The back ratio spread is an advanced options structure that can be done with all call or put options.

We never mix calls and puts in this spread.

It is termed a “ratio” spread because it involves buying and selling different numbers of contacts.

In our example, we will be buying two call options and selling one call option.

It is called a “back ratio” spread instead of the “front ratio” spread because we buy more contracts than we sell.

The front ratio spread is similar, except that it sells more contracts than it buys.

The back ratio spreads are done when a trader thinks the stock or underlying is about to make a big move.

The keywords here are “about to make.”

It will not be as effective if the stock has already made a big move unless the trader thinks that the stock will continue to make another big move.

What the trader does not want is to have the price of the underlying just sit there at the same price while the spread is in place.

This can happen if the stock has already made a big move and is now consolidating.

Contents

In our first example, we will use call options.

Call Back Ratio Spread Example

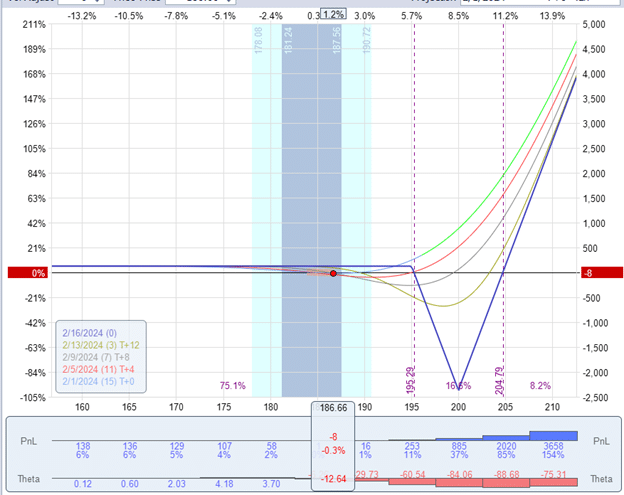

Suppose a trader sees on the earnings calendar that Apple (AAPL) reports earnings after the close on Thursday, Feb 1, 2024.

So, within the last hour of the trading session that day, he initiated a call-back ratio spread, hoping to capitalize on a large gap up or down in the price of Apple after the earnings report.

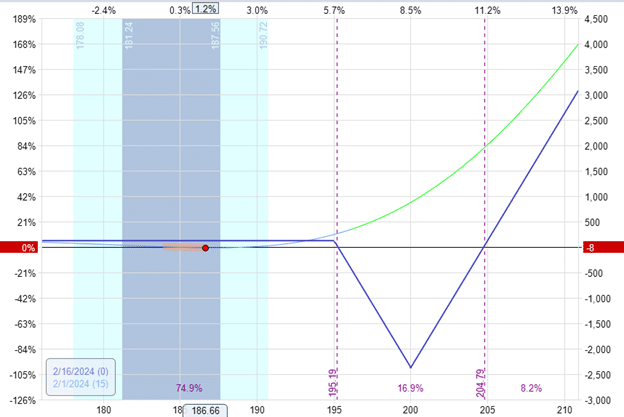

Date: Feb 1, 2024

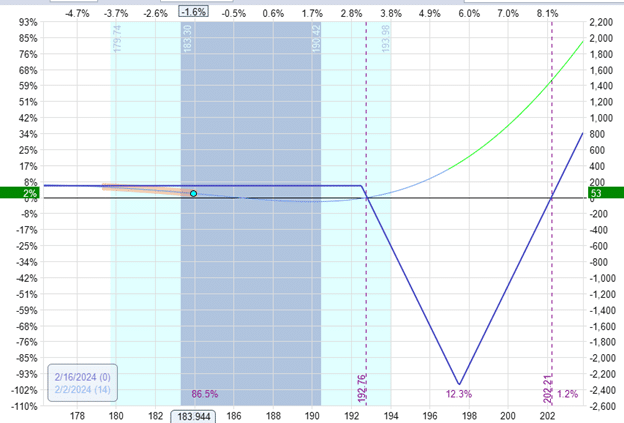

Price: AAPL @ $186.66

Sell five Feb 16 AAPL $195 call @ $1.37

Buy ten Feb 16 AAPL $200 call @ $0.56

Net credit: $125

You can think of this as five ratio spreads.

The ratio of the number of contracts we buy to the number of contracts we sell is 2 to 1.

Delta: -2.54

Theta: -12.64

Vega: 15.53

Gamma: 4.07

From the expiration graph and from the calculation, we can determine that the maximum risk of the trade is $2375.

This max risk is only experienced if AAPL closes at $200 at expiration.

The trader plans to close the trade in one or two days, so the maximum risk should never be experienced.

If closing in one or two days, the P&L graph to be looked at would be the T+1 or T+2 line, which will be closer to the shape of the T+0 (green line drawn above) rather than the expiration graph.

This trade has 15 days till expiration.

After The Earnings

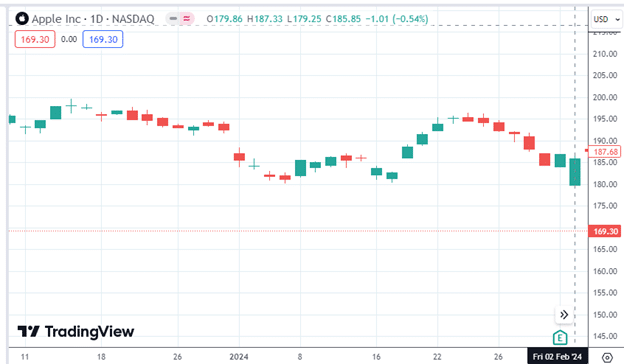

The next morning, AAPL gapped down on the open of Feb 2 and then came back up to close within range of the prior day:

Because the price was farthest away at the open, the spread’s P&L was highest at $107 five minutes after the market opened.

As the price came back up, we started to lose this profit.

At 45 minutes after the market opened, the P&L is at $80, and at this point, the spread can be bought back to exit the trade, representing a 3.4% return of the capital at risk.

Date: Feb 2, 2024

Price: AAPL @ $184

Buy to close five Feb 16 AAPL $195 call @ $0.33

Sell to close ten Feb 16 AAPL $200 call @ $0.12

Net Debit: -$45

Trade 45 minutes after the market opened:

If the trader had waited till near the end of the day, the profit would be only $42.

Is This A Directional Trade?

Some consider the call-ratio spread a bullish directional trade because it has unlimited reward when the price of the underlying moves up.

It has a small capped reward when the underlying moves down.

However, others consider the ratio spread a non-directional trade because its delta is fairly neutral at the start, and it can make money regardless of whether the underlying price goes up or down.

In this example, the trade’s strike selection was made in such a way as to have a small delta at the start, and it was planned as a non-directional trade, assuming that the trader has no opinion as to whether AAPL will gap up or down on earnings.

As we’ve seen, this so-called “bullish” call ratio spread made money even when the underlying stock price went down.

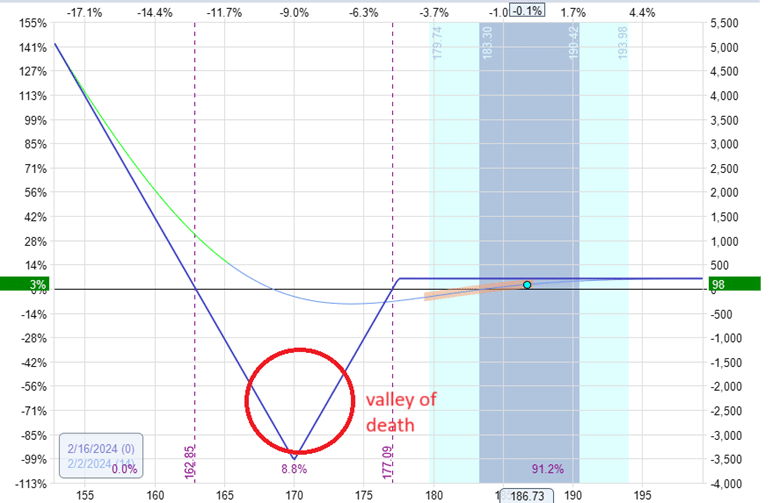

And yet others may consider it a bearish trade because they prefer to have the price go in the direction away from the high reward side (since it has to pass through the valley of death to get there).

Tweak The Strikes

Let’s see if we tweak the trade to have a positive delta, to begin with, as in the following:

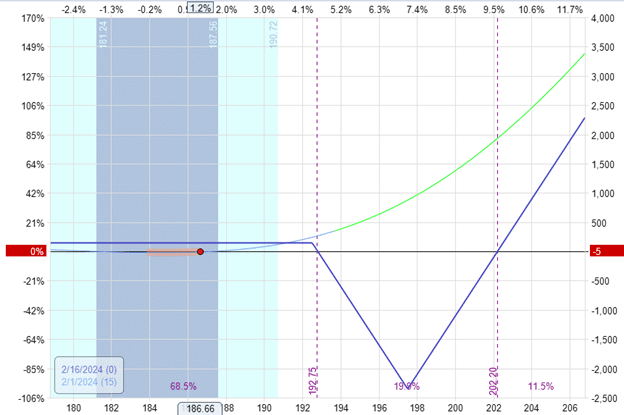

Date: Feb 1, 2024

Price: AAPL @ $186.66

Sell five Feb 16 AAPL $192.5 call @ $2.07

Buy ten Feb 16 AAPL $197.5 call @ $0.89

Net credit: $145

Delta: 12.45

Theta: -24.95

Vega: 28.63

Gamma: 7.27

The model still shows a profitable P&L of $52.50 the next morning…

So, the price movement away from the initial price is the biggest contributor to the profit.

The more the price moves, the greater the profits.

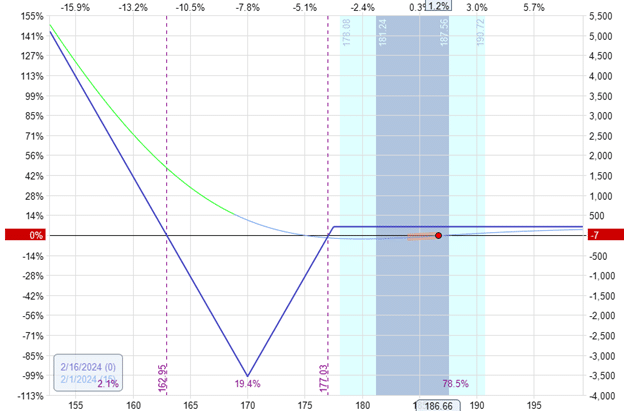

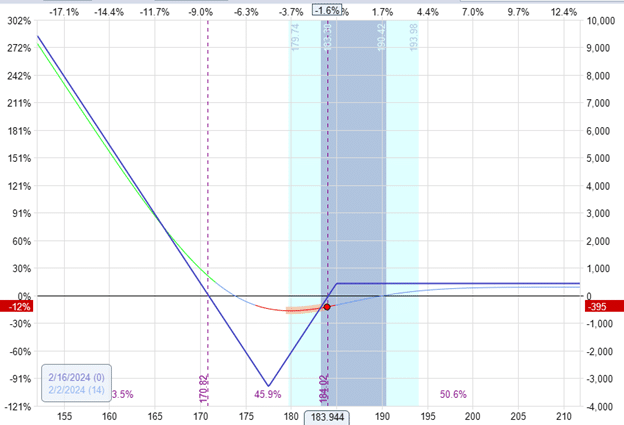

Put Back Ratio Spread

The put-back ratio spread looks like the mirror image of the call-back ratio spread.

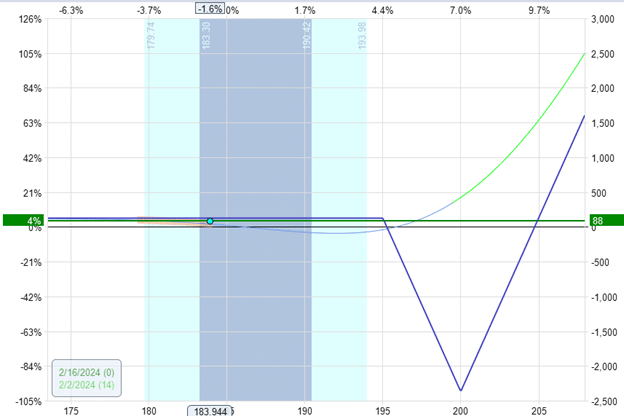

Date: Feb 1, 2024

Price: AAPL @ $186.66

Sell five Feb 16 AAPL $177.5 put @ $1.38

Buy ten Feb 16 AAPL $170 put @ $0.48

Net credit: $210

Delta: 17.49

Theta: -11.11

Vega: 4.90

Gamma: 0.72

The next morning, it resulted in a slightly negative P&L of -$37.50.

However, as the price increased (away from the Valley of Death), the P&L started profiting until it reached $97.50 in the late afternoon:

The ratio spread appears to favor the price moving away from the Valley of Death.

This implies that starting the spread with the price too close to the valley is also not a good idea.

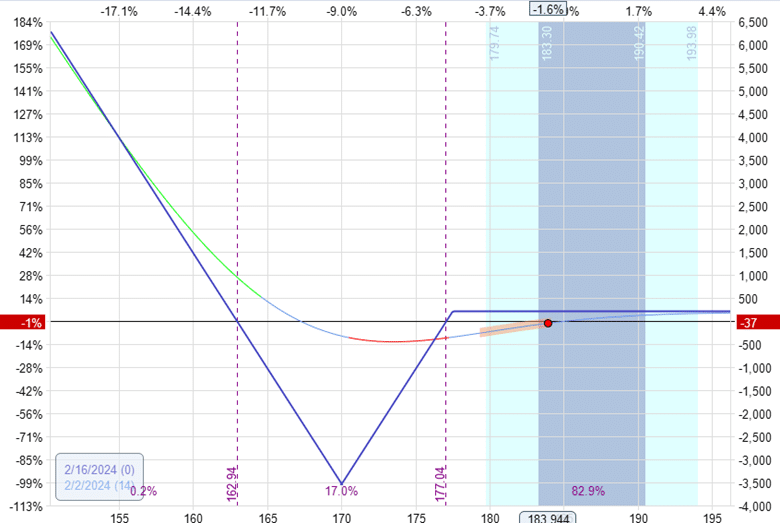

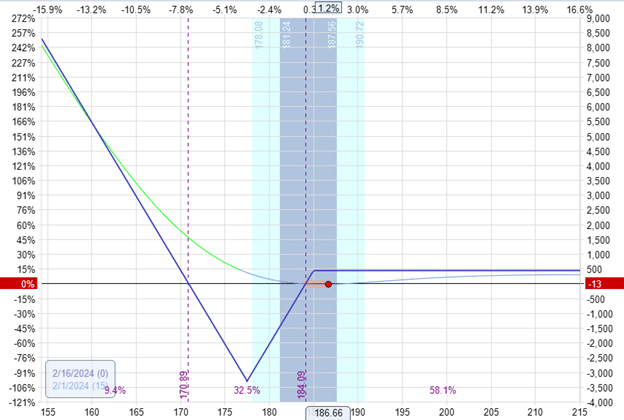

Price Too Close To The Valley of Death

To prove the point, what if we start the trade with the price being close to the valley like this:

Date: Feb 1, 2024

Price: AAPL @ $186.66

Sell five Feb 16 AAPL $185 put @ $3.66

Buy ten Feb 16 AAPL $177.5 put @ $1.39

Net credit: $440

Delta: 5.69

Theta: -41.94

Vega: 32.99

Gamma: 7.23

And the next morning:

It is down 12% with a P&L loss of -$395.

This trade started with the price being too close to the valley, and the price went in the wrong direction into the valley.

In addition, the back ratio spread, with a greater number of long options, is negatively affected by the volatility crush during the earnings announcement.

Note that it has positive vega.

The closer the long strikes are to the current price (as in the case of this last example), the larger the vega and the volatility effects.

Frequently Asked Questions

Is the back ratio spread positive or negative theta?

It depends.

It is a negative theta, to begin with.

And if the price goes towards the valley, it becomes even more negative:

However, if the price moves away from the valley, the trade can have some small positive theta, as seen from the theta histogram above.

That is why some traders will get out of the trade as soon as the price gets into the valley but are willing to linger in the trade longer if the price is “in the handle” away from the valley.

Is the Back Ratio Spread The Same As The Backspread?

This back ratio spread is also known as the “backspread.”

However, this is a misnomer. There are no back spreads in options.

There are ratio spreads.

The “back” or “front” are adjectives that describe the type of ratio spread.

Hence, “back ratio spreads” is the preferred name.

Can Ratio Spreads Be Done In IRAs?

Certain IRA accounts will not allow ratio spreads.

You have a naked short strike because the front ratio spread involves selling more options than buying.

A naked short call requires the highest options privileges, which may not be allowed in certain IRA accounts.

However, it may be possible to construct a back ratio spread by putting in two separate orders.

For example:

Order 1:

Sell five Feb 16 AAPL $195 call @ $1.37

Buy five Feb 16 AAPL $200 call @ $0.56

Order 2:

Buy five Feb 16 AAPL $200 call @ $0.56

If the account allows selling bear call spread (order #1), and it certainly allows buying long calls (order #2), then this would be equivalent to our first example of a call-back ratio spread.

Conclusion

The ratio spread can have some complex, nuanced behaviors.

By modeling various scenarios, we conclude that the ratio spread benefits from price moving away from the valley unless the directional move is so great that it can jump across to the other side of the valley.

If the price falls into the valley and we continue to hold the trade while it is there, that is the death of the trade.

We hope you enjoyed this article on how to trade the back ratio spread across earnings.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Great article, thanks for sharing.

1. Price Too Close To The Valley of Death – how faraway price range we should consider for back ratios spread?

2. Can we do back ratios 3-4 months out? what to watch out for?

3. If we do fall into valley of death, how to recover/repair the trade?