When trading Delta Neutral option strategies, there are times when the Delta exposure becomes higher than what we initially planned for the trade. Perhaps the market has made a sharp move resulting in a skyrocketing Delta.

The trader wants to stay in the trade, but is concerned that further moves will see losses start to accelerate. One solution is to use futures to temporarily hedge the Delta exposure. This can be a short-term solution until things settle down. The beauty of using futures to hedge rather than other option trades is that futures have no exposure to the other greeks – Vega, Gamma, Rho and Theta. However, futures should only be used by sophisticated investors who understand how they work and the risks involved.

Traders with small accounts should not use futures as the exposure is too large.

In this article, I’ll look at what futures are, how they work and how they can be used to hedge option Delta.

What is a Futures Contract?

Simply put, a futures contract is an agreement to buy or sell an asset at a future date at a contracted settlement price. Futures contracts are standardized and traded on an exchange, just like options. The Chicago Mercantile Exchange (CME) is one of the biggest futures exchanges. Others include Intercontinental Exchange (ICE), New York Board of Trade (NYBOT), NYSE Euronext and the London Metal Exchange (LME).

In a futures contract, one party agrees to buy a specified quantity of securities or a commodity, and take delivery on a certain date. The other party in the transaction agrees to provide those securities or commodities.

Futures were designed as a hedging instrument for commodity producers. For example, farmers can lock in a price for their orange juice in advance by entering into a futures contract to sell their orange juice in the future at a specified price. By doing this, they are protecting themselves from an unexpected decline in price. Their price is locked in no matter what happens between that date and the delivery date.

By the same token, airlines might want to lock in the price for jet fuel. They would enter into a futures contract to buy the jet fuel for a specified price on a specified date. No matter what happens, their price is locked in.

Both examples are of the participants, hedging their exposure.

On the other side of the coin are the speculators. These are traders who take a view on the future prices of a security of commodities and enter into a futures contract looking to profit. A trader who thinks the S&P 500 is going up, would buy a futures contract, looking to lock in today’s price. He will profit if the S&P 500 is higher on the expiration date of the future.

Traders who speculate in commodities would never take physical delivery. They would always trade out of their position and lock in the profit.

Futures are leveraged instruments and traders can maintain an exposure far greater than the amount of capital required to enter the trade. This means gains and losses are accelerated. Some futures can be trade with leverage of 10:1 or even 20:1. It is the futures exchanges who set the rules regarding leverage and margin requirements.

Stock Index Futures

There are too many stock index futures to list here, but some of the major ones include:

S&P 500 Futures – Code SP

E-mini S&P 500 Futures – Code ES

E-mini NASDAQ 100 Futures – Code NQ

E-mini Dow Futures – Code YM

Russell 2000 Index Mini Futures – Code TF

You can see more of the products offered by CME here and ICE here.

In terms of pricing, using the S&P 500 Futures as an example, a 0.10 move in the index results in a $25 change in the price of the future. So, if the S&P 500 makes an -18.44 move as it did today (Dec 14, 2016), traders who were long the future would lose $4,610. You can understand why I mentioned futures are only for those with large accounts!

In terms of exposure, the value of the contract is the index price x $250. Therefore, the current value of the future is roughly 2,253.28 x 250 = $567,930. The actual exposure will vary slightly depending on which contract month you are trading.

The S&P E-mini is only $50 x the S&P 500 index value, so roughly 2,253.28 x 50 = $112,664. The exposure of the E-mini is much less, and for this reason, E-minis have become very popular in recent years.

How to Hedge Option Delta Using Futures

Now that you understand a little bit about futures, let’s look at how they can be used to hedge option Delta.

Let’s assume a trader has an open iron condor that is under pressure on the call side. The trader thinks the index will still finish below the short strike so he doesn’t want to move the calls. He also doesn’t want to use options to hedge the Delta because they could suffer from additional losses due to changes in implied volatility and time decay.

Instead, what he decides to do is buy an E-mini future to help avoid further losses if the index continues going higher.

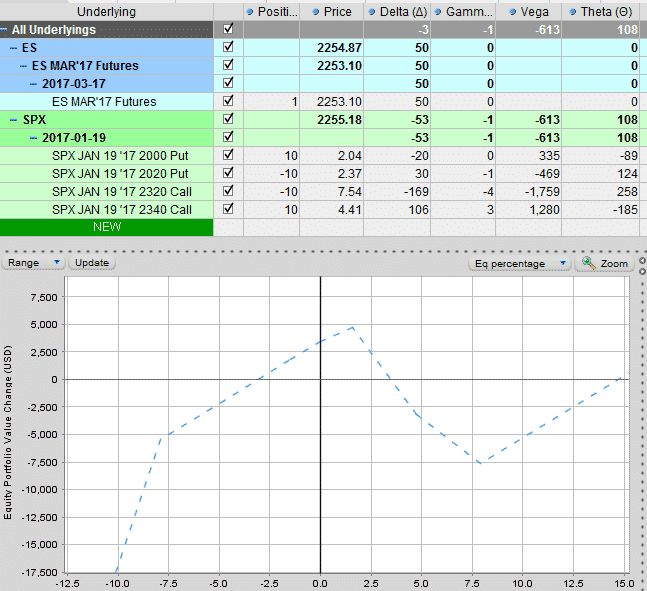

Here we have a theoretical position that has become skewed and the calls are under pressure. Notice that Delta is -53.

Assuming the trader doesn’t want to move the calls and doesn’t want to use another adjustment strategy, let’s look at how we can use futures.

Here the trader has bought one March 2017 E-mini S&P 500 future. This contract has a Delta of 50 which will remain constant. Notice that none of the other greeks have changed. All we have done is reduce the Delta exposure.

Now the trader’s losses will be much less if the index continues to rally. If the index falls back down, he can sell the future (hopefully for only a small loss). By adding the future, the trader has hedged his Delta exposure for the time being.

Using Futures While Entering Trades

Another time to use futures can be when entering iron condors. Have you ever entered one side of a condor, only for the market to move in the direction of the spread before you get a chance to enter the other side? It can be annoying and it means leaving potential profits on the table.

Let’s say a trader enters two orders, a bull put spread and a bear call spread to make an iron condor. The bull put spread gets filled straight away, but he can’t get filled at a good price on the call side.

The market starts to drop, resulting in the call spread dropping in value before he has had a chance to get filled. Instead of panicking and selling the call spread for a less than desired amount, the trade can sell an index future. This can buy him some time while he waits for the market to bounce back.

If the market doesn’t bounce, his losses on the open bull put spread will be partially offset by the gains on the short future.

If the market does bounce, he can take a small loss on the short future and enter the call spread for the price he wanted.

Using futures in this way can help prevent big losses when a trader only has one side of the condor open.

Summary

All option trades have exposure to various greeks – Delta, Vega, Gamma, Theta and Rho. Rather than using more options to hedge Delta, Futures can be used to hedge Delta exposure with the added advantage of not altering the exposure of the other greeks. Using futures to Delta hedge is an advanced strategy and requires a large amount of capital. It should only be attempted by experience, well capitalized traders.

Thanks Gav, very helpful.

Thanks Mike, glad you found it helpful.

Hi Gav, i have a few questions. 🙂

1. Which month is the future bought in? Is it always the active month or the one most closely aligned with the expiry of the condor?

2. Why buy a future instead of going long SPY?

Thanks!

Hi Mike, great questions. I try and match the future with the condor expiration, but they will all perform similarly if you are only holding it for a few days. Yes going long or short SPY will have the same impact on Delta without touching the other greeks. The advantage of the futures, is they can be traded 24/7. So if markets are crashing overnight due to some terrorist attack, you can hedge your exposure without having to wait for the market to open. I probably should have mentioned that in the article…

It’s good strategy. Points which needs to be taken care is to exit as soon as price return back else it can blow off account in negative direction.

Do you recommend to enter future before strike price is reached or after strike price is reached.

Any precautions to be taken. Can the future be hedged for long term…up to expiry.

I don’t like to let my short options going ITM, so I would hedge before the short strike is reached. I wouldn’t use futures for long-term hedging, mostly just short-term. You can also use underlying shares, futures are more if you need to hedge after-hours when the shares can’t be traded.