Most income investors spend years (sometimes decades) patiently building a dividend portfolio.

They reinvest, accumulate shares, and wait.

And at the end of it, they’re earning maybe 3–4% per year.

What if there’s a way to target that same income, or significantly more, with less capital tied up and without waiting years to build a position?

That’s exactly what we’re covering in this article.

By the end, you’ll understand why I use selling puts as my primary income strategy instead of chasing dividends.

Contents

- The Case For Dividend Investing

- The Hidden Risks of Dividends

- How Selling Puts Works as an Income Strategy

- Real Numbers: Selling Puts vs Dividends on Starbucks

- 4 Reasons Selling Puts Works Better For Me

- The Honest Risks of Selling Puts

- The Wheel Strategy: Triple Income Potential

- Real Trade Examples: EWA and EWZ

- Final Thoughts

- Frequently Asked Questions

The Case For Dividend Investing

First, let me be fair to dividends.

It’s a legitimate, time-tested strategy and there’s absolutely nothing wrong with it.

The mechanics are simple: you buy shares in a company, the company pays out a portion of its earnings every quarter, and on a blue-chip stock you’re typically looking at a 2–4% annualised yield.

The math is straightforward. The problem is that it’s also the limitation.

To generate $1,000 per month in dividend income, you need somewhere between $300,000 and $600,000 invested.

That’s a significant capital requirement for most people, and it takes years of compounding to get there.

The Hidden Risks of Dividends

Two risks with dividend investing don’t get talked about enough:

1. Full price exposure from day one. The moment you buy shares, you’re fully exposed to the stock price. If the stock drops 40%, you’re down 40%, regardless of what dividends you’ve collected along the way.

2. Dividends can be cut. This one catches people off guard. Companies like Intel and General Electric have cut dividends in recent years. The income stream that felt guaranteed can disappear overnight. The dividend income isn’t as secure as it feels.

How Selling Puts Works as an Income Strategy

Selling puts is the foundation of everything I do for options income.

Here’s how it works:

When you sell a put option, you’re agreeing to buy a stock at a specific price (the strike price) if it falls below that level before expiration.

In return, someone pays you a premium upfront.

Cash that lands in your account today.

There are two possible outcomes at expiration:

– Stock stays above your strike price: The option expires worthless, you keep the premium, and you never have to buy the stock.

– Stock falls below your strike price: You buy the stock, but at the lower price you already agreed to, which is below where it was trading when you sold the put.

The key insight: you’re getting paid to wait for a price you’re already happy to buy at.

That premium hits your account immediately, regardless of the outcome.

This is also Warren Buffett’s favourite way to use options.

Real Numbers: Selling Puts vs Dividends on Starbucks

Let’s put some real numbers on this comparison.

Starbucks (SBUX) — Dividend approach:

- Share price: ~$106

- Annual dividend: $2.48 per share

- Dividend yield: 2.33%

Starbucks (SBUX) — Selling a 30-day put option:

- Capital set aside: ~$10,500 (similar to owning 100 shares)

- Premium collected: ~$270 in one month

- That’s more than an entire year’s worth of dividends, collected in 30 days

Using a cash-secured put calculator, that works out to an annualised return potential of nearly 31%, compared to the 2.33% dividend yield.

To be upfront: this isn’t a completely apples-to-apples comparison, and I’ll address the risks shortly. But the yield differential is real and it is significant.

4 Reasons Selling Puts Works Better For Me

1. You don’t have to own the stock to get paid

With dividends, you buy shares first and then wait to collect income. With selling puts, the income comes first.

You’re using your capital as collateral, not deploying it all upfront.

2. You choose your entry price

Instead of buying a stock at whatever price it’s trading at today, you’re getting paid to buy it at a discount.

That’s a fundamentally better way to build a position in a stock you already want to own.

3. The premium is locked in

Once the premium hits your account, it can’t be taken back. Dividends can be cut at any point by the company’s board.

The premium you collect is yours the moment the trade is filled.

4. You’re not limited to dividend-paying stocks

Some of the best premium-selling opportunities are on growth stocks and high implied volatility (IV) names that don’t pay a dividend at all.

Dividend investors are restricted to a much smaller universe of stocks.

The Honest Risks of Selling Puts

This isn’t a free lunch, and I want to be straight with you about the risks.

Both strategies lose money in a sustained bear market.

If you own shares and the stock drops 40%, you’re down 40% whether you collected dividends or not.

If you’ve sold puts and the stock drops 40%, you’re buying a stock that’s falling, though at a lower price than where it was trading, and with the buffer of the premium you already collected.

As a put seller, you are slightly better off than a pure stock investor in a downturn.

The premium and the lower strike price provide a built-in cushion, but the risk is still real.

Selling puts also requires more active management.

You need to monitor positions, understand rolling strategies, and have an exit plan before you enter. It’s not a set-and-forget strategy the way dividend investing can be.

If simplicity is your top priority, dividend investing has genuine merit.

But if you’re willing to learn the mechanics of selling puts responsibly, the return potential is in a different league.

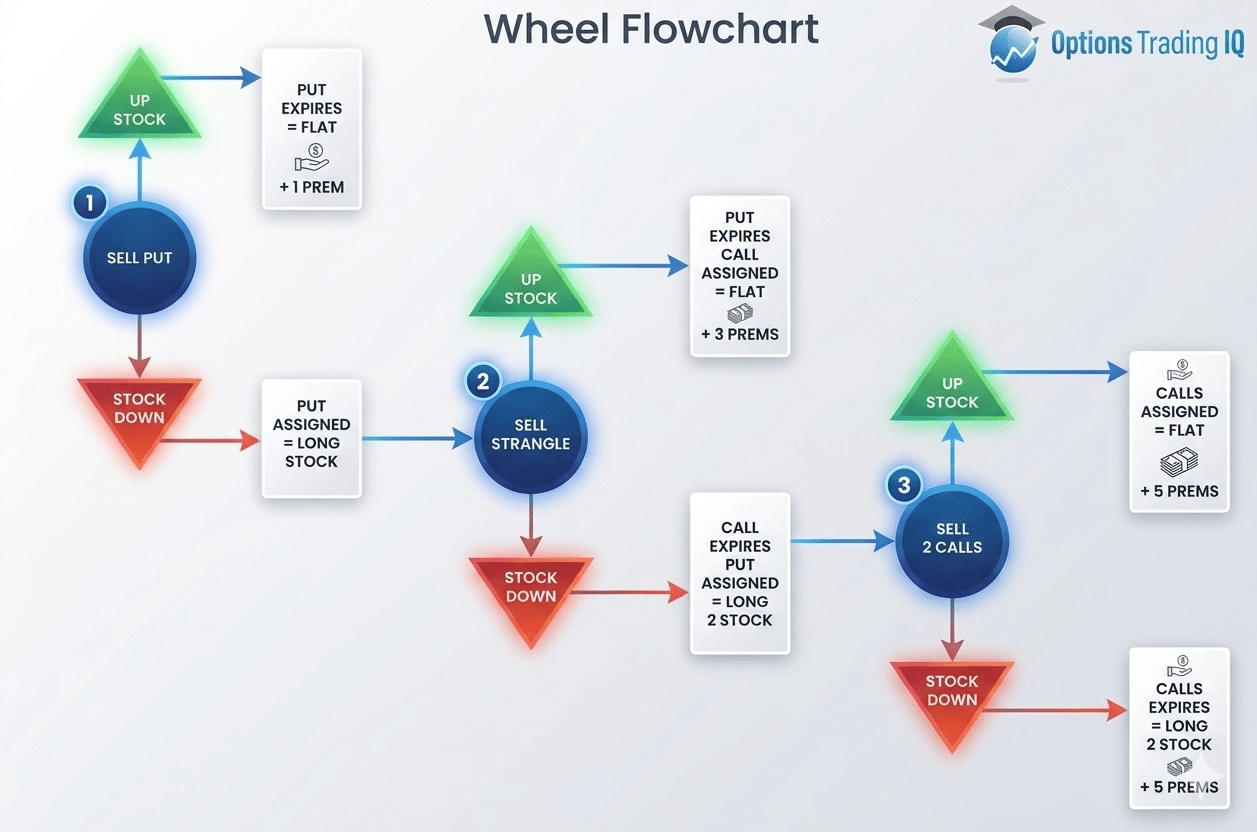

The Wheel Strategy: Triple Income Potential

Here’s where it gets even better, and this is something most people don’t consider.

If you do get assigned on your put, you now own the shares.

At that point, you can sell covered calls against those shares to generate additional income.

And if the stock pays a dividend, you’re collecting that too.

This is called the Wheel Strategy, and when run on a dividend-paying stock, it creates three separate income streams:

- Put option premium (collected while waiting for assignment)

- Covered call premium (collected while holding the shares)

- Dividends (collected as a shareholder)

Here’s how the full wheel cycle works:

1. Pick a stock you like. Sell a cash-secured put below the current price.

2. If the stock stays flat or rises: The put expires worthless, you keep the premium, and you start again.

3. If the stock falls and you get assigned: You now own 100 shares. You can sell a covered call above the current price to generate income while you wait for the stock to recover.

4. If shares get called away: You’re effectively back to cash, having collected multiple rounds of premium along the way.

5. If the stock continues lower: You can sell another put below, potentially accumulating more shares, while continuing to sell covered calls on the position you already hold.

The key is that premium is being collected at every stage of the cycle, whether the stock goes up, down, or sideways.

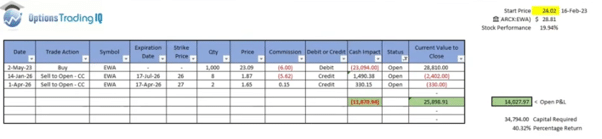

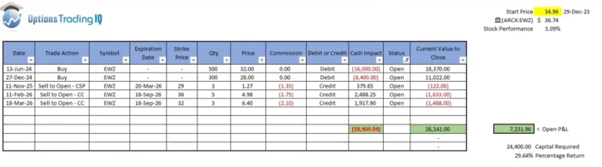

Real Trade Examples: EWA and EWZ

Here are two real examples from my own portfolio running this approach:

EWA (Australian ETF):

- Trade running for approximately 2 years

- Stock price up ~20%

- My portfolio return: up ~40%

- Strategy: selling puts when the stock drops, selling covered calls when it rallies, collecting dividends, using the full triple-income approach

EWZ (Brazilian ETF):

- Trade running for approximately 2 years

- Stock price up only ~5%

- My portfolio return: up ~30%

- Strategy: same wheel approach — generating significant income on a stock that has barely moved

These examples highlight one of the core advantages of this approach.

You don’t need a stock to go up to make money.

The premium income can significantly outperform the underlying asset’s price movement over time.

Final Thoughts

I’m not here to tell you that dividend investing is a bad strategy.

For the right person in the right situation, it absolutely works.

But if you’re willing to learn one additional skill — how to sell puts responsibly — you can make your capital work significantly harder than simply waiting for quarterly dividend payments.

The return potential isn’t even close.

And when you layer in covered calls and dividends through the wheel strategy, you’re building one of the most efficient income-generating systems available to individual investors.

Want to go deeper?

Check out our Options Income Mastery course, which covers everything you need from credit spreads, iron condors, the wheel strategy, to position sizing, and trade management with exact rules you can apply from day one on Interactive Brokers or any other platform.

Frequently Asked Questions

Is selling puts riskier than dividend investing?

Both strategies carry stock market risk.

In a significant downturn, both can lose money.

However, as a put seller you have a built-in buffer — the premium collected and the lower strike price — that gives you a slight advantage over a pure stock buyer.

The key difference is that selling puts requires more active management and an understanding of options mechanics.

Do I need a lot of capital to sell puts?

You need enough to cover the potential purchase of 100 shares at your strike price (for cash-secured puts).

On a stock like Starbucks trading around $106, that’s approximately $10,500 per contract.

For smaller accounts, there are lower-priced underlyings and strategies like bull put spreads that require significantly less capital.

What happens if I get assigned on the put?

Getting assigned means you buy 100 shares at your strike price.

This is not necessarily a bad outcome — it’s a stock you already decided you were comfortable owning at that price.

From there, you can sell covered calls and potentially collect dividends, turning the assignment into the start of a wheel strategy.

Can I use this strategy in an Australian brokerage account?

This depends on your broker and account approval level.

Options trading on US stocks is available through several brokers accessible to Australian investors, including Interactive Brokers.

Always check margin and options approval requirements with your specific broker.

Is this strategy suitable for beginners?

Selling cash-secured puts is generally considered one of the more beginner-friendly options strategies because the risk profile is similar to owning stock.

That said, it’s important to understand the mechanics thoroughly before trading.

Our Options Income Mastery course is designed specifically to walk beginners through this strategy step by step.

We hope you enjoyed this article on selling puts vs dividend investing.

If you have any questions, please send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.