Let’s say that you want to invest in the world of real estate. You’re drawn to the passive income and capital gains. You’re a little leery of the lack of liquidity, the operational challenges (chasing tenants down for rent, the ongoing repair and maintenance, etc.), and the amount of capital that is required to get into the game. What do you do?

Welcome to Real Estate Income Trusts or REITs.

A REIT is a pool of investments made by over 100 shareholders, no 5 of which own more than 50% of the shares. A U.S. REIT must hold 75% of it’s assets in real estate, cash or US treasuries. Additionally, 75% of gross income must come from real estate. The real estate holdings can come from ownership of physical real estate, mortgages, or a mix of the two. REITs that invest primarily in physical real estate are classed as Equity REITs. A REIT that primarily invests in mortgages is classed as a Mortgage REIT. REITs that invest in both are considered Hybrid REITs.

Shares in REITs can be traded publicly on a stock exchange or privately. Shares in private REITs are based on the underlying value of the real estate investments. Shares in publicly traded REITs can be pushed up and down based on the trading trends that the REIT is experiencing, so it acts more like a traditional stock. A REIT isn’t specifically designed for stock price appreciation, but capital gains (and losses) can occur based on the price that an investor buys into the REIT and the price that they sell to get out of the REIT. Typically, REITs have high dividend yields.

How does a REIT start?

A pool of investors is brought together to fund the initial purchases. The REIT takes those funds and invests in real estate that produces income. REITs are required to distribute over 90% of the income that is produced to shareholders through dividend distributions.

Because the funds flow through to investors, the REIT doesn’t pay corporate taxes. The distributions to individual investors are taxed as ordinary income, capital gains and return of capital. They then pay taxes at their ordinary tax rate on the ordinary income portion of the income.

Just how big is the market for REITs?

NAREIT, the National Association of Real Estate Income Trusts, keeps statistics on the industry. It is estimated that REITs own about $3 trillion in gross assets. $2 trillion of those assets are held in publicly traded REITs. It’s estimated that 70 million Americans own shares in REITs. Market capitalization of the FTSE Nareit All REITs Index is around $1.1 trillion. Listed REITs paid out $55.7 billion in dividends in 2016. Public, non-listed REITs paid out $4.4 billion in dividends in 2016. Economic activity supported by REITs led to $52.8 billion in new construction and capital expenditures on existing REIT assets. Unsurprisingly, 2 million Americans owe their jobs to investments made by REITs. They are largely an American phenomenon. The United States holds 2/3 of global REIT market capitalization.

How do they perform as an asset class?

The short answer is, well. The dividend yield on the S&P 500 Index is 1.97%. Comparably, the dividend yield on the Nareit All REITs Index is 4.2%. Historical returns on REITs have been solid. From December 31, 1978 to March 31, 2016 US Equity REITs had an annualized return of 12.87%. Comparatively, the Russell 3000 Index of equities had an annualized return of 11.64%. While the long-term returns are comparable to equities, they aren’t immune to bad years. The Dow Jones Wilshire REIT Index had half of it’s value wiped out in just two years. It posted losses of 17.6% in 2007 and more than doubled it with a 39.2% loss in 2008.

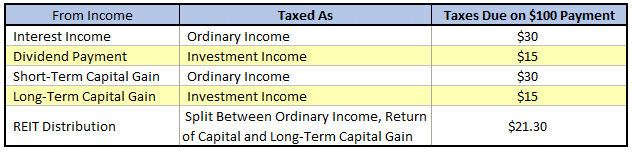

On average, distributions are split into 59% ordinary income, 17% return on capital, and 24% in long-term capital gains.

Because of the split between ordinary income, return on capital, and long-term capital gains, the taxes due on distributions are lower than they otherwise could be.

Let’s look at the tax implications of a $100 payment on someone at a marginal tax rate of 30%.

As you can see, the worst way, from a tax perspective, to receive that income is to receive it as interest income or a short-term capital gain. Dividends and Long-Term Capital Gains are the most tax advantaged, with a distribution from a REIT a little worse off. Dividends and capital gains are, generally speaking, less predictable than a REIT distribution.

What are the types of REITs?

Regardless of whether a REIT is publicly or privately traded, they generally fall into five categories. Each of the five categories are affected differently by changing markets and demographics.

Retail REIT:

Roughly 24% of REIT investments are in financing malls and freestanding retail. Retail REITs get their return from renting units to retailers. Retail REITs are facing some pressures because of the shift to more online sales. Generally speaking, they have proven adept at filling spaces with non-retail focused enterprises or offices. The best example of this is the proliferation of gyms in traditional retail space.

When considering a Retail REIT as an investment there are a number of factors that you should look at.

- How healthy is the retail sector? Because Retail REITs make their money by renting spaces to retailers, store closures are painful. Filling brick and mortar retailing space in an e-commerce world can be a challenge.

- Anchor tenants are extremely important. If a REIT is invested in retail space that holds stable anchor tenants (grocery stores, banks, etc.), it will have less trouble filling the secondary spaces.

- Diversity of investments is important. Retail REITs that have investments spread across a number of sectors and geographical areas are going to have a more balanced risk profile.

Join the 5 Day Options Trading Bootcamp.

Residential REIT:

Residential REITs invest in housing. Typically, it will be in multi-residential buildings and manufactured housing. The largest Residential REITs have their investments clustered around large urban centres. Why? Residential rents are related to housing affordability. If an area has low home affordability, more people will be looking to rent. If more people are looking to rent, vacancies will fall, and the price of rent will increase. Increasing rents are good for the owners of housing stock.

Similarly, when considering an investment in a Residential REIT, look at the markets that they are invested in. If they are experiencing population and employment growth, all things being equal, there will be upward pressures on rents.

Healthcare REIT:

Healthcare REITs invest in real estate that houses healthcare services. Places such as hospitals, nursing stations, long term care facilities, and medical centers. Demographically speaking, they are very well positioned. An ageing population and increasing healthcare costs are the bane of the Social Service Administration, but a boon to investors that have invested in the healthcare industry. Look for a diversity in customers and property types when considering an investment in a Healthcare REIT.

Office REIT:

An Office REIT invests in office buildings. Income comes from the rents charged to tenants. When looking at an Office REIT, there are a number of important factors to consider.

- State of Economy/Unemployment Rate

- A strong economy that is creating good jobs means that office space will have a greater demand. Analyzing the trends in the specific geographical area that the REIT is invested in will give the investor more insight into the REIT than looking at the trends across the entire economy.

- Vacancy Rates

- Simply, supply and demand will dictate that areas that have low vacancy rates will likely see rents rise. Conversely, a high vacancy rate means that landlords will have to compete to fill spaces. That means that rents could be on the way down.

- Capital for Acquisitions

- An Office REIT that has enough capital on hand to take advantage of opportunities is better positioned for long term growth than one that does not have the capital on hand to make further investments.

Sample Iron Condor Trading Plan

Mortgage REIT:

A Mortgage REIT is unique in that it doesn’t invest in physical properties, but does invest in the mortgages that are held on them. A Mortgage REIT behaves much in the same way that a bond would. Increasing interest rates are going to have a downward pressure on the book value of the mortgages that the REIT is holding. In turn, that will put downward pressure on the price of a share in the REIT. The REIT can invest in both primary and secondary mortgages on physical property. Keep in mind, secondary mortgages typically come with a higher interest payment, but also higher risk. If the mortgage holder defaults and the property must be sold off, the first mortgage holder will get paid first. Subsequent mortgage holders are paid out of the remainder of the proceeds of the sale, if there is enough money to pay them out. Roughly 10% of REITs are Mortgage REITs or mREITs.

Who are the major players in the REIT market?

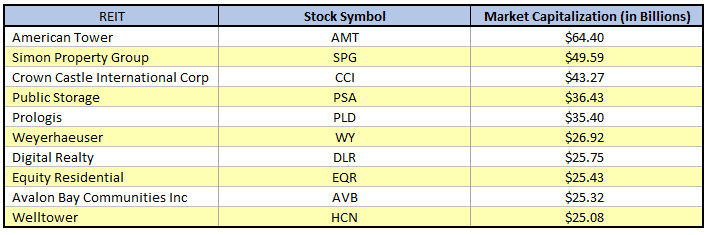

As of December 14, 2017, there were 10 US REITs that had more than $25 billion in market capitalization.

American Tower

American Tower Corporation is headquartered in Boston, MA and focuses investment on wireless and broadcast communications. Currently, American Tower owns and operates over 100,000 sites in 13 countries.

Simon Property Group

The Simon Property Group is headquartered in Indianapolis, IN, and is the largest owner of shopping malls in the USA. Currently, the Simon Property Group owns all, or part of, over 325 properties with roughly 241 million square feet of leasable areas.

Crown Castle International Corp

Based out of Houston, TX, Crown Castle International operates throughout the USA. They own, operate, and lease the infrastructure for broadcasting, mobile networks, and wireless broadband. They operate over 60,000 route miles of fibre optic broadband, and provide cellular network coverage in all of the 100 largest US markets.

Public Storage

The largest self storage brand in the USA is Public Storage. It is headquartered in Glendale, CA, and has international holdings. There are over 2,200 Public Storage self storage properties in the USA, Canada, and Europe. Although Public Storage offers insurance, packing products, and has a substantial interest in Public Storage Office Parks, roughly 90 percent of their revenue comes from self-storage properties.

Prologis

The largest industrial real estate company in the world is run out of San Francisco, CA. Prologis owns, operates, and manages over 3,200 warehouse distribution centers worldwide. Additionally, Prologis has a significant investment management arm.

Weyerhaeuser

A forestry company that morphed into one of the world’s largest owners of timberlands, Weyerhaeuser owns and/or manages over 27 million acres of timberlands through the USA and Canada. In existence since the early 1900’s, Weyerhaeuser expanded into a range of markets unrelated to forestry management. In the 1990’s Weyerhaeuser got out of the financial services, IT consulting, and personal care industries to focus on it’s core, forestry. Currently it’s operations are split into three areas. Timberlands, wood products and real estate/natural resources cover the harvesting and management of forestry, the manufacture of wood products, and the valuable parts of the land that the timberlands are located on. It converted to a REIT in 2010.

Digital Realty

Investing in network-neutral data centers, Digital Realty owns over 130 data centers with over 26 million rentable square feet. Headquartered out of San Francisco, and primarily focused in the USA, they do have significant holdings in Europe.

Equity Residential

A REIT that focuses on apartment buildings in major urban centers, Equity Residential owns all, or part of, over 300 properties with more than 78,000 apartments. It is currently the third largest apartment owner in the USA.

Avalon Bay Communities

Another REIT that focuses on apartment buildings in major urban centers. Avalon Bay Communities is run out of Arlington County, VA and owns over 75,000 apartment units. Most are on the eastern seaboard of the USA, but they do have holdings in Seattle and southern California.

Welltower

Formerly known as the Health Care REIT, explaining the stock symbol HCN, Welltower invests mainly in healthcare real estate holdings. They own seniors housing, long-term care facilities, post-acute care facilities, and office buildings. They do have holdings outside of the USA.

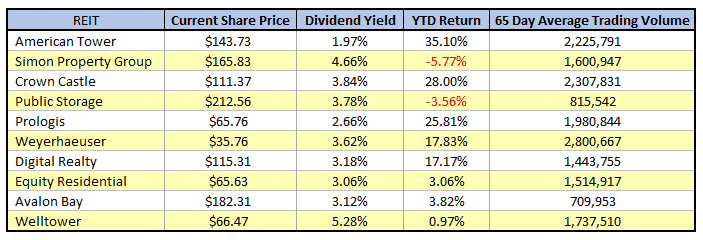

How do these REITS perform?

While these REITs share a large market capitalization in common, there are significant differences in trading volumes, share price and returns. The following chart compares financial indicators that investors look at on the top level. The data is current as of the close of the trading day on December 14, 2017.

A note of caution, past returns aren’t an indicator of future performance. Do your research before investing your hard-earned money.

I hope you enjoyed this introduction to REIT’s. Stayed tuned for more info on REITS over the coming weeks.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Really great article, Gavin. Thanks for putting this together.

Thanks Ken, I appreciate the feedback

Nice info Gavin. Very timely for me. Thanks for doing the work and sharing it.

Thanks Art. Wishing you all the best for 2018.