I can not answer this question.

It is like asking how many miles this car can go on one gallon of gas.

First of all, it depends on the type of car.

If it is an electric car, it can go with zero gallons of gas.

Then, it depends on the size of the car, the load, and how the driver drives.

Is it mostly highway driving or stop-and-go?

The theta of a butterfly depends on the number of contracts, the underlying assets, the wing widths, the implied volatility, the days-till-expiration, the position of the fly in relation to the current price, and other factors.

Typical butterflies will have positive theta, assuming they are reasonably constructed and not extremely far from the current price.

I’m not talking about the bent, out-of-shape, wackily constructed flies far out of the money, in which case they can have negative theta.

Contents

Calculating Butterfly Theta

Butterflies with positive theta will profit from the passage of time due to the different rates of decay of the different options for the legs of the butterfly.

A butterfly is made up of three legs – two long legs and one short leg, as in the following example:

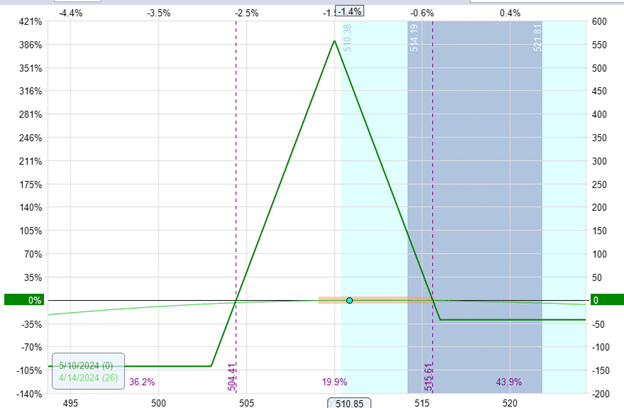

Date: April 12, 2024

Price: SPY @ $510.85

Buy one May 10 SPY 503 put

Sell two May 10 SPY 510 put

Buy one May 10 SPY 516 put

This is one contract of a butterfly or a one-lot butterfly.

The long legs are the 503 put option and the 516 put option because they are the options that we are buying.

The 510 strike is the short leg because we are selling (or shorting) that option.

It is an at-the-money butterfly because the short 510 strike is close to the current price of the underlying.

We are using the SPY (the S&P 500 ETF) in this case.

The overall position theta for this butterfly is 1.13.

This number tells you the number of dollars the butterfly is expected to increase each day if all else stays the same.

It is a theoretical number because we know things will not stay the same.

Let’s look at only the long put option at the strike price of $516.

This option has a theta of -0.13 on a per-share basis.

On a per-contract basis, if an investor buys this put option, it will lose $13 each day from time decay.

The negative sign in theta means that the option (if purchased) will lose money from the passage of time.

Because options have an expiration date, their extrinsic value must go to zero.

Therefore, the option loses value each day as it gets closer to expiration.

Similarly, the long put option at strike at 503 will lose $14 per day.

We sold two put options contracts at a strike price of $510.

The option on the option chain shows a theta of -0.14 on a per-share basis for this option if we buy it.

Because we are selling it, we flip the sign.

This option gives us a positive theta of $14 per contract.

Since we are selling two contracts, we are gaining $28 per day.

But we lose $14 per day for the 503 put option.

And we lose $13 per day for the 516 put option.

In aggregate, the butterfly gains about $1 per day from positive theta:

$28 – $14 – $13 = $1

This is why the software is showing us a theta of 1.13 for the overall butterfly.

This number calculated by the software may vary slightly depending on the platform and software used.

If we double the contracts of this butterfly, such as:

Buy two May 10 SPY 503 put

Sell four May 10 SPY 510 put

Buy two May 10 SPY 516 put

We would get double the theta, getting about $2 per day.

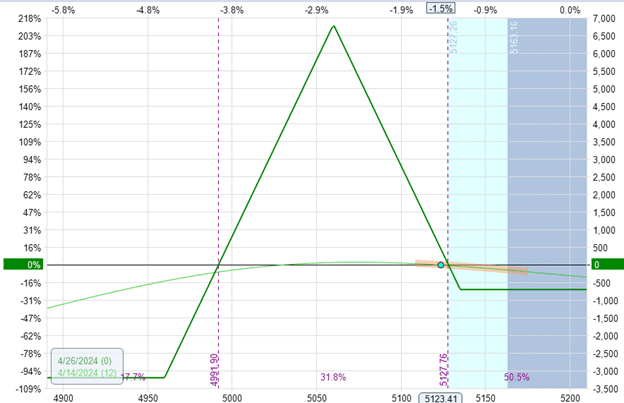

Another Example:

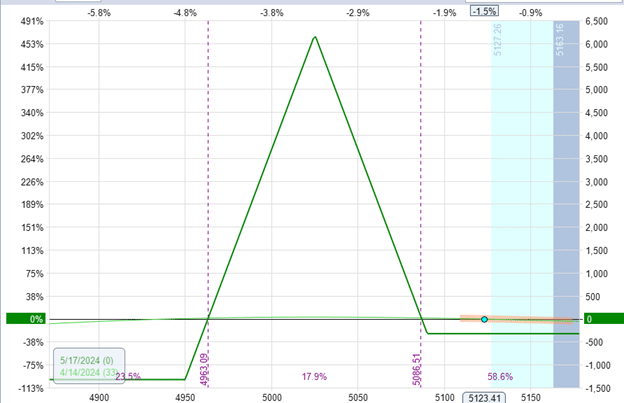

Here is a butterfly on SPX.

This is the larger S&P 500 index (not ETF).

Date: April 12, 2024

Price: SPX @ $5123.40

Buy one May 17 PM SPX 5050 put

Sell two May 17 PM SPX 5125 put

Buy one May 17 PM SPX 5190 put

It has a 65-point upper wing width and a 75-point lower wing width – also centered around the current price.

Because of its larger underlying asset price, it has a theta of 9.

The SPX fly gives nearly ten times as much theta per fly as the SPY fly.

This makes sense since the SPX index is about ten times as large as the SPY ETF.

The theta in this SPX fly is a little less than expected because this fly has an expiration date that is one week farther away than the SPY fly.

Because this fly has more time till expiry, its extrinsic value does not need to decrease as fast.

Hence, less theta.

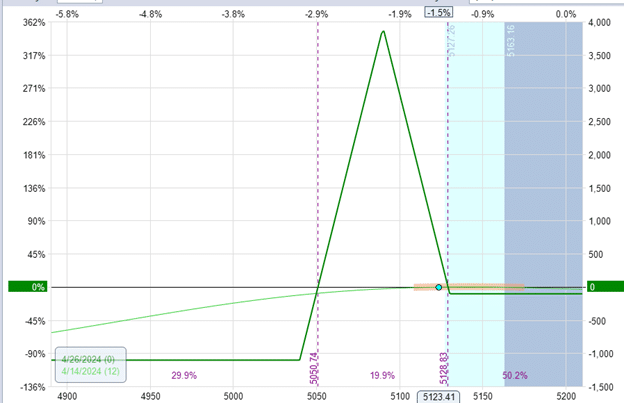

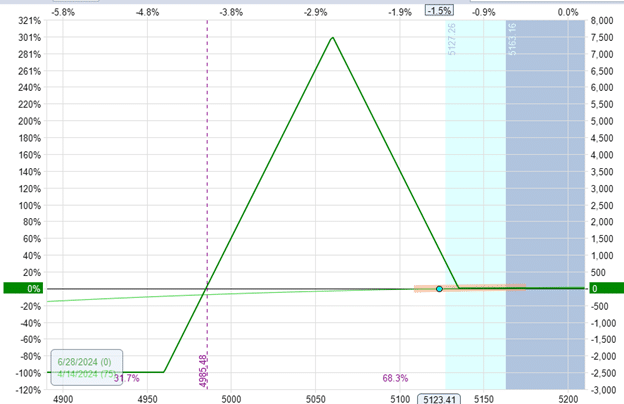

Out Of The Money Butterflies

If we were to shift this fly further away from price (but keeping the wing width and the expiration date the same):

Buy one May 17 PM SPX 5050 put

Sell two May 17 PM SPX 5125 put

Buy one May 17 PM SPX 5190 put

We would get less theta at $7.8 per day.

The at-the-money strikes have the highest extrinsic value.

Since we no longer sell the at-the-money strikes like before, we don’t get as much theta.

Shorter DTE

Shorter duration flies with less time to expiration typically have higher theta.

This fly with a 40-point upper wing and 50-point lower wing on the SPX has $18 of theta per day because it has only 14 days till expiration.

If we widen its upper wing to 75 points wide and its lower wing to 100 points wide:

We get even more theta at $53 per day.

Moving the fly further out in time with 75 days till expiration decreases the theta to $3.5 per day:

The Answer

What appears to be a simple question turns out to have a complex answer.

This starkly contrasts Douglas Adams’ science fiction novel “The Hitchhiker’s Guide to the Galaxy,” where a complex question is asked, and a simple answer is given in return.

A group of hyper-intelligent beings asked the supercomputer deep thought about the answer to the ultimate question of life, the universe, and everything.

Eventually, the computer gave the simple answer of “42”.

We hope you enjoyed this article on how much theta is in a butterfly.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.