Small caps have an historic rally in the last 9 trading days with IWM up 13.5% in that time.

Noted technician Mark Arbeter thinks certain asset classes are due for a bit of mean reversion. That includes TLT, IWM and certain metals such as gold. While that is certainly possible, the strength of this relief rally can’t be underestimated, and I tend to think we’ll see a correction through time via some sideways consolidation. A similar occurrence to what we saw after Brexit.

If we do get sideways movement, then Short Strangles are the perfect trade.

Unlike Long Strangles, which benefit from big moves in stocks, Short Strangles do really well when stocks go no where.

Post Brexit, stocks basically went no where for about 3 months. Since the, we’ve come through a decent down move prior to the election and then a historic rally. The last month has been a pretty wild ride, and I think it’s time for stocks to settle down a bit and have some consolidation.

Of course, with small caps starting to look a little stretched and overbought, we could easily see a pullback here. Short Strangles would not do well in that case. They are also “naked” trades with unlimited risk, so they are not for the feint hearted and they do require significant margin. Some traders may not even have access to trade this strategy.

With the above in mind, let’s take a look at how a Short Strangle on IWM might look.

Typically with these trades, it’s best to keep duration short so that time decay can work in your favor. Here I’m looking at the December expiry which is in 1 months time.

For the short strikes, we’ll look at two examples.

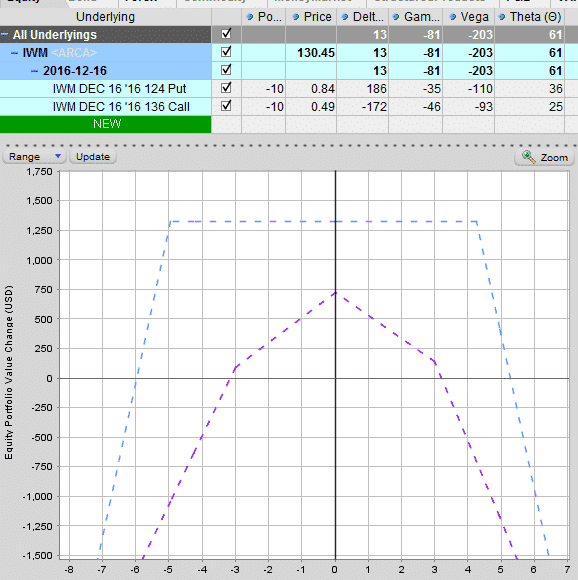

EXAMPLE 1 – 124 Put and 136 Call

These strikes are around delta 17-18 so a little bit more conservative than Example 2. Margin requirement is around $47,000.

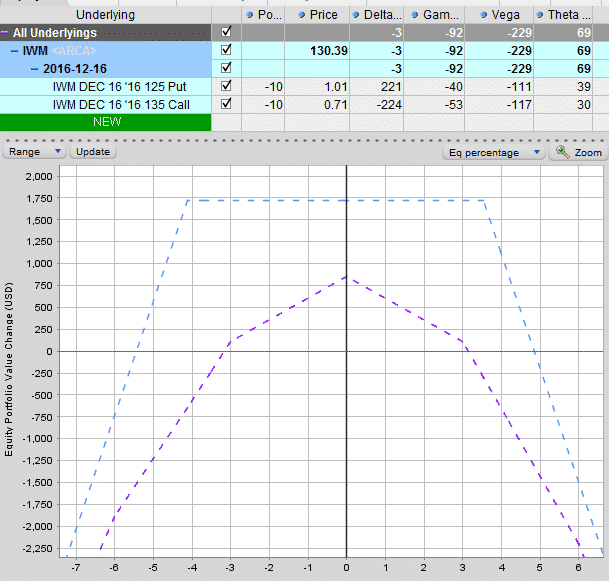

EXAMPLE 2 – 125 Put and 135 Call

The second example is just a little bit more aggressive with strikes places around Delta 22. Margin requirement is around $49,000.

Both trades can withstand a move of 5-6% over the next month. The purple line above represents the trade at Nov 3oth (assuming no change in implied volatility). Provided IWM stays within a +/- 3% range over the next two weeks, the trade should do ok.

Check back in two weeks and I’ll provide an update on how the trades are looking.

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.

Gavin, I was very strongly considering a debit spread for January also a calendar with slightly -ve delta. I do agree I think this is overbought a little bit – What do you think

Small caps are definitely stretched but the momentum is amazing. Not sure I would want to step in front of this steam train.

Interestingly the more RUT goes up the more I want to sell that call credit spread and really be some short deltas. This is what I have been thinking 5 Jan 1450/1460 Call credit spread for 0.8 (Total of 4.00) to partially finance a single Jan 1355/1340 Put debit spread which costs 6.4 and if the market reverses (hopefully soon) sell 5 Put spreads to fully finance the debit spread. In a way leg into the trapdoor strategy that you have been doing before

Nice idea. Hopefully you got this on before the selloff on Monday. The IWM Strangle is looking pretty good so far. I’ll try and post an update today.