Discover what caused the 2018 Volmageddon crash that destroyed inverse volatility products like XIV, and learn how to protect your options portfolio from the next extreme VIX spike event that experts are calling Volmageddon 2.0.

Contents

- Understanding Volmageddon: The 2018 Volatility Crisis

- What Happened During Volmageddon?

- The VIX Spike That Changed Everything

- What Happened To Short Volatility Strategies?

- The Death Of XIV And Inverse Volatility Products

- Why The Volatility Spike Was So Extreme

- Mainstream Media On Volmageddon 2.0

- How To Protect Against Volmageddon 2.0

- FAQs About Volmageddon

- Conclusion: Trading Safely In High Volatility

Understanding Volmageddon: The 2018 Volatility Crisis

“Volmageddon” is not a word in the dictionary.

It was a term coined by the derivatives industry that refers to the extreme market event that occurred on February 5, 2018. As of this writing in November 2025, we’re still awaiting what many are calling “Volmageddon 2.0.”

People are speculating that it is not a matter of “if” but “when” it would happen.

“Volmageddon 2.0” is the next volatility event that will happen that is similar to (if not larger than) the event on February 5, 2018.

I don’t know who specifically came up with the word, but I would admit that it is a catchy name.

The Origin of the Term

The word “Armageddon” is a word found in the dictionary.

It originates as a biblical reference to the location of the place where the last battle between good and evil will be fought.

The key word here is “last,” as in “last battle.”

The implication here is that this battle would destroy the world, and hence there would be no next battle afterward.

Armageddon has now come into popular usage to refer to any dramatic and catastrophic event likely to destroy the world or the human race.

Volmageddon is a play on that word where the prefix “vol” refers to volatility.

Options investors who employ short volatility strategies will know it well because they rather say “short vol” for brevity instead.

What Happened During Volmageddon?

On February 5, 2018, the Dow Jones Industrial Average lost more than 1,500 points during intraday trading.

This is its biggest intraday point drop in history up to that time.

That is not to say that it could not make larger intraday swings in the future.

The DOW finally closed down by 1,175 points for the day.

Understanding how market volatility affects options prices is crucial for any options trader navigating these extreme market conditions.

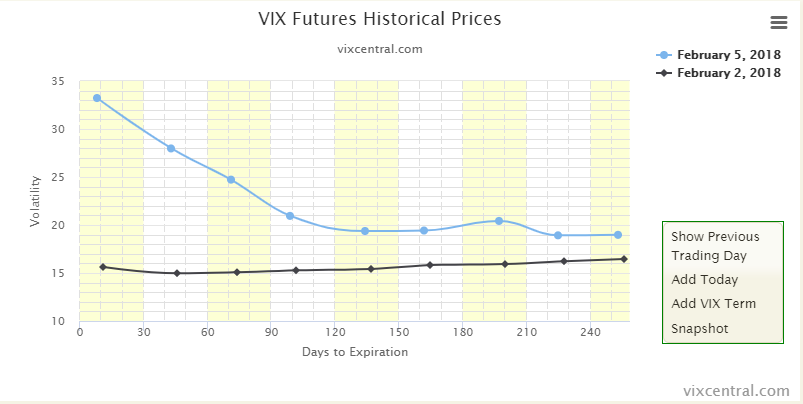

The VIX Spike That Changed Everything

It is natural that when market indices drop, the VIX will rise. The VIX is the CBOE Volatility Index, often referred to as the “fear index” and used as a measure of market volatility.

That day was accompanied by an extreme spike in volatility, where the VIX rose from 17.16 to 37.32 (close to close), a spike of 117% — the largest VIX spike till then.

For options traders, understanding implied volatility and how it impacts your positions is essential for risk management during volatile periods.

What Happened To Short Volatility Strategies?

When VIX goes up by such a large amount, it financially damages certain exchange-traded products (ETPs).

Specifically, the “inverse volatility” products are hardest hit.

Inverse volatility products are funds that capitalize on falling volatility.

They are designed to profit when volatility falls and vice versa.

When volatility rises (as in the spike in the VIX), they lose value.

Prior to the event was the growing popularity of these inverse volatility products leading to an over-crowded “short vol” space.

Many options traders were using strategies like iron condors and credit spreads which also benefit from falling or stable volatility, though these defined-risk strategies fared much better than the inverse volatility ETPs.

Ready to Master Volatility-Based Strategies?

Learning how to trade during high volatility periods and protect your portfolio from extreme events is crucial for long-term success.

Discover proven strategies for managing risk:

- Options Income Mastery: Learn systematic approaches to selling options safely, including position sizing and risk management techniques that protect you during volatility spikes ($397)

- The Accelerator Program: Master advanced volatility strategies, portfolio Greeks management, and crisis navigation techniques used by professional options traders ($997)

Both programs teach you how to trade profitably while protecting your capital during extreme market events like Volmageddon.

The Death Of XIV And Inverse Volatility Products

Among products such as SVXY, UVXY, etc., one very popular inverse volatility product was XIV — an obvious play on the reverse spelling of VIX.

I used the word “was” because XIV no longer exists.

It was terminated when it lost 96% of its value during Volmageddon.

Somewhere in the legalese, there must have been a clause that mentioned that termination of the product is a possibility if the product loses 80% of its value, and if such an event occurred, investors would likely lose the entirety of their investment.

Many investors do not read such legalese, nor do they believe that such an event could happen.

Unfortunately, it did.

This is why using defined-risk option strategies like spreads and combinations is so important — your maximum loss is always known upfront.

SVXY is still around, but check out the drop in Feb 2018!!

Why The Volatility Spike Was So Extreme

What was unusual was why volatility increased so much when the S&P 500 dropped only about 4% that day.

I’m not saying that 4% is not a significant drop.

But one would think such a large volatility increase would only occur in a much larger market crash.

Many investors also did not understand how these inverse volatility products derived their value.

It is not based on supply and demand but rather on the end-of-day rebalancing of first and second-month VIX futures contracts.

Those ETPs that did not get terminated lost a significant amount of value.

The SVXY chart from that period shows a dramatic cliff-like drop — rarely seen even in the most volatile of stocks.

Understanding options Greeks like gamma helps explain why these products moved so violently during the volatility spike.

Mainstream Media On Volmageddon 2.0

Can this type of event happen again?

Sure, it can.

The mainstream media is calling it Volmageddon 2.0.

In February 2023, CNBC titled their media piece “Volmageddon 2.0: How Options are Influencing Markets”, where it says that zero-DTE options are now estimated to make up about 50% of the daily volume of the S&P500 index options.

The Wall Street Journal asked the question in its article, “Are 0DTE Options creating the next Volmageddon.”

In an article published in investing.com, J.P. Morgan’s chief global markets strategist, Marko Kolanovic, said that the rise of trading near-term U.S. equity options could trigger the next one.

The proliferation of zero-DTE options trading has created new dynamics in the market that could potentially trigger another extreme volatility event.

Access Our Best Options Trading Resources

Before you continue, get instant access to our most popular options trading guides and resources:

Download Our Best of Options Trading IQ Collection – Includes comprehensive guides on volatility trading, risk management, and option strategies.

How To Protect Against Volmageddon 2.0

Always use defined-risk spreads or combinations thereof.

The worst thing that you can do is to short the VIX by selling a naked call option.

You get a small premium for doing it.

But if VIX skyrockets through the roof, the short call will be deep in the money, and you will be obligated to buy back the short call at expiration for a very high price.

If VIX is insanely high at that time, your net loss is theoretically unlimited — especially if your expiration is short and there is no time for the VIX to calm back down prior to the expiration of the option.

Recommended Protection Strategies:

- Use Defined-Risk Spreads: Always trade vertical spreads instead of naked options to cap your maximum loss

- Manage Position Size: Never risk more than 2-5% of your account on any single trade, even with defined-risk strategies

- Monitor Portfolio Greeks: Keep your portfolio delta and vega exposure within manageable levels

- Use Stop Losses: Implement adjustment rules that automatically trigger when positions move against you

- Diversify Across Time: Don’t concentrate all your positions in the same expiration cycle

For a comprehensive approach to managing risk during volatile periods, check out our guide on reducing gamma risk on iron condors.

FAQs About Volmageddon

How is Volmageddon different from the Flash Crash?

The Flash Crash refers to May 6, 2010, when the DOW dropped almost a thousand points (or about 9%) intraday, only to recover most of that loss within minutes.

In this case, the blame was placed (rightfully or not rightfully) on high-frequency trading algorithms, which caused a cascade of selling.

Volmageddon is a more sustained market event that lasted several days.

What other names has Volmageddon been referred to as?

Volmageddon has been referred to by other names such as “Volpocalypse” and “Volnado.” But the name that stuck with mainstream media is “Volmageddon.”

Can retail options traders survive a Volmageddon 2.0 event?

Yes, absolutely — but only if you’re using proper risk management.

Traders using defined-risk strategies like credit spreads and iron condors with appropriate position sizing can survive and even profit from volatility spikes.

The key is never trading naked options or using undefined-risk strategies when selling volatility.

Should I stop trading options because of Volmageddon 2.0 concerns?

No.

The lesson from Volmageddon isn’t to avoid options trading — it’s to avoid reckless strategies like naked short positions and leveraged inverse volatility products.

With proper risk management techniques and defined-risk strategies, you can navigate volatile markets successfully.

How often do Volmageddon-type events occur?

Major volatility spikes occur irregularly, but understanding historical market patterns helps.

While the 2018 event was unprecedented in its magnitude, smaller volatility spikes happen several times per year. Preparing for the worst while trading systematically is the key to long-term success.

Conclusion: Trading Safely In High Volatility

Just remember that the VIX can go up dramatically and unexpectedly.

This is what makes shorting the VIX and other variants of that strategy a bit dangerous.

The use of defined-risk options structures would be wise.

Whether you’re trading the wheel strategy, diagonal spreads, or iron condors, always ensure you know your maximum risk upfront and size positions appropriately.

The key takeaway is this: Volmageddon didn’t destroy all options traders — only those who were using undefined risk strategies or didn’t understand the products they were trading.

By using systematic approaches, defined-risk strategies, and proper position sizing, you can build a sustainable options income trading business that survives (and potentially profits from) the next volatility crisis.

Related Articles

- 10-Part Iron Condor Course

- Understanding Implied Volatility

- How to Adjust Iron Condors

- Options Greeks Explained

- Best Iron Condor Strategy

- Credit Spread Basics

We hope you enjoyed this article on Volmageddon 2.0.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.