If you want to build wealth, dividend stocks can be a great way to do it.

These stocks pay you a portion of their earnings, providing a potential income stream.

You can receive cash or additional shares, depending on the type of dividends or if you choose to reinvest it.

Some of these are even taxed at a lower rate.

You also have options like Dividend Reinvestment Plans (DRIPs) to maximize growth.

Plus, investing in a diversified portfolio can help offset some potential risks.

By exploring different strategies, you can tailor your approach for ideal results.

Contents

What Are Dividend Paying Stocks

Understanding what dividend-paying stocks are can greatly enhance your investment strategy.

These stocks represent shares in companies that regularly distribute a portion of their earnings to shareholders, typically in the form of cash but occasionally in other methods like additional shares or physical bullion.

By investing in these stocks, you’re hoping for price appreciation and dividend appreciation to create an income stream.

You’ll often find dividend-paying stocks categorized into common and preferred stocks.

Preferred stocks generally offer higher and more stable dividend payments, making them attractive if you prioritize consistent income.

The trade-off with preferred is that they can be more illiquid and don’t often have the price appreciation of common.

Dividend stocks have a metric called yield, which is represented by percentages.

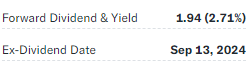

You can expect to earn this percentage of the share price back in cash payments throughout the year. Let’s take Coca-Cola (KO), for example.

They have a yield of 2.71%, and their share price is $71.64 at the time of this writing.

You can earn back roughly $1.94/year per share.

You don’t need to calculate this for each stock; the image above is from Yahoo Finance, and they have it for every ticker that pays a dividend.

The other piece of important information is the Ex-Dividend date.

This is the date you need to hold the shares to be considered for the dividend.

Finally, there are several classifications of dividend-paying stocks.

Companies that consistently increase dividends over time gain recognition in the form of a category classification.

Companies that have increased their dividend every year for the last 25 years get the title of Dividend Aristocrats, and companies that have increased their dividends for each of the last 50 years are known as Dividend Kings.

These designations highlight the reliability and strength of a company’s financial health.

What Are The Different Types Of Dividends?

Now that you have the background on dividend-paying equity let’s look at some of the different categories of these equities.

Outside of the regular equities, there are also Real Estate Investment Trusts (REITS) and Master Limited Partnerships (MLPs).

While they all trade similarly on the open market, several distinctions in terms of structure and taxes make them slightly different.

Regular dividend-paying equities represent common stocks of companies that share profits with shareholders through dividends.

These corporations are subject to corporate taxes, and shareholders also pay taxes on dividends.

Examples of these would stocks like Coca-Cola above or Apple.

Generally, dividend yields for these stocks range between 2% and 4%, and they are available across various sectors of the economy.

Real Estate Investment Trusts (REITs) focus on income-producing real estate properties.

By law, they must distribute the majority of their income, at least 90%, allowing them to bypass corporate-level taxation.

Shareholders, however, are taxed on these dividends, typically as ordinary income.

REITs often offer higher yields than regular stocks but, as the name suggests, are limited to Real Estate.

These can be a great way to get exposure to Real Estate income without putting up the large upfront capital.

Master Limited Partnerships (MLPs) are the last subsection of dividend stocks we will look at.

There are publicly traded partnerships and are usually found in the energy sector.

These pass-through entities avoid corporate taxes and distribute income directly to investors responsible for paying taxes on their portion.

MLPs typically offer the highest dividend yields of the three, often between 8% and 10%, but they also tend to have more complex tax reporting due to the issuance of K-1 forms.

Their focus on energy and natural resources can also make them more volatile compared to REITs and regular equities as well.

Key differences between these vehicles include income distribution rules, tax reporting requirements, and risk profiles.

Each can offer a potential stream of passive income, but they all require a different amount of due diligence and tax knowledge.

DRIP: The Ultimate Reinvestment Plan

If you have been investing for any length of time, you have probably heard about a DRIP program.

Dividend Reinvestment Plans (DRIPs) are a powerful tool for investors looking to automate and increase their returns.

By automatically reinvesting your dividends into additional shares of the same stock, you can harness the power of compounding without worrying about remembering to invest your dividends.

For example, an investment in an S&P 500 index fund from 2000 to 2020 yielded an annualized return of 4.2% without reinvestment, which jumped to 6.2% when dividends were reinvested.

The large benefit of the DRIP program is that it allows you, as the investor, to take advantage of dollar cost averaging without having to think about or worry about market conditions.

Enrolling in a DRIP program used to require a sign-up through the company itself or a third-party custodian like Compushare but given the rise of discount brokers and the rapid increase in trading technology, most brokers have a place where you can opt-in to have all distributions and dividends reinvested.

How Are Dividends Taxed?

Dividends are taxed differently depending on whether they are qualified or non-qualified.

Based on the investor’s income bracket, qualified dividends are taxed at lower long-term capital gains rates, ranging from 0% to 20%.

To be counted as a qualified dividend, distributions must come from a US corporation or a qualified foreign company, and the investor must hold the stock for at least 61 days around the ex-dividend date.

The official rule reads as follows: “…must have held the security for at least 61 days out of the 121-day period that began 60 days before the security’s ex-dividend date”.

This is and should be a non-issue if you are treating this like a long-term investment.

In contrast, non-qualified dividends do not meet the criteria for lower tax rates and are taxed as ordinary income, which can range from 10% to 37% in the US at the time of this writing.

Non-qualified dividends can occur if the stock is held for less than 61 days within the specified period or through certain investments like REITs and MLPs.

This higher tax classification can significantly impact investors in higher tax brackets, making it important to understand how these dividends affect overall tax liabilities.

The best way to do this is to talk to your tax professional.

Knowing the difference between qualified and non-qualified dividends is critical for effective tax planning and wealth accumulation.

Qualified dividends offer better after-tax returns, while non-qualified dividends can increase your tax burden.

Should You Invest In A Single Stock Or Portfolio For Dividends?

Investing in dividend stocks can frequently make you choose between a single stock and a diversified portfolio.

While a single dividend stock might lure you in with the promise of high yields, it can also expose you to company-specific risks that could jeopardize your entire invested amount.

Relying solely on one company ties your investment success to whether they succeed in the long run.

On the other hand, a diversified portfolio helps mitigate company-specific risks by spreading your investments across various companies and sectors.

This strategy stabilizes your investment account from a risk perspective and helps offset payment days, creating better cash flow for the portfolio.

Combining dividends from multiple sources creates a buffer against unexpected cuts from any single stock.

This creates several advantages for you.

First, there is more peace of mind that even if one company goes south, the remainder of your account will still be produced.

Second, as discussed above, multiple companies can help to spread cash flow across multiple days each quarter.

Lastly is the growth potential; the more companies you can meaningfully invest in, the higher the odds you will select one that breaks out.

Given all these factors, diversifying your portfolio whenever possible would make more sense.

It is fine to start investing in a single stock, but diversification should be a priority as soon as you have the capital.

Do Index Funds Beat Custom Portfolios For Returns?

One of the easiest ways to diversify your portfolio is to invest in an index fund like the SPY or one of Vanguard’s low-cost ETFs like VTI.

This exposes you to the entire market without worrying about how spread out your risk is.

Another reason index funds can be a better solution is that research shows that over 80% of actively managed portfolios fail to outperform their benchmark indices in the long run.

For instance, a study by S&P Dow Jones Indices revealed that 92% of large-cap active funds underperformed the S&P 500 over a 15-year period, which underscores the challenges of custom portfolio management.

This also does not consider that these actively managed funds typically have higher fees, which can further undercut performance.

One notable exception here would be using a specific type of ETF that can help offset drawdowns in the overall market.

One example would be covered call or wheel strategy funds such as JEPI or WEEL.

These funds use options premiums to help offset sideways and downward action in the market.

They still have the same tendency to underperform the overall market, given they have a capped upside.

Still, the additional premium on the downside can be a nice addition to your income.

So, where does this leave you as an investor?

Overall, it would probably make the most sense to invest a dividend portfolio directly into an Index fund unless you have a specific need or type of portfolio you want to maintain.

Statistics say that this is the best way to achieve market returns, and it helps keep fees to a minimum.

Conclusion

Dividend-paying stocks offer a flexible way to build wealth through income and capital appreciation.

By choosing between common stock, REITs, and MLPs, investors can tailor their portfolios based on income goals and risk tolerance.

Understanding the tax differences and utilizing tools like Dividend Reinvestment Plans (DRIPs) allows investors to compound their returns for long-term growth.

Diversifying investments across multiple stocks or index funds helps mitigate risk while maintaining a steady income stream.

Single stocks may offer higher yields but expose investors to company-specific risks, making a diversified portfolio a safer option.

Whether you choose individual stocks or broader funds, a well-planned dividend strategy can provide consistent returns and support long-term cash flow, especially with attention to tax considerations and dividend reinvestment.

We hope you enjoyed this article on Dividend Stocks.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.