The Jade Lizard options strategy is a strategy where the investor is looking to collect premium and limit the risk to one direction which is generally the downside.

The trade is similar to an iron condor but contains one unprotected side which means the trade involves naked options and is therefore not suitable for beginners.

Let’s take a deep dive into this popular options strategy.

Contents

- Trade Setup

- Maximum Loss

- Maximum Gain

- Breakeven Price

- How Volatility Impacts The Trade

- How Theta Impacts The Trade

- Other Greeks

- Risks

- Jade Lizard vs Iron Condor

- Jade Lizard vs Big Lizard

- Summary

Trade Setup

To construct a Jade Lizard options strategy an investor will sell an out of the money put, and simultaneously sell a bear call spread that is also out of the money.

The goal of the Jade Lizard strategy is to collect premium where the aggregate premium collected from the naked out of the money put and the sold call spread is greater than the difference between the two calls.

This way, the trade has effectively zero risk on the upside.

For example, let’s assume and investor sells an out of the money put with a strike price of $20 that expires in 1 month on XYZ stock for $0.80 when XYZ is trading at $22.

The investor will also simultaneously sell a $24-$25 call spread for $0.30, to make the total premium collected from the trade $1.10 ($0.80 + $0.30).

The only risk that the investor assumes on this trade is downside risk. If XYZ stock moves above $25 per share, the investor would lose $1 on the call spread, but gains $1.10 from the premium collected for a net gain of $0.10.

The investor profits from the trade unless the price of XYZ moves below the strike price of the naked put by more than the premium that is collected. In this example the stock price would need to drop below $18.90 ($20 – $1.10).

< Download 9 FREE Bestselling Option Books >

Investors who are participating in the Jade Lizard options strategy are attempting to find a stock with volatility skew.

The skew should be a smirk which means that the implied volatility of the “out of the money” puts are higher than the “at the money” strike implied volatility and the implied volatility of the “out of the money” calls are lower than the “at the money” calls.

In this circumstance the investor is selling options volatility that is rich (in terms of the OTM puts), and purchasing an option that is relatively inexpensive (in terms of the OTM call).

The best situation for an investor that trades a Jade Lizard strategy is that the security they are trading remains trapped in a tight range during the tenor of the trade allowing the investor to pocket the entire premium.

The most important aspect of the trade is to limit your risk to one side.

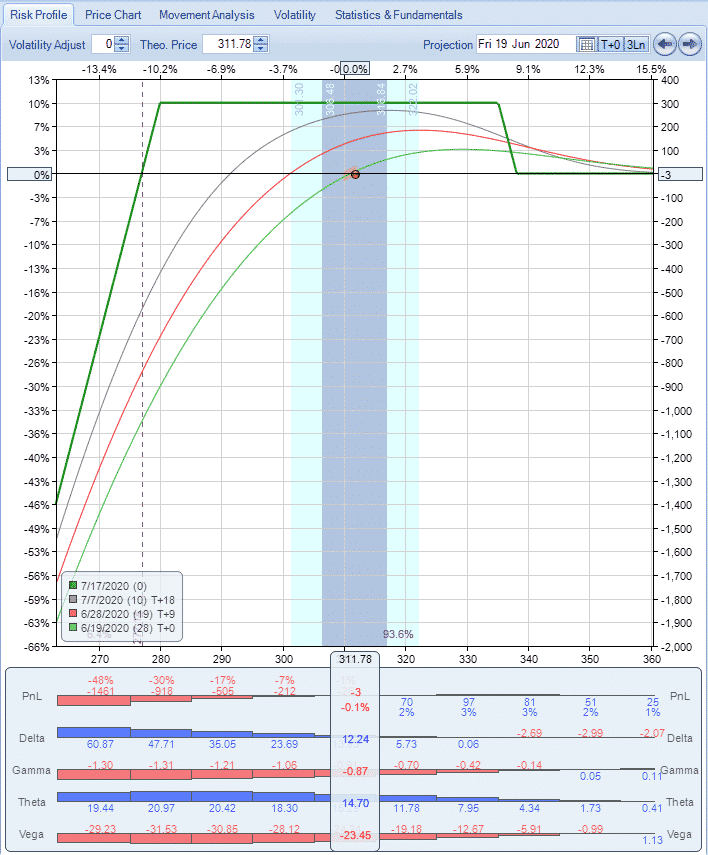

Let’s look at an example using SPY.

Date: June 18, 2020

Current Price: $311.78

Trade Details: SPY Jade Lizard

Sell 1 SPY July 17th $280 put @ $2.76

Sell 1 SPY July 17th $335 call @ $0.95

Buy 1 SPY July 17th $338 call @ $0.68

Premium: $303 net credit

The call strikes are 3 points wide and we have generated $300 in premium, which means there is zero risk on the upside.

The biggest risk with the trade is a sharp fall early in the trade. This makes sense given the naked put and the positive delta of the trade.

Maximum Loss

If the trade is constructed correctly, there will only be one side of the trade that has the chance of suffering a loss.

Unfortunately, the potential loss on that side is substantial because of the naked put. Still, it’s no greater than a cash secured put.

The loss on the put side is unlimited until the stock reaches zero. In our example, the maximum loss is equal to $27,700, which is calculated by taking the 280 strike price x 100 less the $300 premium received.

Maximum Gain

The maximum gain is limited to the combined premium received for selling the put and selling the call spread.

In the above example that is equal to $303.

Breakeven Price

If the trade is constructed correctly, there will be no breakeven price on the call side because the worst that can happen is the trader ends with a small profit.

This is reliant on the option premium received being more than the distance between the two call strikes.

On the put side, the breakeven price will be equal to the short put strike less the premium received.

In our example, this is equal to $277 which is calculated as the 280 strike less the $3 premium received per contract.

How Volatility Impacts The Trade

Similar to an iron condor this trade is short volatility or negative vega. That means that an increase in implied volatility after entering the trade will be bad for the position.

Vega is the greek that measures a position’s exposure to changes in implied volatility. If a position has negative vega overall, it will benefit from falling volatility. You can read more about implied volatility and vega in detail here.

Looking at the SPY example above, the position starts with a vega of -23. This means that for every 1% rise in implied volatility, the trade should lose $23

The opposite is true if implied volatility drops – the position would gain $23.

How Theta Impacts The Trade

This type of trade is positive Theta trades in that it makes money as time passes, with all else being equal.

This is due to the fact the trade involves selling a naked put and selling a call spread. Generally speaking, option strategies that involve selling options are positive theta.

In our example, the trade has positive Theta of 14. This means that, all else being equal, the trade will gain $14 per day due to time decay.

Other Greeks

DELTA

Jade Lizard’s are a positive delta trade because the positive delta from the sold put is much higher than the negative delta from the short call spread. This SPY example trade had delta of 12.

This is an equivalent exposure to owning 12 shares of SPY.

GAMMA

This trade has negative gamma. Gamma is one of the lesser known greeks and usually, not as important as the others. I say usually, because you’ll see further down in this post why it can be really important to understand gamma risk.

The initial gamma on the SPY trade was quite low at -0.87.

Risks

It goes without saying that as a positive delta trade, we have a risk that the price of the underlying will fall sharply causing an unrealized loss, or a realized loss if we close the trade.

Volatility risk is also a consideration for jade lizard traders.

As mentioned on the section on the greeks, this is a negative vega strategy meaning the position benefits from a drop in implied volatility. If volatility rises after trade initiation, the position will likely suffer losses.

Jade Lizard vs Iron Condor

The main difference between a jade lizard and an iron condor is that the sold put is unprotected. This gives the trade much higher profit potential, but it also exposes the trader to a lot more risk due to the naked put.

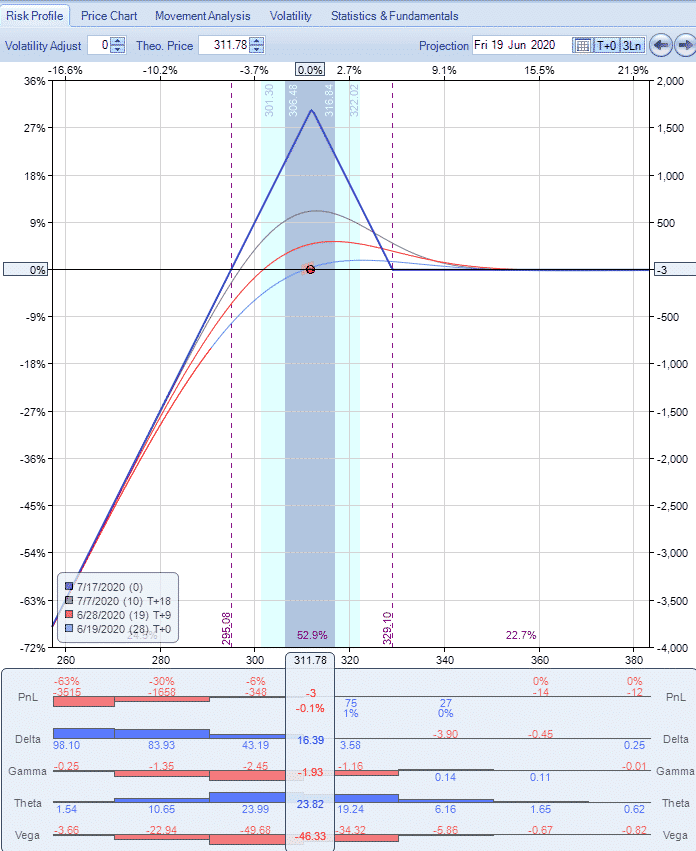

Jade Lizard vs Big Lizard

A big lizard involves selling the put and the call at the same strike rather than them being spread out.

That gives the trade more of a straddle look rather than a strangle / iron condor look.

The big lizard has a tent-shaped profit zone, like a put ratio spread while the jade lizard has a flat profit zone which is more like an iron condor.

Below is the setup for a Big Lizard.

Date: June 18, 2020

Current Price: $311.78

Trade Details: SPY Big Lizard

Sell 1 SPY July 17th $312 put @ $10.22

Sell 1 SPY July 17th $312 call @ $8.57

Buy 1 SPY July 17th $329 call @ $1.84

Premium: $1,695 net credit

In this example, the breakeven on the Big Lizard is much closer at $295 and the profit zone in much narrower.

Summary

A jade lizard is an advanced strategy that involves selling a naked put and selling an out-of-the-money call spread.

The trade is taking risk on the put side in order to create a trade that has zero risk on the call side.

The trade aims to take advantage of volatility skew by selling an expensive out-of-the-money put and leaving it unprotected.

Usually the trade has quite a wide zone of profit, similar to an iron condor.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Wish you had given Liz and Jenny of Tasty Trade credit for naming Jade Lizard

This exact trade can be called Jade Lizard but different versions of the strategy has been around for ages, I could not care less what the name is and who the credit belongs to. It is an excellent article, Gavin Thanks for sharing!

I only say this because women are often not given credit for what they do, esp in the stock market business

It seems a little un-necessary to rename an existing standard strategy … a put ladder … which can be executed on most exchanges as a single trade …. as a Jade Lizard …. which cannot be executed on most exchanges as a single strategy?

very nice strategy i’ve found this article very valuable this will definitely help me at avapartner thanks.

Thanks for this article. Tasty Trade stresses the importance of high IV. Do you have experience with this strategy in low IV times?

Hi Uwe, it’s not something I would do in a low vol environment, the premium on the puts just isn’t worth it.