The double calendar option strategy has a couple of strengths that make it a resilient trade even in uncertain times.

By combining two calendar spreads at different strikes, traders get a wider profit zone that can absorb significant market moves, making it particularly attractive when volatility is elevated or the outlook is uncertain.

Contents

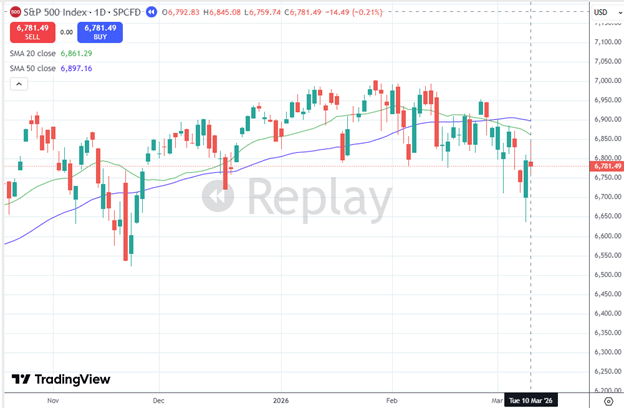

Let’s go back to March 10th, 2026, when SPX was at 6812 and was just turning into a downtrend…

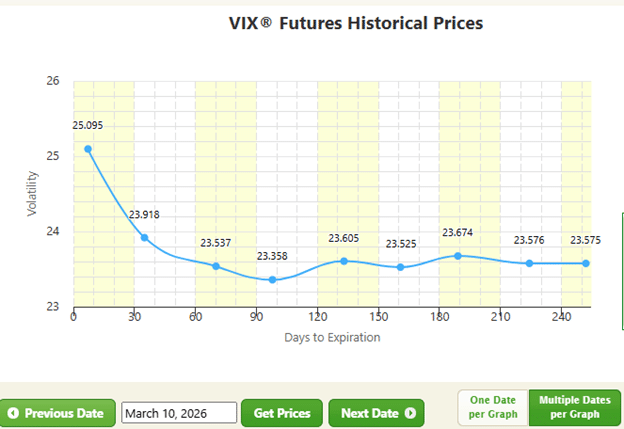

The VIX was moderately elevated at around 25.

The VIX term structure was already showing backwardation, with the volatility of the front month higher than the following month…

This indicates heightened anxiety among investors.

When fear creeps into the market and the VIX spikes, the term structure often flips into backwardation, creating unusually favorable conditions for calendar spread traders who know how to take advantage of it.

Therefore, instead of using the single calendar option, we elected to use the double calendar strategy, which will provide a wider profit graph and can handle large price moves in the underlying asset.

Date: March 10, 2026

Price: SPX at 6812

Buy one contract April 1st SPX 6975 call @ $36.92 [IV = 15.36]

Sell one contract March 27 SPX 6975 call @ $27.56 [IV = 15.36]

Sell one contract March 27 SPX 6525 put @ $54.02 [IV = 24.98]

Buy one contract April 1st SPX 6525 put @ $64.16 [IV = 23.95]

Net Debit: -$1950

Cost of call calendar: (27.56 – 36.92) x 100 = -$936

Cost of put calendar: (54.02 – 64.16) x 100 = -$1014

Max risk is the debit paid for both calendars: $1950

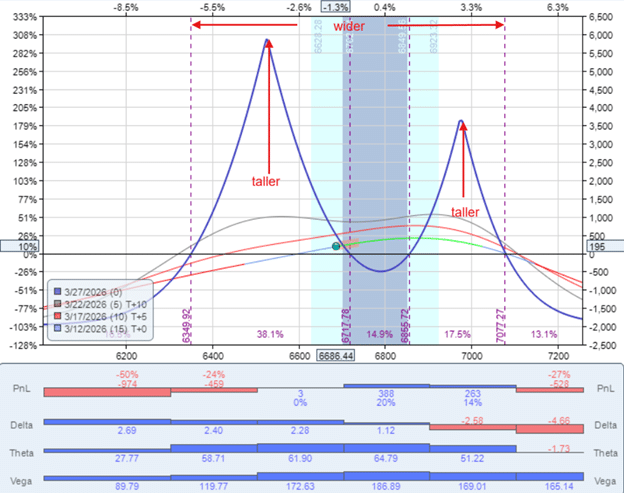

In this setup, the two calendar peaks were placed quite far apart, far enough that the blue expiration P&L curve dips below zero at the current price.

Normally, this is something we’d want to avoid.

However, when the goal is to give the trade room for significant price movement, a small amount of this downward dip can be an acceptable trade-off.

Importantly, this dip is not a practical concern because its negative impact only materializes near expiration. We don’t intend to hold the trade that long.

For this trade, which has 17 days till expiration from its start, our target exit date is approximately one week after entry (about one-third of the trade duration).

This is why the T+6 intermediary P&L line is the curve we care most about. We can see that this profit curve sits comfortably above the current price, with no drawdown.

This early exit approach is a core part of managing options position sizing and risk. Holding a calendar spread too close to expiration exposes the position to rapid gamma risk, where small price moves can quickly erode profits.

By targeting an exit at roughly one-third of the duration, the trade captures the most favorable portion of the theta decay curve while avoiding the turbulence that comes near expiration.

Why Is the Put Calendar Bigger?

For the lower calendar centered below the current price of SPX, we use put options because they are out of the money at that level.

For the upper calendar above the market, we use call options because calls are out of the money when above the current price.

We like to use out-of-the-money options because they are more liquid and have a tighter bid/ask spread than in-the-money options.

The put calendar is larger and offers a higher peak profit because we paid more for it, and as expected, we get what we paid for.

But why is the put calendar more expensive?

In most markets (especially indices), implied volatility is higher for puts than for calls at equidistant strikes.

This is known as the volatility skew.

Higher implied volatility correlates with higher value options.

In addition, the put calendar is in “backwardation”.

That means the near-term short put we are selling has a higher implied volatility than the far-term long put we are buying.

We are selling an IV of 24.98 and buying an IV of 23.95 for the put calendar.

The call options were not in backwardation because both the short and long calls had the same IV of 15.36.

Backwardation is not the normal state of calendars.

Typically, under normal market conditions, the near-term IV would be lower than the far-term IV, a state known as contango.

But when there is fear among investors, we sometimes can see backwardation.

When that happens, we get particularly good reward-to-risk in the calendar, as we can buy it at better prices than normal.

This better reward-to-risk ratio is reflected in the calendar’s expiration graph by taller peaks.

It is worth noting that even under normal contango conditions, the double calendar remains a valid strategy.

The backwardation here simply tilted the reward-to-risk further in our favor, delivering a better entry price and more generous profit peaks than we would typically see.

Traders who understand the volatility term structure can use this knowledge to time their entries more effectively, deploying double calendars precisely when fear-driven backwardation creates the most attractive setups.

Understanding the Greeks: Vega and Theta

A double calendar spread has two key Greek characteristics that work in the trader’s favor when conditions are right.

First, it is a positive vega trade, meaning it benefits from rising implied volatility.

Since we are long the far-dated options and short the near-dated options, an expansion in IV increases the value of the long legs more than it hurts the short legs, particularly when backwardation is already present, and the short-dated IV is already elevated.

Second, the position has positive theta, meaning time works in our favor as long as the underlying stays within the profitable range.

Each day that passes without a large directional move adds value to the spread through time decay on the short options.

This combination of positive theta and positive vega is rare and valuable. Most premium-selling strategies are hurt by rising volatility, making them vulnerable during market sell-offs.

The double calendar, by contrast, actually benefits from the kind of volatility spike that often accompanies a sharp market decline.

This is a significant edge for traders navigating uncertain or choppy market environments.

For a deeper look at how the volatility risk premium plays into options pricing broadly, that concept is worth exploring alongside the calendar’s Greek profile.

Exit the Trade

Two days later, the trade posted a P&L of $195 and was exited for a 10% profit, even though SPX dropped 126 points to 6686.

Because of the drop in SPX, the VIX rose, further increasing option implied volatility.

Long 6975 call [IV from 15.36 to 17.15]

Short 6975 call [IV from 15.36 to 17.18]

Short 6525 put [IV from 24.98 to 26.92]

Long 6525 put [IV from 23.95 to 25.77]

Because the short and long options expire only 5 days apart, any rise in implied volatility affects both legs almost equally.

A clean 10% profit in two days, despite a 126-point drop in SPX, is a strong demonstration of what makes the double calendar so resilient.

A single calendar centered at the market price would have suffered from the directional move away from the profit peak.

The double structure, with strikes placed on both sides of the current price, absorbed that move within its profit zone.

The IV increase from the VIX spike added fuel, expanding the width and height of the profit graph and turning what could have been a small gain into a clean, decisive exit.

Having defined exit rules in advance, such as a 10% profit target or a time-based exit at one-third of the trade’s duration, is equally important to the setup itself.

Without a plan, traders risk holding positions too long, watching profitable trades erode back toward breakeven or worse as expiration approaches and gamma risk escalates.

Disciplined exits are what convert a sound strategy into consistent results over time.

Summarizing

The rise in implied volatility caused the double calendar to expand in both width and height across both the put and call sides.

This is evident when comparing the peak profits and expiration breakeven points in the before-and-after analysis screenshots.

So, in addition to calendar spread adjustment not being necessary, the positive vega from the IV increase provided an added boost to profitability alongside theta decay working in the trade’s favor.

The double calendar option strategy has a very wide profitable range.

Its positive vega characteristics make the trade a bit more resilient on a down move, as implied volatility tends to pump up, which is beneficial to the trade.

The key takeaways from this trade are worth reviewing.

First, choosing between puts or calls for each leg of the double calendar matters, and using out-of-the-money options on both sides keeps the bid/ask spreads tight and execution costs manageable.

Second, the presence of backwardation in the put calendar improved the reward-to-risk at entry, producing bigger profit peaks than a flat term structure would have allowed.

Third, a pre-defined profit target of 10% provided a clear and objective exit signal, removing emotion from the decision.

Fourth, the wide strike placement, while creating a slight dip in the expiration curve at the current price, was entirely acceptable given the short intended holding period and the forgiving shape of the T+6 line.

For traders looking to manage broader options trading risk management during volatile market periods, the double calendar deserves serious consideration as a core strategy.

It performs well precisely when many other non-directional strategies struggle, combining a positive response to volatility expansion with steady theta decay.

When the market is fearful, the VIX is elevated, and the term structure is in backwardation, the double calendar becomes one of the most attractive risk-reward setups available.

We hope you enjoyed this article on the SPX double calendar strategy.

If you have any questions, send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Thanks for the helpful article!