Today, we are looking at covered call exit strategies. We will cover when to let them expire, when to be assigned and rolling out. Enjoy!

Contents

- Let The Call Expire

- Let The Call Be Assigned

- Close Out The Call And Retain The Stock

- Unwind The Entire Position

- Rollout

- Rolling Out And Up

- Rolling Out And Down

- Closing Early To Avoid Earnings Volatility

- FAQ

- In Summary

As covered call investors, we generally want the stocks on which we are trading covered calls to be neutral to slightly higher when expiration date approaches.

If the stock rises too much, we have foregone potential profit by selling the call, and if the stock falls too far we are left with an unrealized loss on our stock position.

In a perfect world, the stock would finish up just below our call strike on expiration day. Unfortunately, the world is not perfect, particularly when it comes to financial markets.

In most cases, investors will need to take some sort of action on or around the expiration date and sometimes even earlier than that.

Managing the exit side of a covered call is far harder than the entry side and should be decided in advance of entering the trade.

This should all be written down as part of your trading plan.

There are generally considered to be seven different actions you can take with regards to exiting a covered call trade:

- Let the call expire

- Let the call be assigned and have the stock be called away

- Close out the call and retain the stock

- Unwind the entire position by selling the stock and simultaneously buying back the call

- Rollout the call to the next month at the same strike price

- Rollout to the next month and move the strike up

- Rollout to the next month and move the strike down

Let’s look at each of these scenarios in detail.

Let The Call Expire

As expiration approaches, if the stock has remained flat or declined slightly, investors can simply let the calls expire worthless.

The premium they received for selling the call is theirs to keep and the obligation they had from selling the call (to deliver shares at the strike price if called upon to do so) is removed from their account.

This of course assumes that the stock has not declined below your stop loss level.

If you had a stop loss of 8% and the stock is down 8% as expiry approaches, you may be better off to unwind the entire position.

When the stock has not reached your stop loss level and you are still neutral to slightly bullish, then you can sell another call option if you so desire.

If the investors outlook has changed to strongly bullish, then they may choose to simply continue to hold the stock without selling calls with the aim of achieving higher capital returns.

Occasionally, when expiration draws nearer, the stock can be trading right around the strike price.

In this case, it is difficult to know if the stock will finish in-the-money or out-of-the-money.

Remember that even if the call expires in-the-money by as little as $0.01, it will be automatically assigned.

In the scenario where the stock is trading right around the strike price, one of the other six actions may be more appropriate than hoping the call will finish out-of-the-money.

Example

Suppose an investor has the following covered call on Home Depot (HD):

Date: Jan 21, 2022

Buy 100 shares HD @ $356.01

Sell one Feb 18 HD $370 call @ $5.23

The investor plans to hold to expiration.

On expiration on February 18, Home Depot closed at $346.87 which is lower than the strike price of $370.

Hence the call expires worthless and the investor keeps the $523 credit from the sale of the call.

However, 100 shares lost $914 in value. So the combined covered call position is at a loss of $391.

Let The Call Be Assigned

At expiry, if the call option is in-the-money by as little as $0.01, the buyer of the call will exercise their right to purchase the shares at the strike price and your shares will be called away.

Generally speaking, this is a good thing. Assuming you have sold at-the-money, or slightly out-of-the money calls, you will be in a position of profit.

In fact, with covered calls, this is the maximum profit that can be achieved.

When you are assigned, both the stock and call option will be removed from your account.

The net credit will be deposited into your account which will be equal to the number of shares x the strike price.

Remember that you also still keep the option premium that you initially received when selling the call.

Sometimes option assignments will occur prior to expiration.

This is most common on dividend paying stocks, although it can happen on any stock. Usually early assignment occurs on the day before the stock goes ex-dividend.

The call buyer exercises their option early in order to take ownership of the stock on ex-dividend day and therefore receive the dividend.

This commonly occurs when the call option is in-the-money and the dividend amount exceeds the remaining time premium on the option.

In this case, the call buyer is better off to exercise their option and receive the dividend rather than waiting for the time premium to decay (which is less than the dividend in any case).

When the call buyer exercises their option early, any remaining time value is lost.

Traders that plan to sell covered calls on dividend paying stocks should be aware of how early assignment works, why it would occur and they should also keep a close eye on the ex-dividend dates.

Example

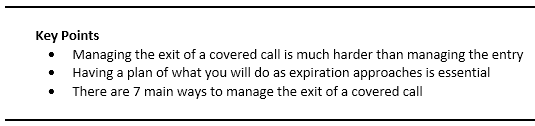

Suppose an investor has the following covered call on Goldman Sachs (GS):

Date: March 1, 2022

Buy 100 shares GS @ $328.65

Sell one Mar 18 GS $345 call @ $5.20

source: OptionNet Explorer

This investor plans to hold to expiration and is willing to let the call be assigned and to give up the Goldman Sachs stock if it gets up to $345.

On expiration March 18, Goldman Sachs closed at $345.38, just $0.38 above the short strike of $345.

Hence, the broker automatically sells 100 shares of GS at $345.

The investor is happy with the sales since the net profit is $2155 from the calculations below.

Buy 100 shares: –$32865 Sell covered call: $520 Sell 100 shares: $34500 Total: $2155

Close Out The Call And Retain The Stock

Investors who have a covered call position that is in-the-money near expiry, but want to retain ownership of the stock, should close out the call option prior to expiry.

To do this, the investor makes the opposite trade to when they opened the covered call.

The opening trade would have involved selling the call option, so the investor simply places a buy to close order.

That information probably seems basic to you, but you would be surprised how many times I get asked this question.

After buying back the call, the investor has removed the obligation to deliver the shares at the strike price and can continue to hold the shares.

Investors might close out the call option and retain the stock if they want to continue to receive the dividends from the stock and / or continue to participate in any future capital gains.

Choosing to retain the stock, generally implies that the investor is still bullish on the stocks prospects.

Example

Suppose an investor has a covered call on Microsoft (MSFT):

Date: February 23, 2022

Buy 100 shares MSFT @ $287.19

Sell one March 18 MSFT $295 call @ $5.90

On the morning of expiration day of March 18, the investor checks the price of Microsoft two hours after the open and sees that its price is at $297.64, which is slightly above the strike price of $295.

Wanting to continue to own the Microsoft shares and is still bullish on Microsoft, the investor decides to close the short call to avoid the risk of MSFT being called away at the end of the day.

Date: March 18, 2022

Buy to close March 18 MSFT $295 call @ $2.94

At the end of the day on March 18, Microsoft closed at $300.43.

The running profit and loss (P&L) so far is.

Buy 100 shares: –$28,719 Sell covered call: $590

Buy to close call: –$294 Value of 100 share: $30,043

Current profit: $1620

The investor made $296 from the sale of the call and still owns the 100 shares which had already appreciated $1324.

Unwind The Entire Position

Unwinding both parts of a covered call position (long stock and short call), can be a prudent choice if the stock has experience a large gain early on in the trade.

In this case, unwinding the trade will lock in the gain, although this will be less than the maximum potential gain if the position was held to expiry.

Sometimes it is best to lock in a gain rather than see the position fall back down and potentially become a losing position.

Call options have a delta, which can provide a guide as to how much the option price will change compared to the change in the stock price.

For example, if an investor buys a stock at $25 and sells a $25 call, the call option will have a delta of 0.50 meaning it will increase 50c for every $1 move in the stock.

Assuming the call option was sold for $2 and after 3 days, the stock has increased to $26, the call option will now be worth approximately $2.50.

This is a very simplified calculation and in reality there are a few other factors that will affect the option price such as implied volatility, time decay and gamma.

In the above example, the investor will be sitting on a gain of 50c.

A $1 gain from the stock price increase and a 50c loss from the call option increase (remember we sold the call).

The total potential profit on the trade is $2 and the investor has made 50c or 25% of the potential profit after 3 days.

In this case, the investor may be tempted to unwind the position and book a profit rather than wait until expiry to hopefully receive the other $1.50 in profit.

A Good Rule Of Thumb

There is a good rule of thumb that can be followed when considering unwinding a covered call early:

If this formula results in a number greater than one, it can make sense to unwind the trade.

Taking the example above, if this was a 30-day trade, the formula would be:

0.25 / 0.10 = 2.5

As this is greater than 1, it makes sense to unwind the trade.

25 percent of the profit has been made in 10 percent of the trade duration.

The investor would have to wait through 90% of the remaining trade time to achieve the remaining 75% profit potential.

There is also the potential that the stock could fall back down and the investor could give back some of the profit.

This is just a rule of thumb and its really personal preference, but it is something that should be detailed in a trading plan.

For example, an investor may choose to modify the rule slightly and say that they will unwind the position if the above formula is greater than 1 AND the profit is greater than 50% of the potential profit.

Example

Suppose an investor sells a covered call on Apple (AAPL) with 22 days to expiration:

Date: February 24, 2022

Buy 100 shares of AAPL at $157.96

Sell one March 18 AAPL $165 call @ $2.49

The max profit on this trade would be:

($165 – $157.96) x 100 + $249 = $953

On March 2nd, not even half-way through the duration, the investor sees that the profit is already at $583, which is more than 50% of the max potential profit.

The investor decides to take the profit by closing out the obligation of the short call first. And then selling the shares.

Date: March 2, 2022

Buy to close March 18 AAPL $165 call @ $5.03

Sell 100 shares of AAPL @ $166.33

The transaction can be performed simultaneously. However, don’t sell the shares before closing the call. Otherwise you will have an uncovered naked short position.

The net profit from this covered call is…

Buy 100 shares: –$15,796 Sell covered call: $2.49 Buy to close call: –$5.03 Sell 100 shares: $166.33

Net profit: $583

It is true that the investor lost money on the call option. But the appreciation in the price of the stock far out-paced this loss.

Rollout

Rolling out refers to the process of closing the short call and selling a new call with the same strike in a subsequent month at the same strike price.

Investors would look to do this if the stock is close to the strike price as expiration approaches and they believe the downside is minimal. i.e. they continue to maintain a neutral to slightly bullish outlook.

If the investor wants to maintain exposure to the stock but is concerned they might be assigned, then a rollout is a good idea.

The process of rolling out will almost always result in a net credit if the options are at-the-money or close to it.

For example, the near month option which is being bought to close might be trading at $1 and the next month option which is being sold to open might be trading at $2.

By closing the near month and opening the later month, the trader receives a net credit of $1 while still maintaining the same covered call exposure.

The difference in option premiums may be much less for deep in-the-money or out-of-the-money calls due to the low time premium component.

Rolling out these types of positions may not make sense given the small additional premium received.

As such, rolling out covered calls tends to make the most sense near expiry, when the stock is close to the strike price.

Example

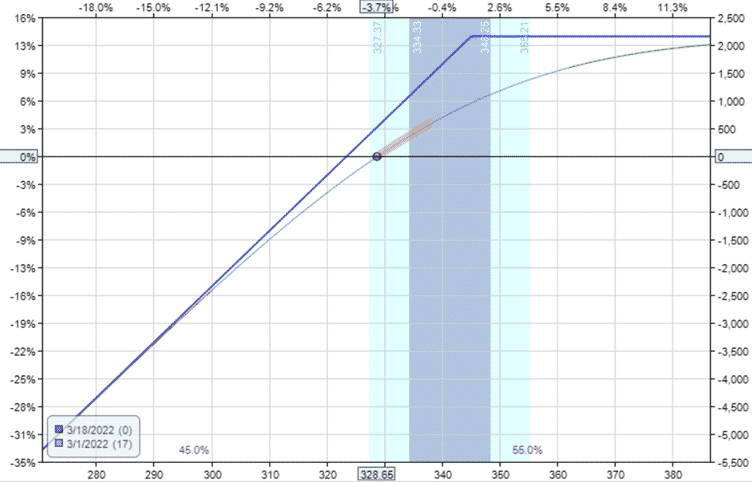

Consider the following covered call on General Mills (GIS):

Date: January 3, 2022

Buy 100 shares of GIS @ $66.13

Sell one Feb 18 GIS $67.5 call @ $0.85

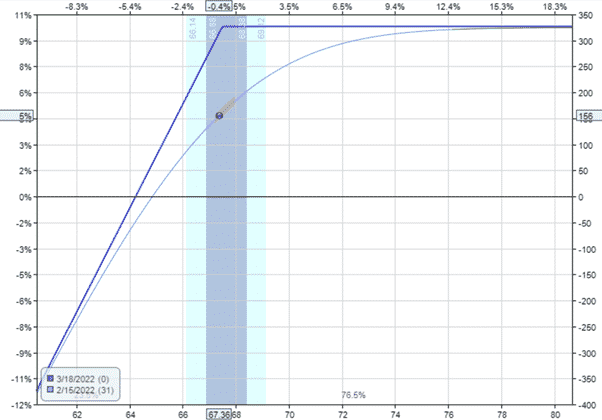

A few days before expiration on February 15, General Mills is at $67.36 quite close to the short strike.

The investor rolls the call further out in time keeping the same strike for a credit of $105.

Date: Feb 15, 2022

Buy to close one Feb 18 GIS $67.5 call @ $0.53

Sell to open one Mar 18 GIS $67.5 call @ $1.58

The new payoff diagram afterwards shows the increase in profit potential:

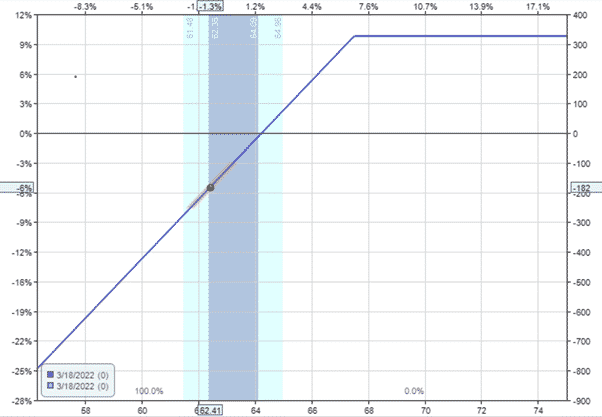

Unfortunately, there was a subsequent decline in the share price.

On March 18 expiration, General Mills closed at $62.41 which is lower than what it had started at $66.13.

The short call expired out-of-the-money and the investor still owns the shares.

The running P&L so far is a loss of $182…

Buy shares: –$6613 Sell covered call: $85 Roll call: $105 Value to GIS: $6241

Running P&L: –$182

An investor who only owned the 100 shares for the same duration would have lost $372.

Rolling Out And Up

Another possibility when expiration is approaching and the stock is close to the strike price is to roll out and up.

Usually an investor would only do this if they are bullish on the stock.

In order to roll up, the investor would close the current month call through buying it back and selling the future month higher strike calls.

Sometimes, investors may be able to roll out and up for a net credit, but this adjustment can also require a net debit.

For example, let’s assume that as the April expiry date approaches, the stock is trading at $24.50 and the $25 call is trading for $2.00.

An investor is bullish on the stock and wants to maintain exposure, but thinks the stock has the potential to rise to the $27-28 level.

The May $27.50 call is trading at $1.20.

If the investor rolls out 1 month and up to $27.50, the adjustment will result in a net debit of $0.80 because they are buying back the $25 call for $2 and selling the $27.50 call for $1.20.

However, there is an extra profit potential in the trade, given that the stock will not be assigned until $27.50, so there is an additional potential capital appreciation component of $2.50.

As this adjustment example costs money to implement, investors would generally only consider this method when they are bullish.

Example

Consider the following covered call position:

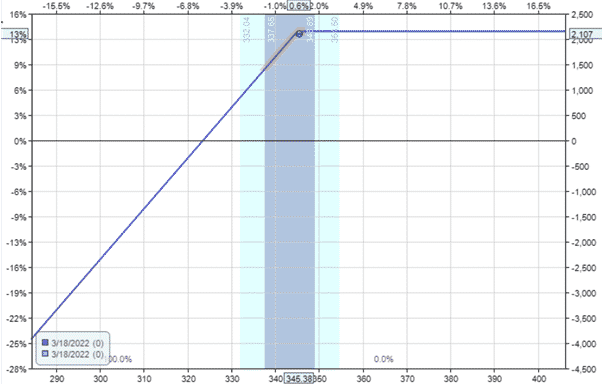

Date: Feb 23, 2022

Buy 100 shares of MRK @ $75.93

Sell one Mar 18 MRK $78 call @ $0.80

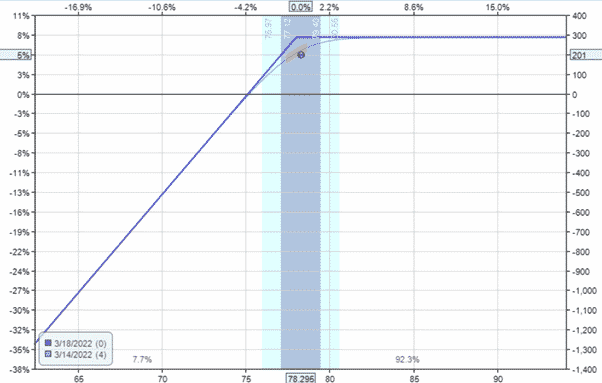

On Monday of expiration week, Merck’s price reached the short strike of $78.

The payoff diagram shows price close to the strike price:

The investor believes that MRK can go much higher and decides to continue the covered call for at least another month.

Hence the investor rolls the short call out in time and up and strike.

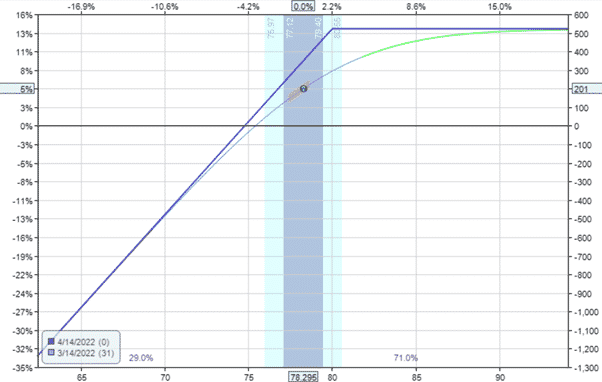

Date: Mar 14, 2022

Buy to close Mar 18 MRK $78 call @ $1.16

Sell to open Apr 14 MRK $80 call @ $1.51

The investor receives a net credit for $35 for the roll adjustment.

Plus, the new payoff diagram shows there is now more room for the stock to go up.

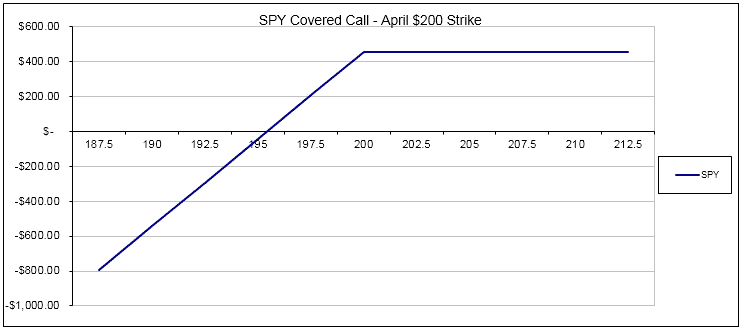

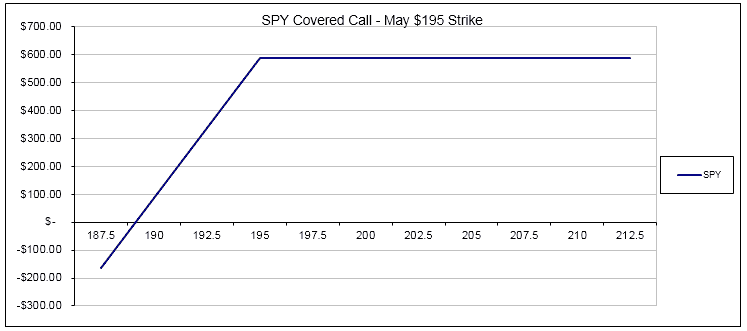

Rolling Out And Down

A roll out and down might be considered as a way to lock in some profits on a stock that has risen above the strike price.

Looking at SPY which is currently trading at 203.22. Assume a trader has sold an April covered call using the $200 strike.

The call is now in-the-money to the tune of $3.22 and has a time premium component of $1.35 for a total premium of $4.57.

By rolling out to May and down to $195, you generate $5.87 in premium and give up $5 of intrinsic value.

In other words, you gain an extra $87 by waiting another month and are protected down to $195 rather than only $200.

Example

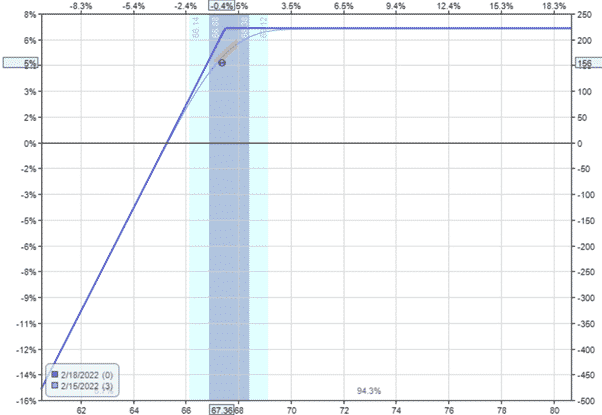

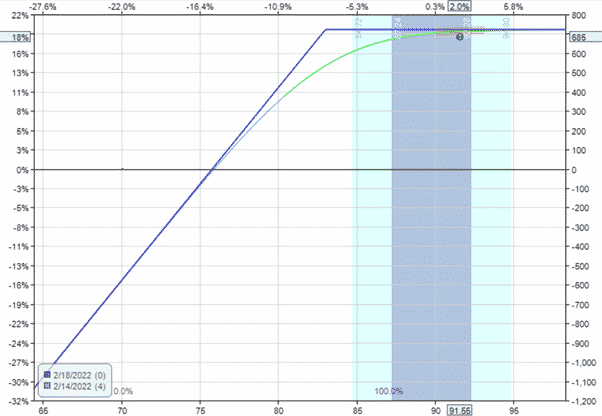

Suppose an investor has a covered call position in Micron (MU):

Date: Jan 23, 2022

Buy 100 shares of MU @ $77.36

Sell one Feb 18 MU $83 call @ $1.58

Four days before expiration on February 14th, Micron price at $91.55 has already surpassed the strike price of $83.

The payoff diagram shows that we are close to max profit near the top of the profit curve.

Since there is not much profit left in the trade, this would be a good time to exit and close the trade out.

But instead, the investor decides to roll the short call out in time and down in strike.

Date: Feb 14, 2022

Price: MU @ $91.55

Buy to close one Feb 18 MU $83 call @ $8.93

Sell to open one Mar 18 MU $77.5 call @ $15.30

Credit: $637.50

This may seem counter-intuitive

Think of it this way. It is similar to closing out the existing trade.

The investor buys to close the call. But instead of selling the stock right away, the investor sells an in-the-money call to get rid of the stock.

The investor sells the $77.5 call with assumption that the stock will stay above $77.5 and be called away in one month’s time.

Buy delaying the sale of the stock by one month, the investor picks up addition extrinsic value that is in the $77.5 call.

At the time of the sale, the call has an intrinsic value of $14.05 (take $91.55 minus $77.50). It has $1.25 of extrinsic value (take $15.30 minus $14.05).

If the investor holds the call to expiration (which is the intent) and if the stock price stays above $77.50, the investor will capture this extrinsic value.

And indeed on expiration on March 18, the price of MU closed at $79.41 and the 100 shares are automatically sold at $77.50 per share.

The total profit from this trade is…

Buy 100 shares: –$7736

Sell covered call: $158

Roll out and down the call: $637.50

Sell 100 shares: $7750

Total profits: $809.50

If the investor had closed out the entire trade on February 14, the profits would have been…

Buy 100 shares: –$7736

Sell covered call: $158

Buy to close call: –$893

Sell 100 shares: $9155

Total: $684

Still good, but less the $125 of extrinsic value captured in the sale of the second call.

This is under the assumption that the price stayed above the strike price of the second call.

If on February 14, the investor rolled to the $80 call (instead of the $77.50 call)…

Date: Feb 14, 2022

Price: MU @ $91.55

Buy to close one Feb 18 MU $83 call @ $8.93

Sell to open one Mar 18 MU $80 call @ $13.18

Credit: $425

Then on expiration March 18, MU would have closed below the strike price of $80.

The call would be gone. The investor still owns the stock, which the investor can still sell on Monday morning at $77.44.

Buy 100 shares: –$7736

Sell covered call: $158

Roll out and down the call: $425

Sell 100 shares: $7744

Total profits: $591

The profits would have been less, depending on how far down the price of Micron goes.

Closing Early To Avoid Earnings Volatility

One final reason for closing covered calls early, is to avoid volatility surrounding earnings announcements.

Depending on the stock, it is not uncommon to see a move of 5%, 10% even 20% after an earnings announcement.

A 20% gap down is a covered call writer’s nightmare.

The sold call does little to protect the downside move and a gap down of 20% would blow right through any stop loss.

Sometimes, it can be best to avoid these earnings announcements particularly if a big move is anticipated.

Investors should always check a company’s earnings date before entering a covered call trade.

It might be best to remove high volatility stocks from an investors covered call candidate list altogether, or if an investor does decide to go with these types of stocks, they need to understand the risks they are exposing themselves to.

FAQ

What Is A Covered Call Strategy?

A covered call strategy involves owning a stock or ETF and selling call options on that stock or ETF to generate income.

What Are Some Covered Call Exit Strategies?

Some covered call exit strategies include rolling up the call option, buying back the call option, letting the call option expire worthless, and selling the underlying stock.

When Should I Consider Using A Covered Call Exit Strategy?

You should consider using a covered call exit strategy when the call option is in the money, when the stock is showing signs of weakness, or when you have achieved your profit target.

How Do I Choose The Right Covered Call Exit Strategy?

Choosing the right covered call exit strategy depends on your goals and the market conditions.

It’s important to have a plan in place and to consider factors such as the time remaining on the option and the potential for further stock price movement.

What Are The Risks Of Using A Covered Call Strategy?

The main risk of using a covered call strategy is that if the stock price rises above the strike price of the call option, you may miss out on further gains.

Additionally, if the stock price falls significantly, the option premium may not fully offset the losses.

In Summary

- Covered calls can be a great way to gain additional income for a stock

- Entering a covered call is the easy part. Managing what happens next is the hard part.

- There are 7 main ways to exit a covered call trade

- Let them expire

- Let them be assigned

- Close the call and keep the stock

- Close the entire position

- Roll out

- Roll out and up

- Roll out and down

We hope you enjoyed this article on covered call exit strategies. If you have any questions, please send an email or leave a comment below.’

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Good explanation, as usual, Gavin.

Len

Thanks Len. Hope all is well with you.

Hi Gavin,

Thank you so much for this. I am a newbie and will read a few times over. I thoght I understood covered calls. I am perplexed. I wrote a covered call $220 strike. 11/5/21 on GME currently trading at $199 and am confused as to whether I will lose the stock or cash somehow if the stock falls dramatically. Market value of contract shows a negative amount but daily gains are positive. Am I losing or winning this trade?

If GME closes above 220 on the expiration date, the shares will automatically be sold for $220. If you are currently showing a loss on the short call, you most likely have a gain on the stock position which would offset that lost and then some. So, the combined position should be in profit, but it’s hard to tell based on the limited information you provided.

In the “Rolling Out and Down” example; how exactly do you come up with $5.87 premium figure? Also, where exactly does the $87 come from? Thank You!

Hi Brian,

When I wrote the article, the May $195 call was trading at $10.44. Buying back the $200 call for $4.57 and selling the new call for $10.44 gives us a net premium of $5.87 received.

We are giving up $5 of capital by lowering the strike price. So $5.87 less $5 = $0.87 or $87.

Hope that helps. Let me know if you still have questions.

thank you Gavin

appreciate your time and willingness to share your experience and time.

your posting could not have been more timely,after reading it,went to my open positions and closed 2 expiring this week,was able to minimize loss and secure small profit on a covered call that was almost sure will have been assigned,most important gave me a more structured way to look at my choices.

Excellent,like how clearly you present your ideas,same applies to your book on Condor that I purchased for my Kindle.

David

Hi David, thanks for the feedback and glad it helped you!

I own 4500 shares of AAPL,and sold last year 45 contracts for6/18/17 maturity $115.00 call.today the stock is at $131.00 ,what would be the best stratagey to unwind the calls and capitalize on the stock upside?

Thanks

Saul

By selling a $115 call, you have given up the chance of any upside over $115.

I buy options out 2 years are more. I this wise?

Spell checker should say “I buy option out two years from now is this wise?”

Nothing wrong with it as long as you have a plan and it meets your overall risk profile.

A little late, but how is there positive intrinsic value of 5$ in that “Roll out and down” scenario? Wouldn’t you lose on the sale to roll it, since underlying assets have risen, assuming it hasn’t been exercised already since in the money?

Hi Paul, that’s poorly worded on my part, let me change it.

Thanks for the covered call info and sample illustrations to demonstrate. Very informing and helpful. Bolsters my clarity and courage to delve further as I just started to execute covered calls so learning the MATH as well as understanding the 7 plays is empowering. Appreciate your simplification and claruty.

Thanks Karen, great to hear and I wish you the best on your journey. Reach out any time with questions.

Thanks for explaining each method clearly. If I just let a covered call expire, when am I allowed to sell another covered call on the same 100 shares? Is it one hour before close on the expiration day or do I need to wait until the following trading day? I’m just trying to maximize selling weekly covered calls. If I do decide to roll out the covered call to the following week, is there a deadline time for choosing this option? Is it one prior to close on expiration day? I’m just trying to figure out all my options

Hi Paul, you would need to wait for the call to expire before selling another one, or as you said, buy it back before expiration, then you can sell another one.

Thanks Gavin. This is very helpful but one final question. If options expire one hour before trading closes, does this mean I can buy another weekly covered call during that final hour of trading on expiration day? I think the answer is yes but just not sure since option contracts aren’t settled yet. Just making sure.

I don’t think options expire one hour before the close. Where did you get that info?

Yeah, you’re right. I was able to find more information. It sounds like it is still open even during after hours trading.

This is so well explained, I was able to really understanding it after reading through a few times. Very much appreciated!

Thanks Chris, glad you liked it and I appreciate the feedback.

One other possibility…

What if you were to donate the shares when the underlying stock price has exceeded the strike on the short call? If selling the shares instead would have resulted in a long-term gain, can you deduct the entire market value of the donated shares as a charitable deduction? Could you also close the related short call and net that against other gains? If not, could you buy replacement shares, wait 31 days, and then close the call in order to net the loss against other gains?

Interesting idea, but I’m not sure. Substance over form probably takes effect in your example. Also I’ve never heard of anyone donating shares before so not sure how that would even work. Sounds like maybe you’ve done it before? I’m not a tax expert, so best to check with your accountant etc.

I sold a covered call option. If I then simply sell the option, will I also forfeit the premium received, or is that premium always mine no matter what? Thank you!

Hi Pater, the premium is your to keep, but if you want to buy the call back to close it you will have to pay the premium to close it. Depending on what the stock has done the premium paid might be more or less than you initially received when you sold the call. Let me know if that makes sense or if you need more details.

I have the most basic scenario and just want to check. I have a stock that I bought 100 shares and sold the call at a high strike price and the option then on expiration was out of the money. I didn’t see the sense of buying back anything… And the system doesn’t let me do this anyhow since and shows that it is no longer tradeable. Just to be sure, there is no money left on the table correct or no…?

The current values show that the bid is zero. But there is a negative market value.

Correct. Basically if the call is out-of-the-money it expires worthless and no longer exits. You are still left with ownership of the 100 shares.

One of the best explanations of covered call I have ever seen so far. Thanks for all your help

You’re welcome. Thanks Ajay!

Hi, I just have chance to read your article today, well explained! I have a covered call position. Recently the underline suddenly becomes very volatile. Its price rapidly rised, leaving my strike price deeply ITM. But I expect the price will fall back. What’s the best strategy to cope this situation? Is there a way to lock the profit from stock price increase?

Easiest thing is to close the existing position, wait for the pullback and re-enter.

Or you could add another bearish strategy like a bear call spread or a poor man’s covered put.

such great content. binge reading. fantastic. thank you – jacques

Thanks Jacques. Reach out any time with questions.

🙂

Hey Gavin, how to keep both my premium and stocks, let it expire, exercise or sell early to close?

Thanks

If the call is out of the money, you can let it expire. If it’s in the money, you would need to buy it back to close before expiration / assignment.

If I want to sell the stock anyway, can I sell a call itm, and also exercise to sell the shares?

Yes, that is one way to get rid of your shares. When you sell a call, you can’t exercise it though, only the buyer has the right to exercise. But, if it’s ITM it will get exercised eventually.

Love the intricacy involved but it does get confusing. So far, I write a covered call with a profit and expiry fairly close to the current date – not trying to get rich on one trade. In so doing, I am usually able to get out with a profit and then just buy back in or look for another fish.

I do want to stay connected with you – for sure. What is the best way to receive your articles? Thank you!!

Tom

You can sign up to our email list or just email us at [email protected]

Excellent explanation for covered calls -very simple to follow with good understanding. Thanks.

You’re welcome.

Thank you.

Hi Gavin,

Does assigning a covered call and buying back another covered call within 30 days(sell to open) trigger a wash sale?

Thks

It could, but I’m not an expert in this area, so you may want to talk to a tax expert.

Thanks, Gavin, for the detailed explanation of covered call.

How likely the covered call be assigned before expiration date, assuming the company has no dividend distribution?

I had an Uber covered call for the strike price of $59, expiring on Feb 2. I bought the option back at a loss yesterday since I don’t want it to be assigned.

By reading your post, it seems to me that this is not the right thing to do, correct? What would be your suggestions for this situation?

Thanks

Hi FJ,

Technically, an option can be assigned any time. However, in this case, as there is not dividend and there is around $0.55 in time premium remaining, it is unlikely to get assigned, but if the time premium got down to about $0.10 it might get assigned.

Might have to reread the Roll out and down part again. But overall the best explanation.

Gavin, what’s your recommendation for long term holds on stocks that the investor is bullish on. Let’s say a dividend growth investor who’s in it for the long haul to collect dividends but also monthly cash from covered calls. If the underlying security shoots deep in the money, should they let it expire and be assigned then sell a cash secure put, or just close out the position for a debit that month, then just continue to sell a cover call. What would you do?

Great explanation on these exit strategies by the way.

It depends on the individual really. There are also potential tax considerations, if the stock gets called away and I have a large gain, I’m might incur significant capital gains tax. So, generally speaking, if it’s a long-term hold, I would prefer to buy back the calls at a loss and continue holding the shares.

Excellent post! I’ve recently started trading covered calls with some success. This is the first week that my stock price has dropped by almost $9.00 a share. I’m sure I will end up owning the stock at expiration, but now I also may want to sell it after the option expires, unless there is a better recommendation. Overall I think the stock will eventually recover but not certain when and don’t want my account to take a big hit if it takes a while to recover

You can always sell an ATM call or even an ITM call to generate a higher premium and increase the chances that the stock gets called away.