If you’ve spent any time trading neutral options strategies, you’ve almost certainly wrestled with this question: calendar spread or iron condor?

Both strategies profit from a quiet, range-bound market. Both use theta decay as their engine.

On the surface, they look like near-identical tools, which is why so many traders treat them interchangeably and end up in the wrong trade at the wrong time.

The reality is that calendar spreads and iron condors are built on fundamentally different volatility assumptions.

Getting this distinction right is the difference between entering a trade that has the wind at its back and one that’s fighting a headwind from the moment you put it on.

This article breaks down exactly when to use each strategy, what conditions favour each one, and how they can actually work together in a portfolio.

Contents

- The Core Structures: A Quick Recap

- The Critical Difference: Vega

- Choosing Based on the IV Environment

- Theta: How Each Strategy Earns Over Time

- Profit Zones and Pin Risk

- Risk Profiles Compared

- Adjusting When Trades Go Wrong

- Best Underlyings for Each Strategy

- Using Both Together in a Portfolio

- Quick Decision Framework

- FAQ

- Summary

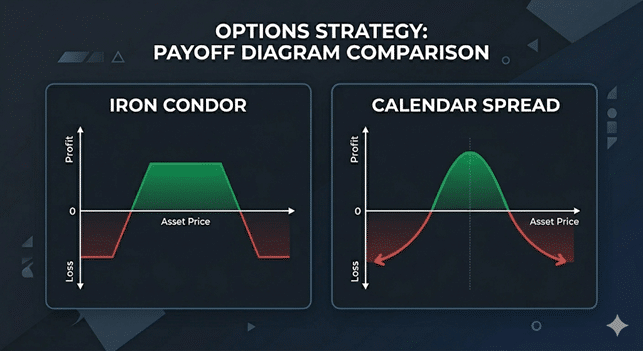

The Core Structures: A Quick Recap

An iron condor sells an out-of-the-money call spread above the current price and an out-of-the-money put spread below it, all in the same expiration.

You collect a net credit at entry.

The trade profits if the underlying stays between your two short strikes by expiration.

For a full breakdown, see our complete iron condor guide.

A calendar spread sells a near-term option and buys the same strike in a later expiration. You pay a net debit at entry.

The trade profits primarily from the short-dated option decaying faster than the longer-dated one, with the underlying ideally pinned near the strike at the front expiry.

For a full breakdown, see our calendar spreads 101 guide.

Both strategies are theta-positive and market-neutral. That’s where the similarities end.

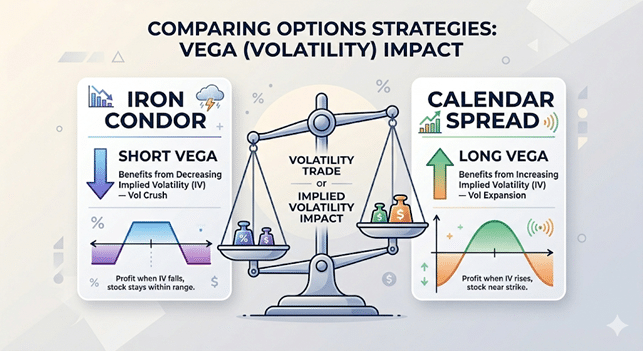

The Critical Difference: Vega

This is the single most important concept in this entire comparison, and the one most traders gloss over.

Iron condors are short vega.

When you sell an iron condor, you have sold more vega than you bought. A rise in implied volatility hurts the trade.

A fall in implied volatility helps it.

Calendar spreads are long vega.

When you buy a calendar, the back-month option you own has more vega than the front-month option you sold.

A rise in implied volatility helps the trade. A fall in implied volatility hurts it.

This single difference drives almost every other comparison in this article.

The two strategies are essentially on opposite sides of the volatility trade.

Think about what that means in practice.

If you enter an iron condor during a period of low IV and then the market gets nervous, IV spikes, and your condor gets hammered, from both the vega expansion and the price movement that usually accompanies it.

The same scenario is actually helpful to a calendar spread.

Conversely, if IV is extremely elevated and starts contracting, your iron condor benefits from the IV crush while your calendar spread is hurt by it.

Getting on the right side of the vega trade starts with correctly reading the volatility environment.

Choosing Based on the IV Environment

The IV environment is your primary guide for which strategy to use.

Favour iron condors when IV is high relative to recent history.

Use IV Rank as your filter. When IV Rank is above 50, meaning the current IV is in the upper half of its 12-month range, you are collecting an elevated premium on your condor and positioning to benefit as IV mean-reverts lower.

This is the natural environment for short vega trades.

The volatility risk premium is most accessible when IV is elevated.

Favour calendar spreads when IV is low relative to recent history.

When IV Rank is below 30, selling premium through an iron condor means collecting thin credits for meaningful risk.

But a calendar spread entered in a low-IV environment is positioned to benefit if volatility picks up; the long back-month vega gains value as IV rises.

This is sometimes called “buying cheap volatility.”

Watch the term structure, not just the level.

For calendar spreads specifically, the relationship between the front and back-month IVs matters enormously.

The ideal calendar entry occurs when the near-term option has higher IV than the back month, a condition called backwardation.

This means you’re selling expensive short-term vol and buying cheaper long-term vol, which is structurally advantageous.

You can monitor term structure through tools like VIX Central.

When the term structure is in normal contango (back months more expensive than front months), calendar spreads are less favourable because you’re paying a premium for the back-month hedge.

Theta: How Each Strategy Earns Over Time

Both strategies are theta-positive; they benefit from the passage of time, assuming price remains stable, but the rate and profile of theta decay differ.

Iron condors earn theta in a more linear fashion throughout the life of the trade, accelerating as expiration approaches and the short options lose value.

Most condor traders target 45 DTE entries and close at 21 DTE or at 50% of max profit, capturing the steepest portion of the theta decay curve without holding through the high-risk gamma period near expiration.

Calendar spreads earn theta less predictably.

The short front-month option decays faster than the long back-month option; that differential decay is the primary engine of profit.

However, the spread value also depends heavily on IV changes (the long vega effect described above), which can either amplify or offset the theta gains.

A calendar spread in a volatile, swinging market can find its theta gains consistently erased by price movement.

The practical implication: Iron condors tend to produce a smoother, more predictable theta income curve. Calendar spreads can be more lumpy, strong gains when the stock pins near the strike, sharper losses when it moves.

Profit Zones and Pin Risk

An iron condor has a defined, flat profit zone between its two short strikes.

Any price in that zone at expiration earns the full credit.

This makes the payoff relatively easy to understand and monitor.

A calendar spread has a tent-shaped profit zone centred on the strike price at the front expiration.

The further the price moves from the strike in either direction, the worse the trade performs.

The ideal outcome is the underlying “pinning” the strike at front expiry, hence the term “pin risk” when your short option is close to the money near expiration.

This difference in shape has a significant practical implication. An iron condor gives you a wide, flat range to be right.

A calendar spread has a narrower, peaked profit zone with steeper edges.

A stock only needs to move moderately in one direction to push you into the loss zone of a calendar, even without breaching what would be an iron condor’s short strike.

For traders who want more room to be wrong about direction, the iron condor’s wider profit zone is an advantage.

For traders who want to benefit from IV expansion within a specific range, the calendar spread’s vega sensitivity is the advantage.

A double calendar spread addresses this partially by creating two profit peaks instead of one, widening the overall tent, at the cost of a higher debit and more complexity.

Risk Profiles Compared

- Iron condor risk profile:

- Entry: net credit received upfront

- Maximum profit: the net credit

- Maximum loss: spread width minus net credit (fully defined)

Risk/reward ratio is typically unfavourable on paper (max loss larger than max profit), offset by the high probability of profit

- Calendar spread risk profile:

- Entry: net debit paid upfront

- Maximum profit: theoretically calculable but unknown in advance (depends on back-month IV at front expiry)

- Maximum loss: the net debit paid (also defined)

The risk/reward ratio can be very attractive, often 3:1 or better, but it requires the stock to cooperate.

Both are defined-risk strategies, which is one of their shared advantages over short straddles or strangles.

However, the iron condor’s risk/reward is known precisely at entry, while the calendar’s maximum gain is an estimate that depends on future IV.

This makes position sizing and profit targeting more straightforward for condors.

The hidden dangers of iron condors, particularly the unfavourable raw risk/reward ratio, are well-documented.

But the calendar spread’s sensitivity to IV collapse is a hidden danger that traders often underestimate when entering the market in the wrong environment.

Adjusting When Trades Go Wrong

Both strategies require active management when prices move against them, but the adjustment toolkit differs.

Iron condor adjustments typically involve rolling the untested side closer to collect more premium and improve the overall position delta, or rolling the tested side further out in time or strike to give it more room.

See our full guide on managing iron condors for specific techniques.

Calendar spread adjustments often involve converting the symmetric calendar into an asymmetric diagonal by rolling the short strike up or down in line with where the price has moved.

This re-centers the profit tent around the new price level.

Our adjusting calendar spreads guide covers the mechanics in detail.

One nuance worth noting: because calendars are long vega, a sudden IV spike that damages the position through price movement can partially offset itself, the long back-month gains vega value even as the position takes a directional hit.

Iron condors have no such partial hedge.

A sharp move, combined with an IV spike, hits a condor from both the delta and vega direction simultaneously.

This makes calendar spreads somewhat more self-hedging in turbulent markets, though not enough to offset a severe directional move against a narrow tent.

Managing vega exposure in calendar spreads is a skill that separates experienced calendar traders from beginners.

Best Underlyings for Each Strategy

For iron condors: slow-moving, range-bound underlyings with beta at or below 1.0, liquid options, and no major upcoming binary events.

Indices and broad ETFs are ideal because they can’t gap on single-stock earnings risk. See our guides on the best iron condor stocks and best ETFs for iron condors.

For calendar spreads: underlyings where you can identify a likely near-term price anchor (a key technical level, a support/resistance zone), and where near-term IV is elevated relative to back-month IV.

Calendars also work well on indices for income traders who want long vega exposure to offset short vega from other positions.

They are generally unsuitable for underlyings approaching earnings unless a specific double-calendar pre-earnings strategy is used.

One important shared rule: avoid entering either strategy on highly volatile, high-beta individual stocks where a single news event can gap price far beyond any reasonable profit zone.

Using Both Together in a Portfolio

Here’s something most traders miss: calendar spreads and iron condors are natural portfolio complements.

An iron condor carries short vega.

A calendar spread carries long vega.

Running both together reduces the overall vega exposure of the portfolio; the condor’s short vega and the calendar’s long vega partially offset each other.

This matters in a practical sense.

An all-condor portfolio suffers badly in volatility spikes.

Adding calendar spreads to the mix provides a partial natural hedge.

When IV spikes and the condor is under pressure, the calendar spread’s long vega is gaining value, softening the blow.

This is one reason experienced income traders don’t run just one neutral strategy. A portfolio that combines iron condors (in high-IV environments) with calendar spreads (in low-IV environments, or as a vega hedge) tends to have a smoother equity curve than either strategy in isolation.

The options income strategies guide covers, in more detail, how to think about building a multi-strategy income portfolio.

Quick Decision Framework

Use this as a starting point when deciding which strategy fits current conditions:

- Lean toward an iron condor when:

- IV Rank is above 50

- The term structure is in contango (normal)

- You want a defined credit and known max loss

- The underlying has a demonstrated tendency to stay range-bound

You want a wider, flatter profit zone

- Lean toward a calendar spread when:

- IV Rank is below 30

- The near-term IV is elevated relative to back months (backwardation)

- You want long vega exposure to hedge existing short vega in the portfolio

- You can identify a likely price anchor for the underlying

You want a potentially higher risk/reward ratio on smaller capital

- Consider both when:

- You want to partially hedge portfolio vega while maintaining theta income

- You’re in a neutral IV environment and want balanced exposure

FAQ

Q: Can I run calendar spreads and iron condors at the same time on the same underlying?

A: You can, but it’s unusual and adds complexity without much benefit. The more common approach is to run them on different underlyings to take advantage of different IV environments across the market. Some traders use an index calendar as a vega hedge while running condors on individual stocks.

Q: Which strategy is better for beginners?

A: Iron condors are generally more beginner-friendly. The defined credit at entry, clear profit zone, and known maximum loss make them easier to understand and size correctly. Calendar spreads require a stronger grasp of vega dynamics and term structure to trade well; getting the IV environment wrong can turn a theoretically attractive trade into a consistent loser.

Q: Is a calendar spread more or less risky than an iron condor?

A: Both are defined-risk strategies, so neither can blow up beyond the capital committed. However, they carry different types of risk. Iron condors risk a sharp directional move breaching the short strikes. Calendar spreads risk an IV collapse (which destroys the long vega value) or a large directional move away from the strike. The raw maximum loss as a percentage of capital at risk tends to be similar.

Q: What about diagonal spreads? How do they compare?

A: A diagonal spread is essentially a calendar with different strikes; it introduces a directional bias that a standard calendar doesn’t have. Diagonals and PMCCs fit between a pure calendar and a covered call in terms of character. They’re useful when you have a mild directional lean alongside your volatility view. Our double-diagonal guide covers how these compare with double calendars.

Q: Do calendar spreads work in high IV environments?

A: They can, but you need to be careful. If you enter a calendar in high IV and IV subsequently collapses, the long back-month vega loses significant value, potentially swamping the theta gains. The exception is the pre-earnings double-calendar strategy, which deliberately enters an elevated-IV environment and exits before the earnings IV crush. See our double calendar pre-earnings guide for how this works.

Q: Which strategy works better on indices like SPX and SPY?

A: Both work well on indices for different reasons. Iron condors on indices benefit from the absence of single-stock gap risk and the broad diversification that keeps prices more range-bound. Calendar spreads on indices benefit from the reliable, liquid term structure and the ability to use them as portfolio vega hedges. Many systematic income traders run iron condors as their primary strategy on indices and use calendars tactically when IV is compressed.

Q: How should I size these trades relative to my portfolio?

A: The 2% rule, risking no more than 2% of total portfolio value on any single trade, is a reasonable starting point for both strategies. Because calendar spreads are entered at a debit, the capital at risk is simply the debit paid. For iron condors, the capital at risk is the spread width minus the credit received. Size based on actual capital at risk, not notional value.

Summary

- The calendar spread vs iron condor decision ultimately comes down to one question: what is implied volatility doing, and which direction is it likely to move?

- Iron condors are short vega income trades that thrive when IV is elevated and declining. Enter when IV Rank is high, and you want to sell expensive premium.

Calendar spreads are long vega income trades that thrive when IV is low and likely to rise.

Enter when IV Rank is compressed and near-term vol is elevated relative to back months.

Beyond the IV environment, the choice also depends on your preference for defined credits vs. debit structures, your tolerance for the calendar’s narrower tent shape, and whether you want to manage overall portfolio vega.

The most sophisticated income traders don’t choose between these two strategies; they understand when each one has the edge and rotate between them accordingly, or use them together to build a more balanced portfolio.

Related articles:

- Calendar Spreads 101: Everything You Need to Know

- Iron Condors: The Complete Guide

- Adjusting Calendar Spreads

- Options Income Strategies: The Complete Guide

- Volatility Risk Premium is the Edge

We hope you enjoyed this article on calendar spreads and iron condors.

If you have any questions, send an email or leave a comment below.

Trade safe!

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.