When It Doesn’t

- Step-By-Step Summary

- FAQ

- Conclusion

- Take Your Options Income Trading Further

Example On RUT

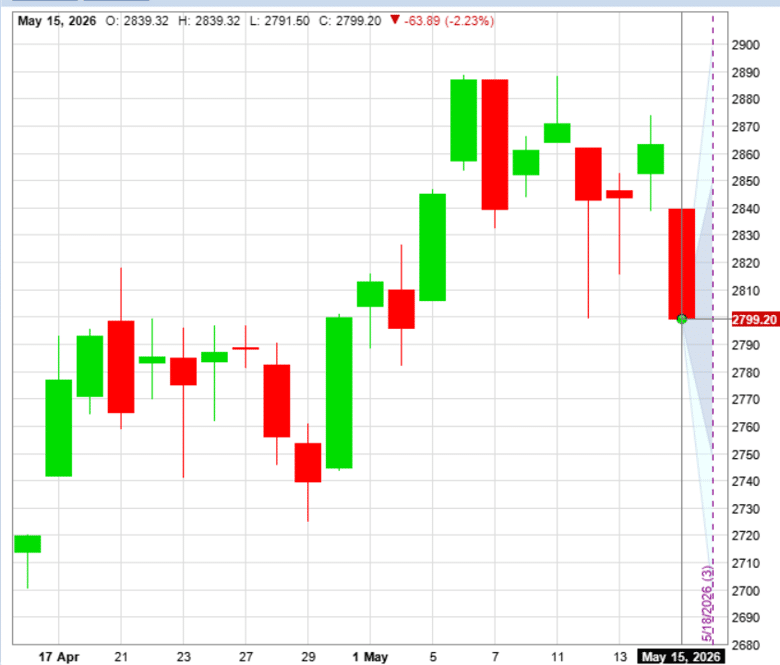

Friday May 15, 2026 was a bearish day for the RUT (Russell 2000) index.

At the last hour of trading, a trader initiates a bear call credit spread.

Date: May 15, 2026

Price: RUT @ 2799

Sell one contract June 26th RUT 2820 call @ $76.30

Buy one contract June 26th RUT 2830 call @ $71.20

Net Credit: $510

For this technique to work effectively, the bear call spread was placed relatively close to the current price.

This lowers the risk amount, giving the trade approximately a one-to-one risk-to-reward ratio — while still keeping the spread far enough out-of-the-money that positive theta works in the trader’s favour.

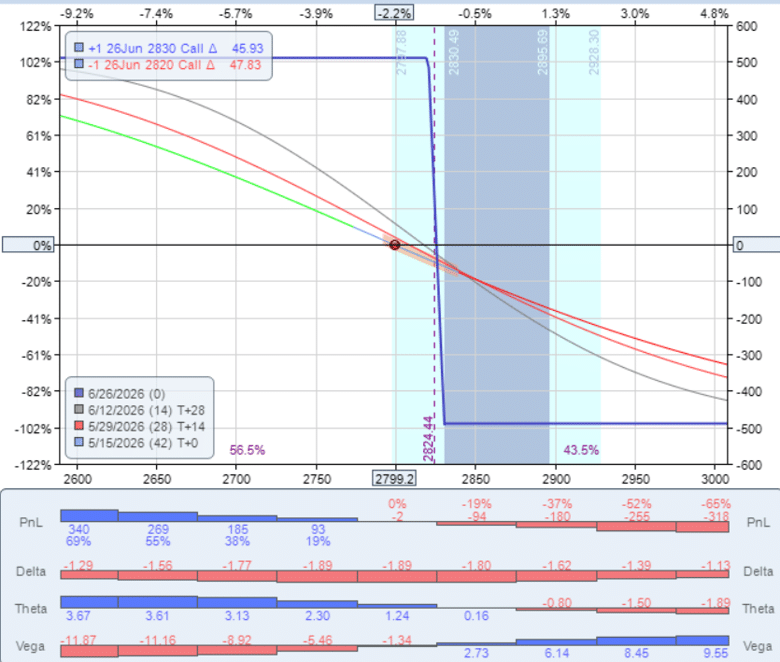

The trade has a theta of 1.26, which should increase as RUT declines and the spread moves further out-of-the-money.

The maximum risk in this trade is $490, calculated as the spread width minus the credit received:

$1,000 − $510 = $490

This $490 is also the margin used in the trade.

Eliminating The Risk

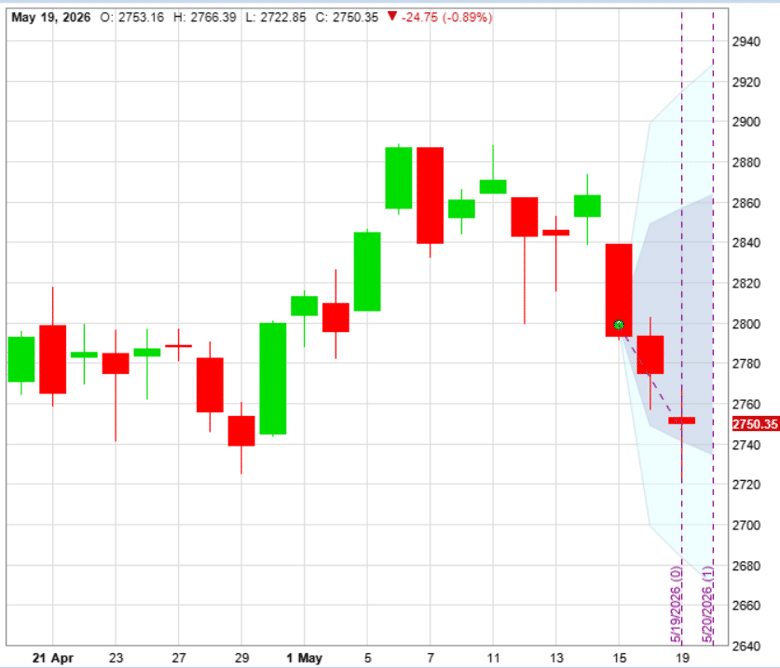

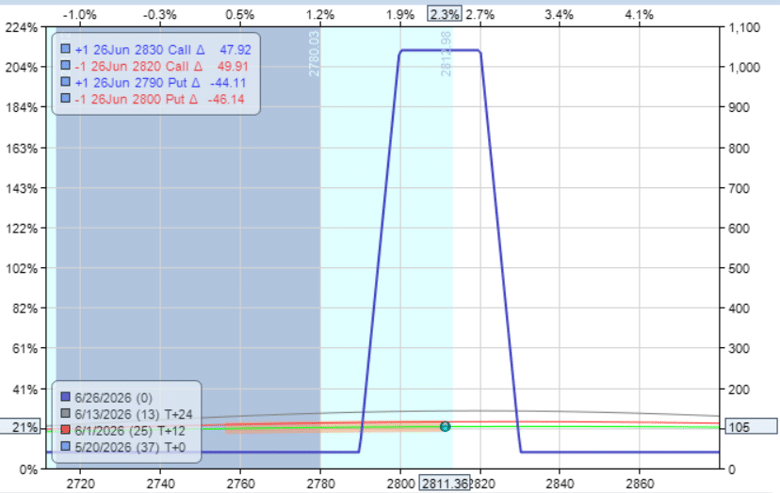

Two trading days later on May 19th, the bear call spread accumulated $105 of unrealized profit with the RUT declining to 2750.

With 2750 being near the previous low and potential support level, the trader becomes concerned that the market may stage a rebound.

He decides to eliminate the remaining risk in the position.

To accomplish this, he sells a bull put credit spread to collect enough credits to offset the existing risk in the trade.

Date: May 19th, 2026

Price: RUT @ 2750

Buy one contract June 26 RUT 2790 put @ $95.00

Sell one contract June 26 RUT 2800 put @ $100.30

Net Credit: $530

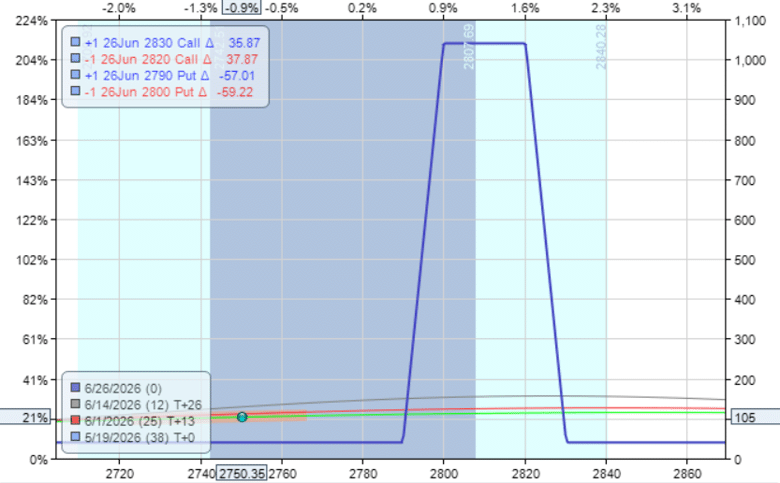

Recall the maximum risk in the original bear call spread was $490.

As long as the new bull put spread credit of $530 exceeds that maximum risk, the combined position becomes risk-free — the expiration graph never drops below zero profit.

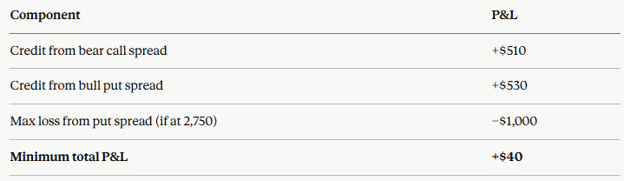

The worst that can happen is that the trade makes $40.

Because $530 – $490 = $40.

Here’s how the combined P&L works in the worst-case scenario — RUT expires between 2,790 and 2,820 (inside the condor):

The trade now has a floor.

No matter what the market does, the position cannot result in a loss.

Margin Reduction

An important secondary benefit of this adjustment is the reduction in buying power.

Many brokers recognise that the position has become a balanced iron condor with sufficient total credits to cover the maximum possible loss.

As a result, margin requirements may be reduced substantially or eliminated entirely, depending on the broker’s risk model.

This frees capital that can be deployed into other opportunities while the adjusted position continues working toward expiration.

For traders managing portfolio-level risk exposure, this adjustment is a useful tool for reducing a trade’s effective risk contribution without closing the position entirely.

What Happened Next: The V-Bottom

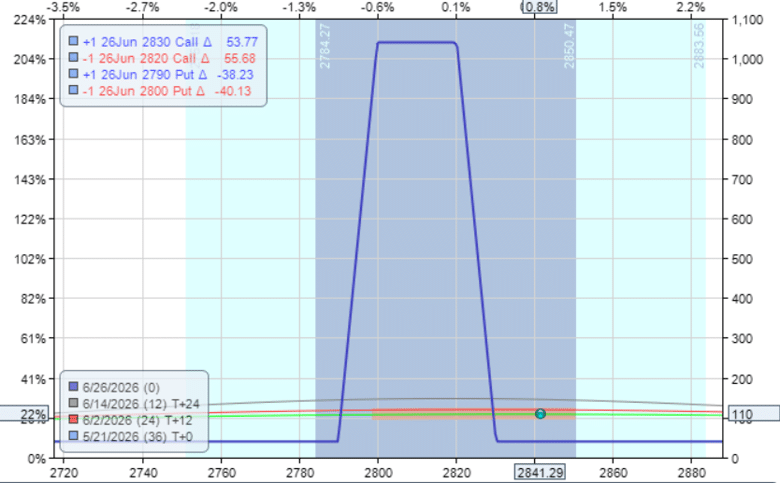

The next day, RUT rallied sharply back upward — exactly the scenario the adjustment was designed to protect against.

Because the bull put spread had been added and the position was now delta neutral, the trade did not lose money.

In fact, the combined position sat near the centre of the resulting condor structure.

Had the adjustment not been made, the original bear call spread would already be showing a slightly negative P&L at this point.

RUT continued to rally and moved through the upper breakeven of the condor.

The trader now has $110 of profit locked in — more than the $40 floor — and faces a decision.

The trader can decide to take the now $110 profit or hold.

What To Do When The Condor Is Breached

When the underlying moves outside the profit zone of the resulting condor, the trader has three options:

Close the entire position for the current profit.

If the position is showing a profit and the trader believes the directional move will continue, this is the cleanest exit.

Take the profit and move on.

In this example, closing at $110 profit is a reasonable outcome given the trade started with a maximum risk of $490.

Hold to expiration.

Because RUT is cash-settled, there is no assignment risk.

The minimum P&L is $40 regardless of where RUT closes.

If the trader is comfortable with the position and believes the market may pull back into the profit zone before expiration, holding is a valid choice.

Roll or adjust.

If the breach is aggressive and the trader wants to reduce further risk or extend the profit zone, rolling one of the spreads outward in strike or time is an option.

This adds complexity and should only be considered if the trader has a clear view on why it improves the expected outcome.

For most traders in most situations, closing for the available profit is the simplest and most disciplined choice when the condor is breached.

When This Technique Works — And When It Doesn’t

This adjustment is not available at trade initiation — several conditions need to be met before it becomes viable.

The original spread must have accumulated significant unrealised profit.

The new bull put spread credit needs to exceed the original spread’s maximum risk.

If the bear call spread has only moved slightly in your favour, the available put premium will not be sufficient to fully offset the remaining risk.

Implied volatility must be cooperative.

If IV has collapsed significantly since you entered the bear call spread, the available put premium may be thin.

The adjustment works best when IV is still elevated — often the case in declining markets — providing rich premiums on the new bull put spread.

Strike selection for the bull put spread matters.

Place the bull put spread below the current price at a level that represents genuine support — not so close that a minor bounce breaches it immediately, but not so far away that the premium is insufficient to cover the original risk.

In the example above, with RUT at 2,750, the bull put spread was placed at 2,790/2,800 — close enough to collect $530 in premium but still below the current price.

Step-By-Step Summary

1. Enter a bear call credit spread near the money with approximately a one-to-one risk-to-reward ratio

2. Allow the underlying to decline and the spread to accumulate unrealised profit

3. When the underlying approaches a support level or you become concerned about a reversal, calculate the remaining maximum risk in the bear call spread

4. Sell a bull put credit spread below the current price, targeting enough premium to exceed the original spread’s maximum risk

5. Confirm the combined credits exceed the combined maximum risk — the position is now risk-free

6. Hold to expiration or close for available profit if the condor is breached

FAQ

How Much Profit Does The Bear Call Spread Need Before I Can Make This Adjustment?

There is no fixed percentage.

What matters is whether the premium available from the new bull put spread exceeds the remaining maximum risk in the original spread.

As a rough guide, the bear call spread typically needs to have appreciated by at least 50–60% of its maximum profit before enough put premium is available to offset the remaining risk.

The further the underlying has moved in your favour, the more premium is available on the new spread.

Does This Technique Work On Individual Stocks?

Yes, but with additional considerations.

Individual stocks carry early assignment risk if your short strike goes in-the-money, you may be assigned shares before expiration.

Cash-settled indices like SPX and RUT eliminate this risk entirely.

On individual stocks, also be aware of upcoming earnings dates that could cause a large gap move through your strikes before you have a chance to manage the position.

What Is The Ideal Market Condition For This Trade?

The original bear call spread works best in declining or range-bound markets with elevated implied volatility.

The adjustment technique works best when IV is still relatively high after the underlying has declined.

This ensures the new bull put spread can collect sufficient premium to cover the original risk.

In a low-IV environment, available put premiums may be insufficient to make the adjustment viable.

Is The Resulting Position Just An Iron Condor?

Yes, once you add the bull put spread to the existing bear call spread, the combined position is structurally an iron condor.

The key difference from a standard iron condor entry is that this condor was built in stages, with the put spread added after the underlying declined, which means the total combined credit typically exceeds the maximum risk, making the trade risk-free or even guaranteed-profit at expiration.

Conclusion

The bear call spread risk elimination technique is a powerful tool for managing winning trades in volatile or trend-reversing markets.

Rather than hoping a profitable spread holds its gains until expiration, this adjustment converts the position into a guaranteed-profit iron condor, removing all downside risk while preserving upside potential if the underlying stays within the profit zone.

The key requirements are straightforward: the original spread must be sufficiently profitable, IV must be high enough to provide adequate put premium, and strike selection for the new spread must be disciplined.

When all three conditions align, the adjustment takes a good trade and makes it a certain winner.

For a deeper look at bear call spreads, the wheel strategy’s credit spread components, and iron condor management, see our related guides:

The Ultimate Guide to the Bear Call Spread

Iron Condors: The Complete Guide

Take Your Options Income Trading Further

Techniques like this — locking in profits and managing risk dynamically — are what separate systematic income traders from those who simply hope their spreads expire worthless.

Options Income Mastery covers the complete income trading framework, including credit spread management, adjustment rules, and how to build a consistent monthly income process.

We hope you enjoyed this article on locking in profits on a bear call spread.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Rut at 2750 selling 2800 put / buying 2790 put isn’t below market , if you got 530 you still have the $40 risk free with a small max profit zone 2800-2820. This trade has too much hopium for me writing the initial spread only 20 points otm even with the 50/50, but that’s just me.

The leg in for the risk free isn’t something I’ve considered with my condor setups and will in the future utilize. Thanks