The below is a guest post from Whealthy Ninja.

Contents

This is an analysis I wrote down a few weeks back, which was only meant for my thought process and decision making only, but I think it is worthwhile to post this up to share my thoughts on KMD and get some feedbacks, second opinions on my analysis.

I wrote this analysis when KMD released their half-year result and announced the equity raising back in March, so some parts are probably out of date, but I think the core analysis remains relevant.

My thoughts are messy, that’s why I write it down to try to organise it because I feel like it allows me to make better decisions (hopefully).

So, I do apologise if this post still seems messy to you and I would love to hear your thoughts on KMD and my analysis.

If you live in Australia or New Zealand, you probably heard of Kathmandu.

The company engaged in the design, marketing and retailing of clothing and equipment for travel and adventure.

Now, COVID-19 is when sh*t hit the fan and it’s a test for a company, but so far KMD seems to fail the test and their investor.

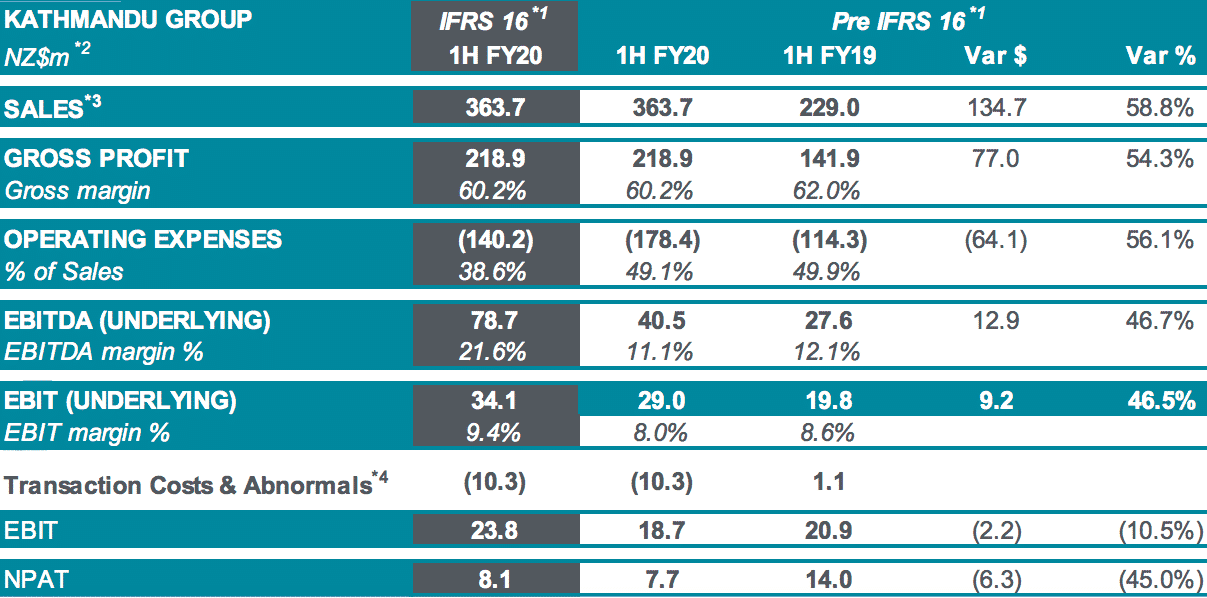

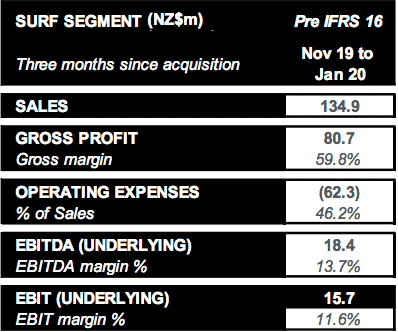

Despite a great performance in their first half, 46.5% increase in EBIT with the recent acquisition of Rip Curl contributing 15.7 million in EBIT within only 3 months since acquisition.

NPAT is 18.4 million when not accounting for the acquisition cost.

I think the fact that KMD has to reach out for help this early in the pandemic proved that they were walking on thin line before sh*t hit the fans.

It would be a better option to wait for the share price to recover before raising equity to minimise the dilution.

KMD has stood down almost all their staffs and cut management wages by 20% but it seems like they are still not well-positioned to deal with the pandemic.

I feel like they are forced by the bank to raise more money as the extension of their loan is subject to the success of equity raising.

Group Results

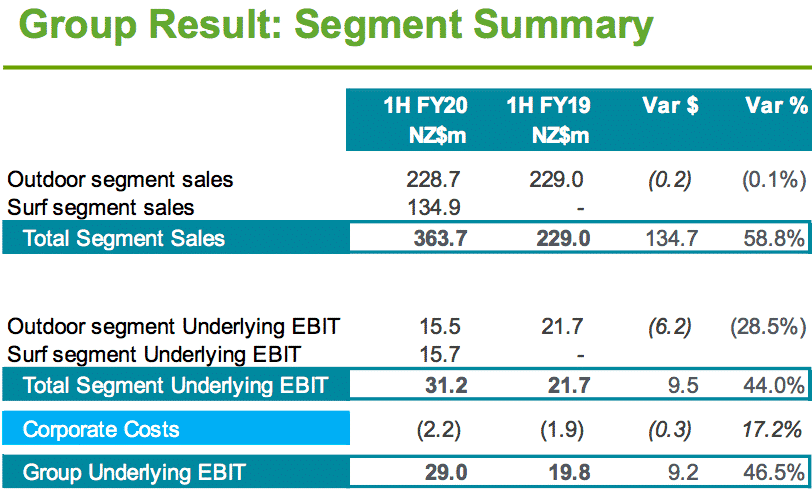

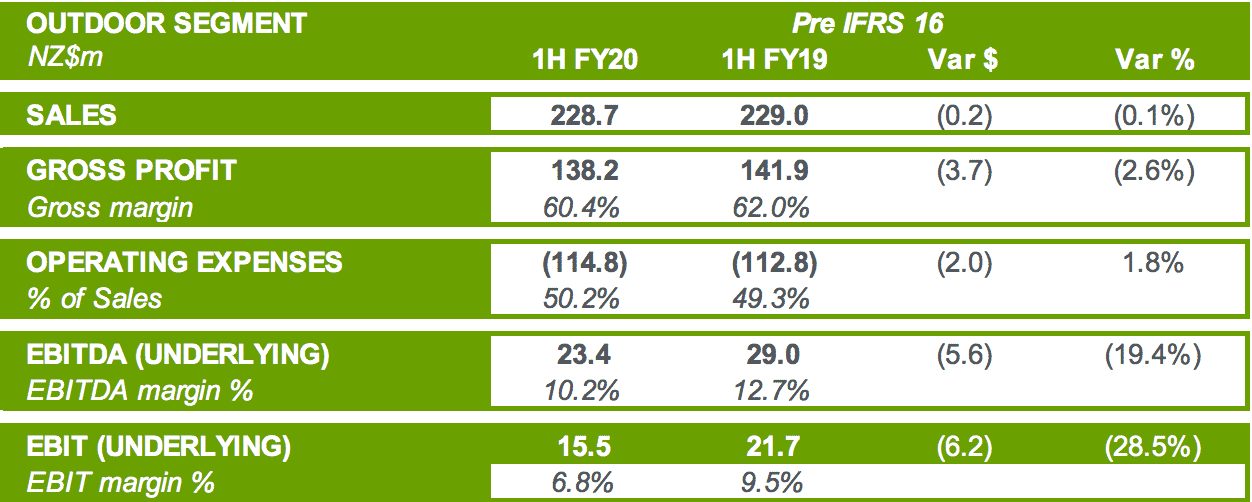

First, let look at the positive side, the half-yearly is pretty good except for the fact that outdoor margin (KMD and Oboz) has decreased significantly (28.5%).

This is due to the foreign exchange rate, an increased mix of clearance sales and wholesale. Rip Curl’s margin seems great since their sales are only half of the outdoor sales but the EBIT is about the same.

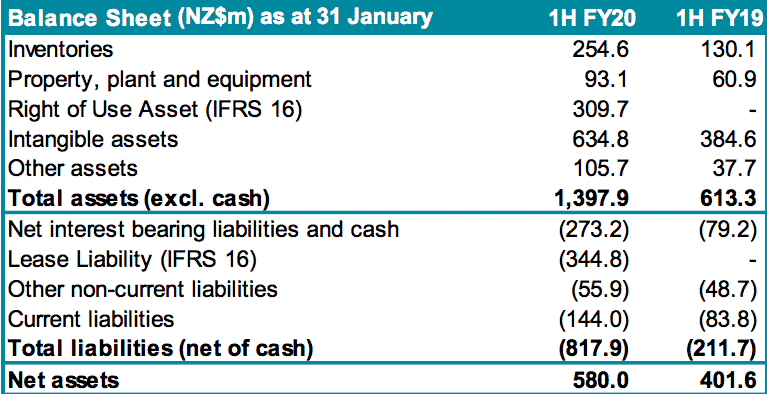

Looking at their balance sheet inventories has increased significantly due to low demand and Rip Curl acquisition.

I think KMD made the same mistake as I did when we see COVID 19 as a china problem and it gonna only affect supplies.

KMD high debt is disturbing since net debt/equity is around 47% and we haven’t take into account the massive lease liability of 344.8 million (net asset is only 580 million).

Outdoor Segment (KMD and Oboz)

Sales are flat, but margins have been deteriorating and that led to the 28.5% decrease in EBIT.

Flat sales also mean that Kathmandu brand sales have been decreasing since the sales figures here includes Oboz and Oboz total sales is up 10%.

But, a 10% increase in Oboz sales is only 2 million. Don’t get me wrong, I wish that I have 2 million but this immaterial to KMD sales.

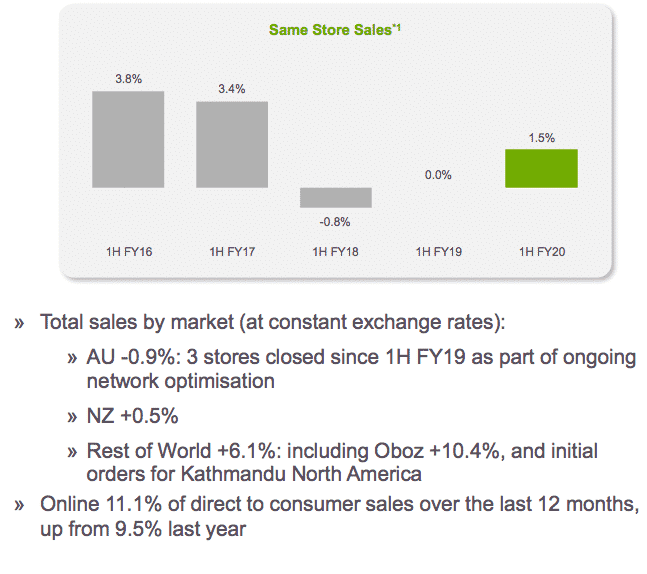

So KMD brand sale is only slightly down (~1%), but management is trying to hide this fact by combining KMD and Oboz sales together and only mention KMD same-store sales growth of 1.5%.

KMD brand has always performed poorly outside of winter and this showed their dependant on the winter products.

The group is trying to eliminate this through the acquisition of Rip Curl, which has strong sales during summer.

KMD brand sales decreased is also caused by the closure of 3 stores in Australia since 1H FY19 as part of ongoing network optimisation.

It is good that management has recognised the bottom-line issues (margins) and start taking action to try to mitigate it.

Closing stores will reduce expenses (rent and employees) and avoid 2 stores taking revenue from each other.

This can hurt top-line (sales) in the short term but hopefully, this will encourage customers to shop online and bring the margin back up.

On the bright side, same-store sales for AU and NZ are both up 2% and 0.5% respectively, online now is 11.1% direct to consumer (9.5% last year).

KMD sales have been stagnant in the last few years and seem like their stores have sales all the time (I live close to a KMD store and noticed) in order to maintain revenue which results in the lower margin.

Oboz has the same story with higher operating cost but it is due to the new investment to grow the brand.

Overall, KMD outdoor segment sales have been stagnant and bottom-line (EBIT) has been suffering to maintain top-line (Revenue).

Overall, KMD outdoor segment sales have been stagnant and bottom-line (EBIT) has been suffering to maintain top-line (Revenue).

The first reason is as mentioned above, KMD brand is highly dependent on their winter product.

Management purchased Oboz and Rip Curl to attempt to fix this issue, Oboz has been performing great but the contribution to the group is still immaterial.

The second reason is KMD’s core market (Aus and NZ) is in their mature stage, I doubt that we will see exceptional growth in these core-markets anymore and it seems like KMD management can see that as well.

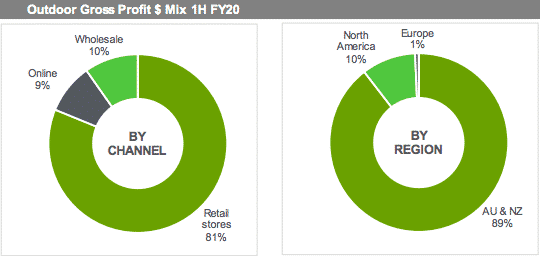

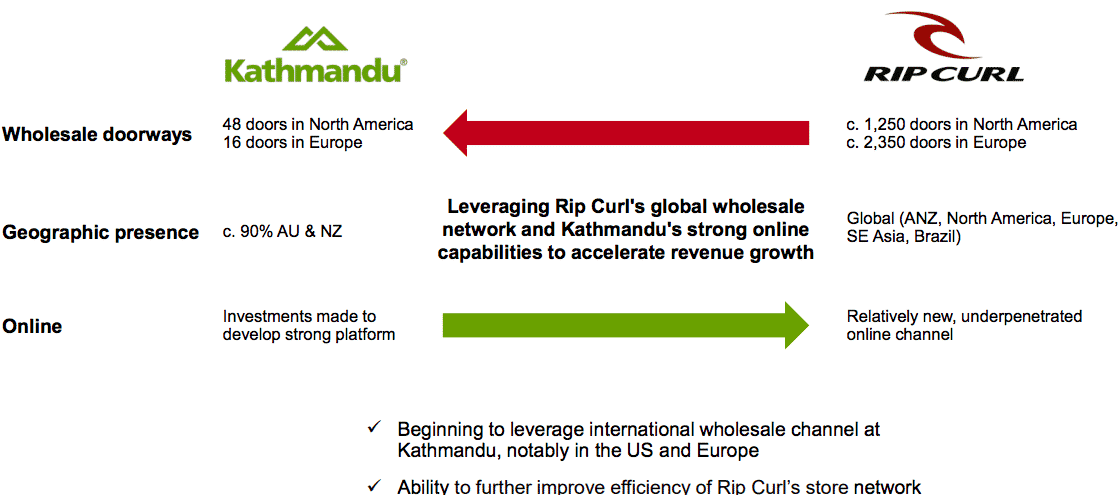

The purchase of Oboz and Rip Curl is also mean to expand KMD products through Oboz and Rip Curl wholesale channels in North America (Oboz) and all over the world (Rip Curl).

This seems like a sound strategy to me as I can see a lot of similarity between KMD and The North Face and The North Face has been very successful by having a mix between retail and wholesale.

So far, we have only seen KMD focusing on their retail but with the purchase of Rip Curl recently, KMD will try to expand their wholesale channels and hopefully the KMD brand will be global.

Surf Segment (Rip Curl)

The highlight of KMD performance is probably their surf segment with 134.9 million sales within 3 months with a successful Christmas trading period.

It’s please to see it contributed half of the group EBIT (15.7 million) within only 3 months of trading. But again, this shows that KMD needs to focus on restructuring its KMD brand to achieve a higher margin.

I think to close down some store and focus on online sales will be a great choice for KMD (seem like they are already on to this with 3 stores closure).

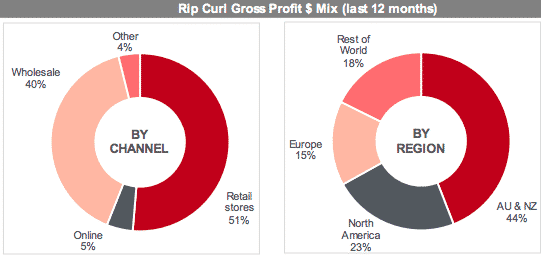

Rip Curl (RC) has a better mix between wholesale and retail compare to KMD brand, so KMD is hoping to use this to gain access to more wholesale doors and grow their wholesale segment.

On the other hand, RC online seem to be underleveraged with only 5% so KMD could help RC improve on this area.

RC sales footprint is much wider than KMD with more than half of their gross profit (56%) comes from other countries other than AU and NZ. KMD hope to take advantage of this when purchased RC to gain access to these regions and make their brand global.

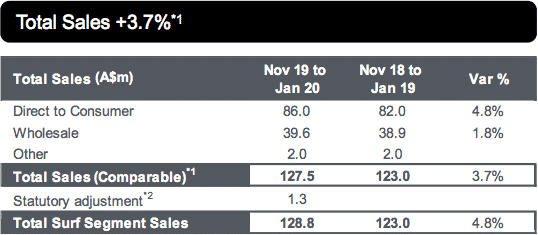

- RC total sale is up 3.7% compared to the same period last year, with strong growth in their core markets AU & NZ: +3.2%, Rest of World +4.5%: North America performed particularly strong.

- Online 6.5% of direct to consumer sales over the last 3 months, up from 6.0% last year

- Same-store sales +2.7% (at constant exchange rates) for the 12 full weeks of ownership from 4 November 2019 to 26 January 2020

- Online comparable sales +19.5% (at constant exchange rates) for the same period

Even though it’s too early to say, RC impressive performance has shown that RC purchase is not a wrong decision by KMD.

But it was at the wrong time due to the COVID-19 outbreak, so the right decision at the wrong time would ultimately be the wrong decision.

However, we should wait a few years for this to play out completely to judge if it’s ultimately the wrong decision or not.

When KMD purchased RC, there are possible chances for synergies but even without taking into account any synergies, the group earning per share was expected to be +10% and this would have been a value-added to KMD shares.

But now since the COVID-19 outbreak, a lot has changed.

KMD forced to issue more shares at a deep discount price and this is a value destroyer. Can KMD make it through this sh*t show?

How much will the equity raising and COVID-19 destroy KMD value?

How much does KMD worth? I will cover this in my next post, which I will release sometime next week on my blog so subscribe to my newsletter to be the first to know.

Whealthy Ninja is a blogger who writes about investing and personal finance. He seeks to be a better investor and achieve financial independence through investing by putting his thoughts and analysis out for discussion and criticism. Follow his blog for more stock analysis, personal finance tips.

“Make money your sword and do not stab yourself”.

Disclaimer: The information above is for educational purposes only and should not be treated as investment advice. The strategy presented would not be suitable for investors who are not familiar with exchange traded options. Any readers interested in this strategy should do their own research and seek advice from a licensed financial adviser.