Today, we are looking at the difference between a ratio spread and a backspread.

Ratio spreads, and backspreads are options strategies that involve buying and selling options with different numbers of contracts.

Let’s start with the ratio spread.

Contents

Ratio Spread

Consider the ratio spread as a credit collection strategy similar to selling put options.

However, the ratio spread has a long option in front of it.

Hence, it is also known as a “front-spread”.

However, that term is becoming out of favor.

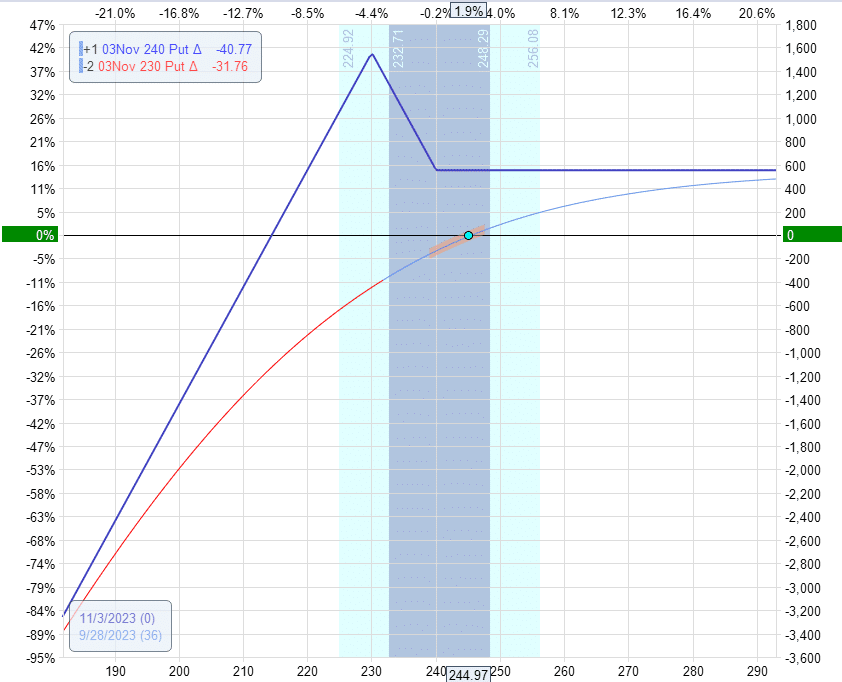

Below, we are selling a ratio spread on Tesla (TSLA).

Date: September 28, 2023

Price: TSLA @ $245

Buy one Nov 3 TSLA $240 put @ $13.52

Sell two Nov 3 TSLA $230 put @ $9.52

Credit: $552

We are selling two puts at the strike of $230 and buying one put option in front of it at the strike of $240.

“In front” means “closer to the current price of the underlying, which TSLA is at $245 now.

The net credit received of $552 is arrived by:

2 x $952 – $1352 = $552.

The payoff graph looks like this:

Unlike other credit collection strategies where the max profit is the credit received, the ratio spread differs slightly.

On the upside, the expiration graph shows a profit of $552 at expiration if the TSLA price is above $240.

In this sense, the profit is the credit received.

However, there is a peak in the graph when TSLA is at $230, where it can make up to $1552 at expiration.

To compute this max profit exactly, you can imagine what would happen if TSLA is at $230 at expiration.

The two short puts will expire worthless, and the long put is in the money by $10.

This long put option gives us a profit of $1000.

Now add to that the initial credit received of $552.

You have a maximum potential profit of $1552.

In a ratio spread, it is sometimes possible to enter the trade for a credit and exit it for another credit.

This is the nice thing about ratio spreads.

The not-so-nice thing about ratio spreads is that it has undefined risk on the downside – similar to that of a short put.

The ratio spread does have one extra naked short put.

If one does not manage the spread correctly, it is possible to lose a significant amount of money if TSLA drops by a lot.

This is also why the ratio spread requires a higher margin than other defined-risk strategies (such as the broken-wing butterfly).

It is worth noting that the ratio spread can be made into a broken-wing butterfly simply by adding another long put option at, say, the $205 strike.

In our example, we built the ratio spread using put options.

We say that is a “put ratio spread.”

Call Ratio Spread

A ratio spread can be constructed with call options as well.

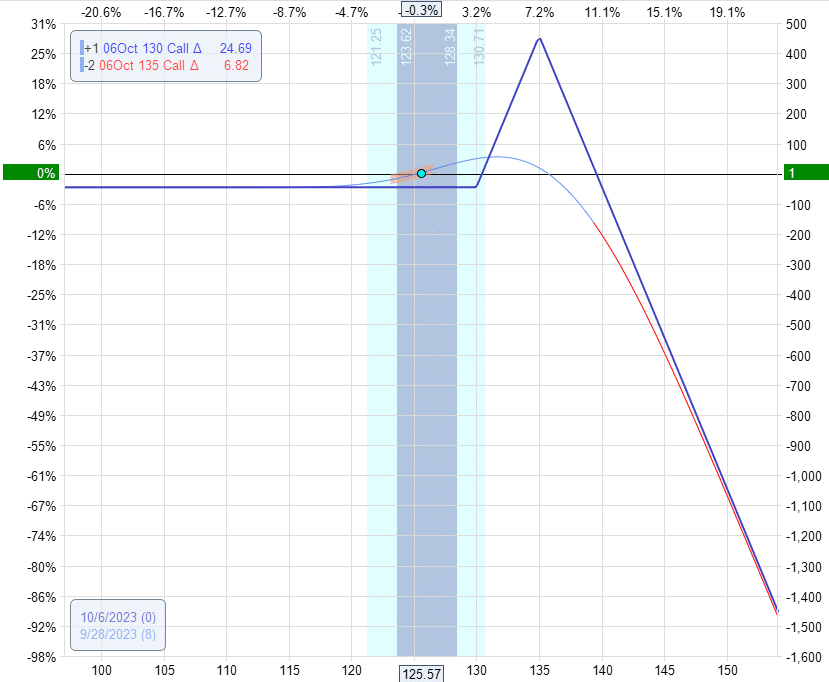

Here, we have a “call ratio spread” on Amazon (AMZN) with shorter days till expiration.

Date: September 28, 2023

Price: AMZN at $126

Buy one October 6 AMZN $130 call @ $0.81

Sell two October 6 AMZN $135 call @ $0.18

Because -$81 + $18 + $18 = -$45

We pay a net debit of -$45 to initiate this ratio spread.

It looks like this:

This ratio spread is no longer a credit collection strategy.

Its theta is negative, unlike the positive theta we had in the TSLA example.

This call ratio spread is constructed as a directional strategy where we want the price of AMZN to go up toward the peak of the expiration graph where the two short calls are located.

Look at the curved T+0 line.

If the price goes up, we can exit the trade with a credit larger than the initial debit paid. And that is the goal.

We don’t want the price to overshoot the peak, resulting in a big loss in the negative profit territory.

As the price increases, it must pass through the positive profit territory before reaching the negative profit territory.

Some traders will monitor the price carefully to exit before getting into a loss situation unless the stock happens to gap up overnight past the peak.

Think of this call ratio spread as a directional call but with one long call at a strike of $130 being financed by two further out-of-the-money short calls at a strike of $135.

If we had just purchased a long $130 call to bet that the price of AMZN would have gone up, that option would have cost us $81.

But here, we only paid $45 because we had collected $18 each for the short calls sold.

Backspreads

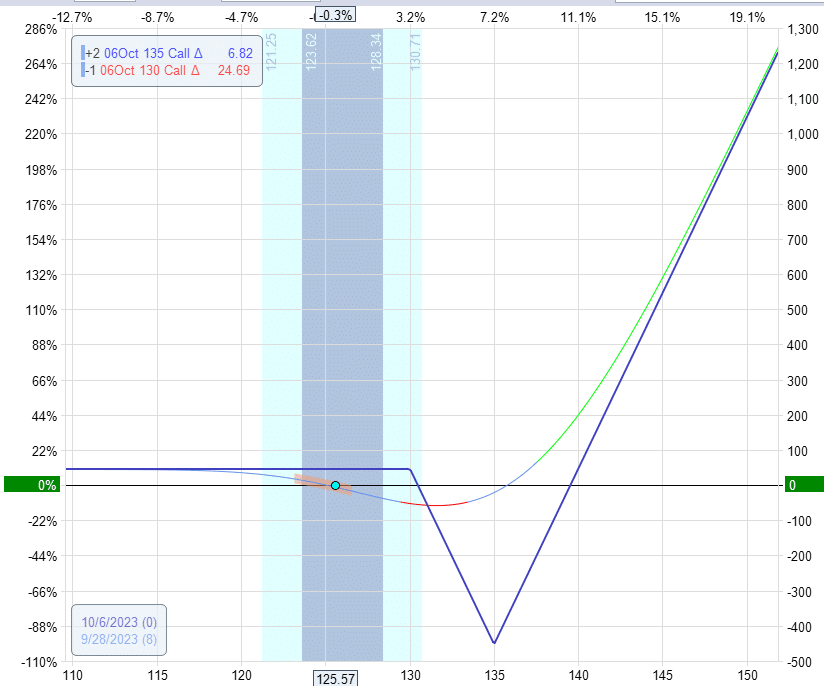

If we take the last example and buy instead of sell, and sell instead of buy, we would have a backspread.

Date: September 28, 2023

Price: AMZN at $126

Sell one October 6 AMZN $130 call @ $0.81

Buy two October 6 AMZN $135 call @ $0.18

Credit: $45

And we get an expiration graph that is the mirror image:

The undefined-risk ratio spread became the defined-risk backspread.

Put Backspread

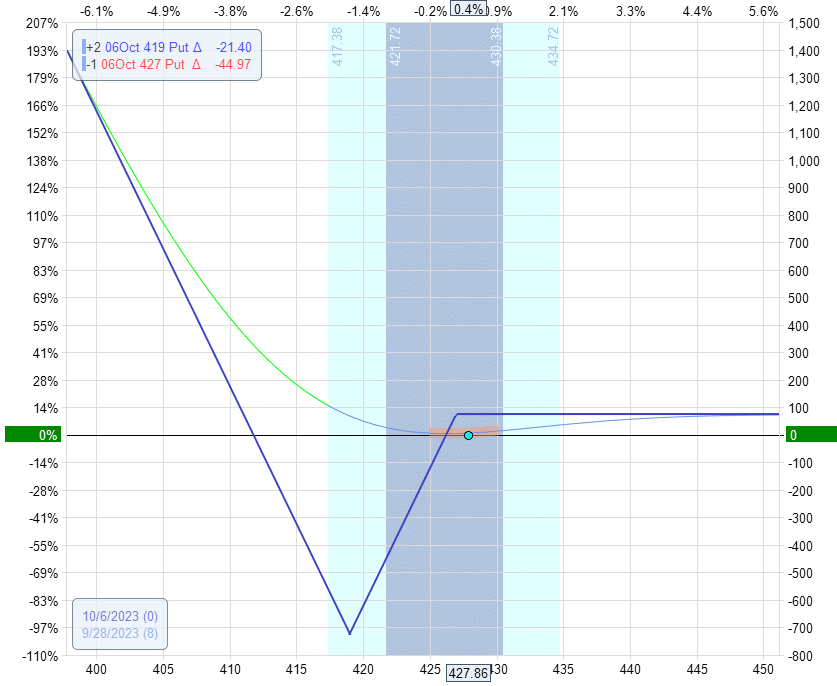

The next example shows a backspread using all put options on SPY:

Date: September 28, 2023

Price: SPY @ $428

Sell one October 6 SPY $427 put @ $3.57

Buy two October 6 SPY $419 put @ $1.41

Net credit: $75

Because $357 – $141 – $141 = $75

This construction aims to profit from a large, quick price move by the S&P 500 in either direction.

See the T+0 line curves up in either direction.

Even though we get a credit at the start of the trade, time decay is working against us.

We have negative theta.

So we want to get out of this trade fast.

The last thing we want is to sit till expiration, and the price of SPY ends at $419, where we lose $725.

When that happens, the short put is in the money by $8 (because $427 – $419) and we lose $800.

Partially compensated by the $75 credit, the max loss on this trade is $725.

While this is a defined-risk trade, losing $725 is still not fun.

Since we are used to collecting credit and getting positive in iron condors.

It may seem strange that we collect a credit but still have negative theta.

The dip in the expiration graph at $419 causes the T+0 line to drop as time passes.

Conclusion

This article has a lot to unpack, and ratio and backspreads are indeed confusing.

They can be constructed with calls and with puts.

Sometimes, you get a credit at the start of the trade, and sometimes you get a debit.

Sometimes, if you are lucky (or skillful), you get a credit at the start of the trade and get another credit when you close the trade.

We hope you enjoyed this article on the difference between a ratio spread and a backspread.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.