Contents

- Setup Put Side Broken Heart Butterfly

- Comparing To The Broken Wing Butterfly

- Call Side Broken Wing Butterfly

- Call Side Broken Heart Butterfly

- Conclusion

As its name suggests, the broken heart butterfly is a variation on the broken wing butterfly, which itself is a variation of the butterfly option trade.

Some investors feel that the broken wing butterfly is a better alternative than the butterfly.

Could it be that this newer broken heart butterfly variation is an even better alternative than the broken wing butterfly?

We say newer since earliest reference to the term “broken heart butterfly” was by TastyTrade during the last quarter of 2020.

However, this type of trade is nothing new.

It is a credit spread hedged by a debit spread, or vice versa.

Investors have been doing it long before then.

It’s just that they never had a good name for it.

Today, we will take a look at the broken heart butterfly as compared with the broken wing version.

Setup Put Side Broken Heart Butterfly

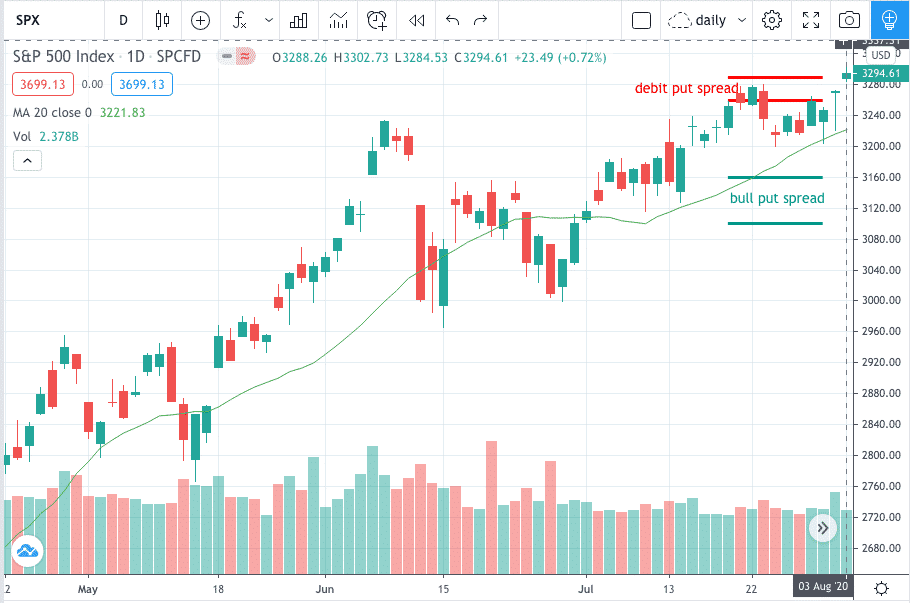

An investor sees a chart of SPX on Aug 3, 2020 with the market on a bull run.

Price is above an upward sloping 20-simple-day-moving average.

As is natural for this investor, a bull put spread is placed on anything bullish.

However, the investor’s conviction is not strong.

The market has already gone up so much already.

Can it really still continue up?

This hesitancy causes the investor to add on an debit spread hedge.

Not a full hedge, but enough to offer some protection if market reverses.

The put broken heart butterfly is constructed as an out-of-money bull put spread with a bear put spread placed closer-to-the-money.

This second spread is the hedge and is smaller (meaning strikes are closer together) so that an overall credit is received for the trade.

Date: Aug 3, 2020

Price: SPX at $3294.61

Short Put Spread:

Buy 1 SPX Sep 18 – $3100 put @ $47.00

Sell 1 SPX Sep 18 – $3160 put @ $58.70

Long Put Spread:

Sell 1 SPX Sep 18 – $3260 put @ $85.80

Buy 1 SPX Sep 18 – $3290 put @ $96.60

Net Credit: $0.90

Max risk: $2,910

Max profit: $3,090

Breakeven price at expiration: 3129

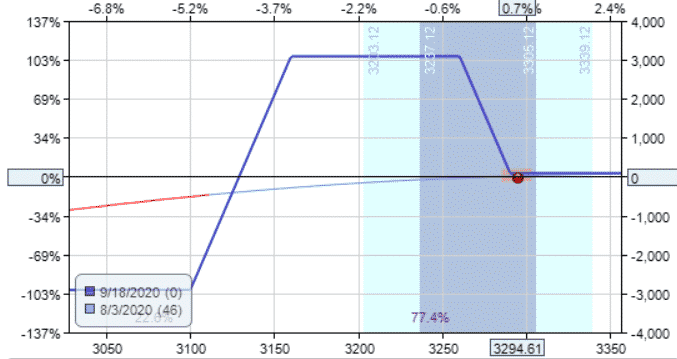

In this example, the short put spread was placed around the 30-delta.

Because the investor has two hedging spreads, the investor feels comfortable putting them on closer to the money than if it was just a solo bull put spread.

However, this location can be adjusted per investor’s preference.

Moving further out of the money will give a smaller Delta and a flatter T+0 line — and hence would be an even more conservative and slower moving trade.

This is not an aggressive trade.

The T+0 line is fairly flat.

The Greeks show low delta and gamma.

Delta: 1.34

Gamma: -0.02

Theta: 7.45

Vega: -37.62

It does have decent theta, which is how this trade will profit, through time decay.

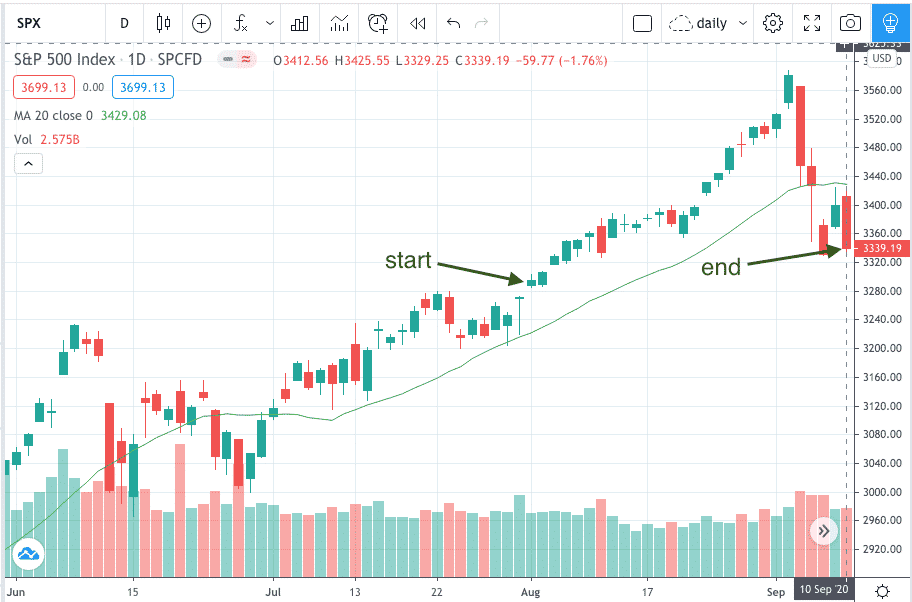

Running this trade in OptionNET Explorer using a stop loss of $582 (20% of max risk) and a take profit of $437 (15% of max risk), this trade exits with a profit of $455 at end of day on September 10.

Ultimately, the investor was correct in that SPX continued to rally.

Comparing To The Broken Wing Butterfly

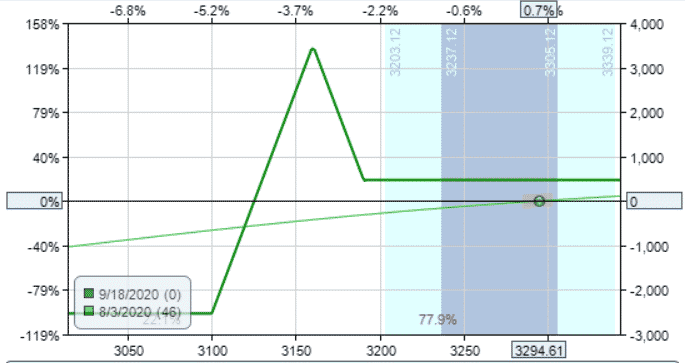

The broken wing butterfly is a special case of the above with the two short strikes coincide.

Buy 1 SPX Sep 18 – $3100 put @ $47.00

Sell 2 SPX Sep 18 – $3160 put @ $58.70

Buy 1 SPX Sep 18 – $3190 put @ $65.70

Net Credit: $4.70

We left the short bull put spread at exactly the same place.

The long put spread is moved closer to the short spread so that the two short strikes are the same.

The short strikes are the body of the butterfly where the heart is.

In the broken heart version, the short strikes are split apart, hence broken heart.

While both the broken heart and broken wing are typically constructed for a credit, a larger credit is collected for the broken wing butterfly.

Max risk: $2,530

Max profit: $3,470

Breakeven price at expiration: 3125.30

The broken wing butterfly has better risk reward with lower max risk and higher max profit.

The Greeks for the broken wing butterfly are:

Delta: 2.47

Gamma: 0.01

Theta: 3.69

Vega: -24.15

The broken wing butterfly version has a higher delta (because we are decreasing the amount of hedging when we move the hedge spread further out-of-the-money).

It also has a lower theta.

With the two spreads close together, it tends to achieve its profits closer to expiration.

Let’s see how this trade does with a stop loss of $506 (20% of max risk) and profit target of $380 (15% of max risk).

Turns out that neither the target nor the stop loss was hit with end-of-day data.

The trade expires on September 18, with the investor keeping the $470 initially collected.

Both broken heart and broken wing butterflies ended up profitable since the price went in our favor.

For longer term trades, that is when price moves away from the butterfly.

Next, we’ll see what happens if price moves towards our butterfly.

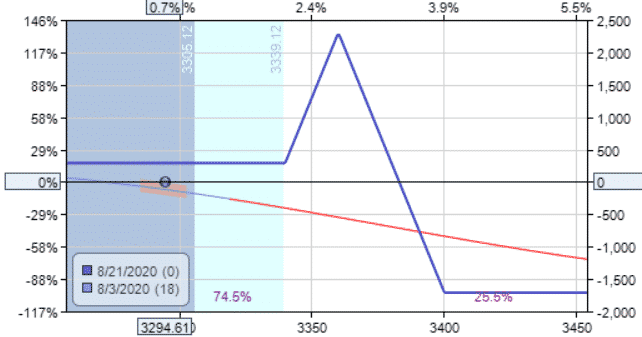

Call Side Broken Wing Butterfly

Another investor looking at the same chart of Aug 3 is thinking, “The market has gone up so much already. Maybe it will go up just a little more, but surely not much higher. It’ll probably reverse down soon.”

Whenever there is that sentiment, the strategies that come into mind are diagonals and broken wing butterflies.

The investor fades the market top expecting the price to drop and uses a shorter time to expiration (18 days to expiration).

A broken wing butterfly is constructed to have no risk on the downside.

Date: Aug 3, 2020

Price: $3294.61

Buy 1 SPX Aug 21 – $3340 call @ $28.15

Sell 2 SPX Aug 21 – $3360 call @ $20.60

Buy 1 SPX Aug 21 – $3400 call @ $10.15

Net credit: 2.90

Max risk: $1,710

Max profit: $2,290

Breakeven price at expiration: 3383

Backtesting this trade with a profit target of $257 (15% of max risk) and stop loss of $342 (20% of max risk), the trades ends with a loss of $485 on end-of-day Aug 12.

Let’s see if the broken heart butterfly does any better.

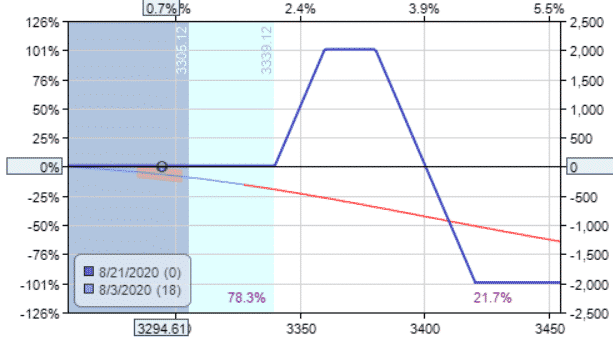

Call Side Broken Heart Butterfly

Splitting the two spreads of the previous call side butterfly to construct a broken heart butterfly.

We keep the long spread the same, but move the short spread further out-of-the-money like this:

Date: Aug 3, 2020

Price: $3294.61

Buy long spread:

Buy 1 SPX Aug 21 – $3340 call @ $28.15

Sell 1 SPX Aug 21 – $3360 call @ $20.60

Sell short spread:

Sell 1 SPX Aug 21 – $3380 call @ $14.65

Buy 1 SPX Aug 21 – $3420 call @ $6.95

Net Credit: $0.15

This reduces the credit to almost nothing.

Another way to think about this is to think of it as an out-of-the money call spread (the long spread), which is financed by selling a further out of the money call spread (the short spread).

The short spread needs to be wide enough to be able to pay for the long spread plus a slight credit.

The slight credit is to remove all risk on the downside.

Max risk: $1,985

Max profit: $2,015

Breakeven price at expiration: 3400

The broken heart butterfly has a wider range of profit as can be seen by a breakeven price that is further away from the current price.

This means it is a higher probability trade.

With the price of SPX at 3295 at start of trade, the broken heart butterfly will profit if price is anywhere below 3400 at expiration.

The broken wing butterfly will profit only if price is below 3383.

Note that in this example, we split the call broken wing butterfly by moving the short spread away from the money and holding the long spread the same.

In the put broken wing butterfly, we had split the butterfly by moving the long spread closer to the money and holding the short spread the same.

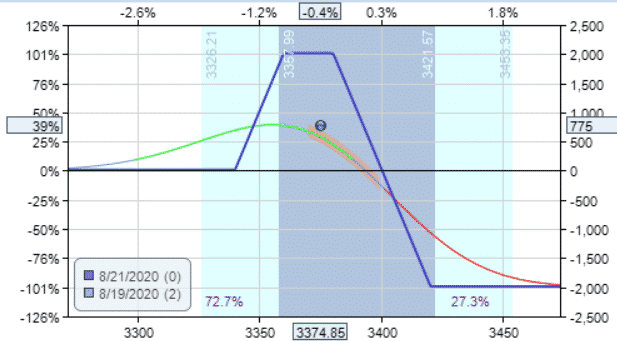

Let’s see how the call side broken heart butterfly does.

Same profit level of 15% of max capital at risk ($298) and stop loss of 20%, or $397.

It ended with profit of $775 at the end of day on Aug 19.

Why did the broken heart not get stopped out on Aug 12th like the broken wing?

The answer is because we had moved the short spread further away from the money.

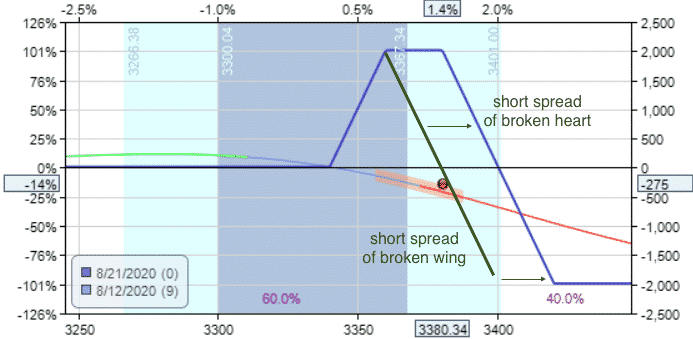

Broken wing butterfly on Aug 12th:

Broken heart butterfly on Aug 12th:

Conclusion

The broken heart butterfly has a larger range in which we can profit from, which is good if prices are uncertain.

The broken wing butterfly receives a larger credit upfront, which is good if there is no movement in price.

One is not necessarily better than the other.

Depending on how the market moves one trade can be more profitable than the other.

But hopefully you now have a better understanding of the construction and dynamics of the two different butterflies.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Having trouble replicating net credits for the put side examples. For the put side BHB, you’re selling a spread for $14.20 and buying one for $10.80; $14.20 minus $10.80 is $3.40 but the example says it’s just $0.90. For the put side BWB, before we even get to the credit calculation, is it even plausible that the price for the highest strike 3190 was less than for the middle strike 3160?

Well spotted Gary, thanks for letting me know. I’ll fix the typos.

What do you think of this setup? unbalanced broken heart put butterfly:

2/-2/-1/1 3200/3215/3220/3240 put (the strike prices are hypocritical), for $0.4 credit. Max profit is $2040, max loss is $960. My thought is that by making the width of the debit spread larger than the width of the credit spreads, it’ll be even better hedge? Also the r/r ratio is 2:1, higher than regular BWB or unbalanced butterfly.

You have a very low profit potential if SPX stays flat and you profit tent on the downside is very narrow (between 3240 and 3205) so you would have to get very lucky for it to finish in that zone. All the risk is on the downside so I don’t think this is going to give you much protection if you’re trying to use this to hedge a portfolio of long stocks.

Gavin do u teach these in your bootcamp

Yes, in the next course starting in December.